Dollar General (DG) Stock May Be 27% Undervalued Despite Raised Guidance

Dollar General stock has delivered a steep 40.3% decline over the past 5 years, yet current valuation checks and intrinsic value work both suggest the shares now trade at a discount to what the underlying business may be worth.

- Over 5 years, Dollar General shareholders are down 40.3%, which sets expectations for a potential reset in how the stock is priced relative to its fundamentals.

- Rising gas prices and household cost pressures can support revenue as consumers trade down to discount retailers. However, any shift in that trade down trend or pressure on margins would directly affect what investors are willing to pay for the stock.

- Dollar General screens as undervalued on most metrics, with valuation checks indicating the stock looks cheap in 5 of 6 areas, according to the broader assessment on Simply Wall St.

The issue now is whether the current discount implied by both the intrinsic value estimate using a Discounted Cash Flow (DCF) approach and the market multiples gives investors enough margin of safety after such a weak 5 year share price performance.

Is Dollar General a Bargain on Cash Flow?

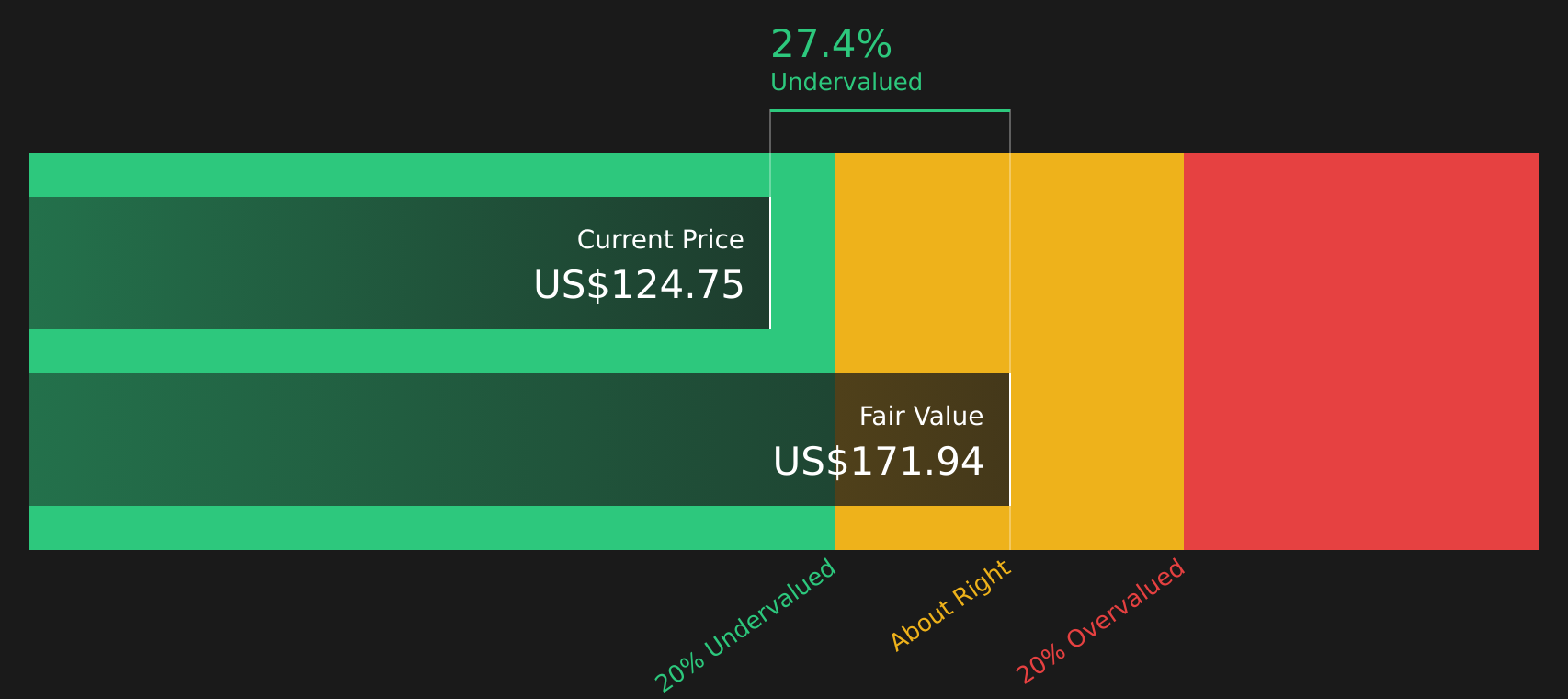

The Discounted Cash Flow (DCF) approach estimates what Dollar General is worth today based on the cash it is expected to generate in the future. Dollar General produced about $2.0b of free cash flow over the latest twelve months, and the 2 Stage Free Cash Flow to Equity model assumes these cash flows continue growing rather than shrinking.

Based on these projections, the DCF points to an estimated intrinsic value of about $172 per share. This implies the stock trades at roughly a 27.0% discount to the cash flow based estimate. Because Dollar General has recently attracted hedge fund interest as consumers trade down to discount retailers, the current price still sitting below the DCF value indicates investors may not be fully pricing in those cash flows.

On this cash flow view, Dollar General stock appears undervalued relative to its estimated intrinsic value.

Our Discounted Cash Flow (DCF) analysis suggests Dollar General is undervalued by 27.0%. Track this in your watchlist or portfolio, or discover 47 more high quality undervalued stocks.

Is Dollar General Still Cheap on Earnings?

The P/E ratio is a useful measure for Dollar General because earnings are a key lens for consumer retailers. Dollar General currently trades at about 17.7x earnings, which is below both the Consumer Retailing industry average of 20.3x and the peer group average of 23.5x. On simple comparisons, the stock changes hands at a lower earnings multiple than many similar retailers.

