ASML (NasdaqGS:ASML) Stock Could Stay Above Fair Value Following Raised 2026 Outlook

ASML Holding has delivered a strong 157.6% return over the past three years, yet the stock now screens as expensive on broader valuation checks, raising the question of how much of the growth story is already reflected in the share price.

- A 157.6% gain over three years suggests investors have already paid up heavily for ASML Holding's role in advanced chipmaking equipment.

- Rising demand for high numerical aperture EUV tools from large customers can support elevated expectations. At the same time, export controls and shifting chipmaker spending plans may cap how much investors are willing to pay for that growth.

- ASML Holding currently scores 0 of 6 on Simply Wall St's valuation checks, which points to a stock that leans expensive rather than a clear bargain on the broader measures, as shown here.

The issue now is whether ASML Holding's current share price fairly reflects those strong expectations or leaves investors paying too much for future growth.

Does ASML Holding Look Pricey on Earnings?

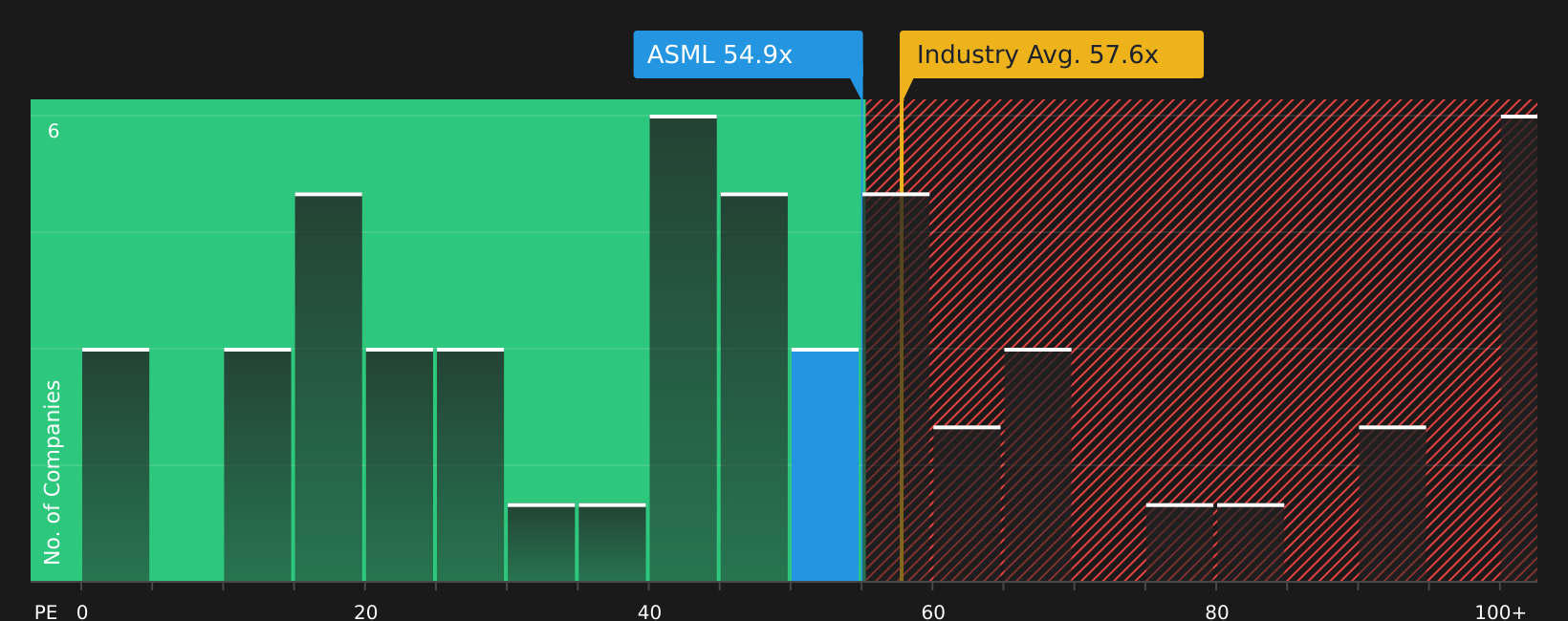

The P/E ratio is a natural fit for ASML Holding because earnings are a key focus for investors watching large, established chip equipment suppliers. ASML Holding currently trades on about 59.1x earnings, which sits slightly above the semiconductor industry average of 58.7x and the peer group average of 56.6x. That puts the stock on a clear premium to many listed chip equipment and semiconductor companies.

The tailored fair P/E ratio for ASML Holding, which tries to account for factors such as margins, size and risk, sits lower at about 51.9x. Against that yardstick, the current multiple implies investors are paying a meaningful premium for the ASML Holding story. Despite recent interest around High NA EUV tools and AI related demand in the news flow, the P/E still points to a stock that already prices in high expectations compared with what the model suggests as a more balanced level.

On the P/E multiple, ASML Holding currently screens as overvalued relative to both its tailored fair ratio and sector benchmarks.

See what the numbers say about this price — find out in our valuation breakdown.

The ASML Holding Narrative: What Would Justify Today's Price?

Simply Wall St Narratives for ASML Holding aim to close the gap between the current P/E premium and what that might imply for ASML Holding's future growth, margins and earnings. Rather than relying on a single multiple or model output, each narrative sets out the assumptions that support its view of fair value so you can compare those expectations with the company’s reported results over time on the Community page.

If you have a number driven view on whether ASML Holding's role in High NA EUV and AI related chip demand supports today's valuation, share a Narrative in the Simply Wall St community and put your assumptions on the record. It is a chance to add your voice on ASML Holding's growth, margins and execution, and then watch how that thesis stacks up as new results and news arrive.

Do you think there's more to the story for ASML Holding? Head over to our Community to see what others are saying!

The Bottom Line

ASML Holding now screens as overvalued on the market multiples used here, with the current P/E premium suggesting expectations already run high. Broader valuation checks also lean weak, so the stock does not stand out as a value idea based on these measures alone. From here, the key question is whether ASML Holding can deliver on the growth and margin profile implied by that premium, or whether the market eventually reins in what it is prepared to pay for the story.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com