A more tailored fair P/E ratio for Dollar General that factors in its industry, margins, size and risks is estimated at 24.2x. This is higher than the current 17.7x level, indicating that the stock would need a higher multiple to align with this framework. Taken together with the earlier cash flow analysis, this points to a market price that may not fully reflect the earnings profile implied by these benchmarks.

On the P/E multiple alone, Dollar General stock appears undervalued relative to what this model suggests investors might typically pay for its earnings.

See what the numbers say about this price — find out in our valuation breakdown.

The Dollar General Narrative: What Would Justify Today's Price?

Simply Wall St Narratives for Dollar General pick up where this valuation puzzle leaves off, spelling out the specific assumptions about Dollar General's future growth, margins and earnings that would need to hold for the stock to be worth materially more or less than today's price, using the Community page as their home. Rather than focusing on a single multiple or model output, each Narrative lays out the key drivers behind its fair value view so you can compare those assumptions with the company’s actual results over time.

Community views on Dollar General are split, with one side focused on expansion and upgrades, and the other highlighting cost and traffic risks.

Bull case: roughly fairly valued

"Remodeling efforts (Project Renovate and Project Elevate), along with expansion of higher-margin nonconsumables and continued development of private label brands, are improving store productivity and encouraging higher basket sizes, helping to drive gross margin expansion and profitable earnings growth…"

Read the full Bull Case to see why Dollar General could be undervalued

Bear case: 35% overvalued

"While shrink improvement is expected, SG&A costs are rising with increased labor expenses and expenses related to planned remodels in 2025; this SG&A pressure without corresponding sales growth can lead to deleveraging and affect operating margins…"

Read the full Bear Case to see why Dollar General could be overvalued

Do you think there's more to the story for Dollar General? Head over to our Community to see what others are saying!

The Bottom Line

Dollar General screens as undervalued on both the Discounted Cash Flow (DCF) intrinsic value estimate and on earnings based multiples, and those two methods are pointing in the same direction. The key question is whether the current discount is compensation for real operational and cost risks or an opportunity if cash flows and margins hold up. From here, what matters most is whether Dollar General can manage shrink, labor and remodel expenses while keeping store traffic and basket sizes healthy, which would be central to whether that apparent discount persists or closes over time.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com