Tesla (TSLA) Stock Looks Strong On Returns But Rich On Sales

Tesla stock is back in focus after a strong multi year run, yet the latest valuation checks suggest the shares are pricing in a lot of good news rather than offering clear value.

- Over the last 5 years, Tesla has returned about 77.6%, which puts current buyers in a very different position to investors who entered much earlier.

- Expectations around areas like robotaxis, Optimus and energy storage can support a rich valuation. At the same time, regulatory scrutiny on autonomy and rising competition in EVs may limit how much investors are willing to pay for that story.

- Tesla screens as overvalued on market multiples and scores 0 out of 6 on our broader valuation checks at Simply Wall St, which points to a stock that currently leans expensive rather than a clear bargain.

The issue now is whether Tesla's current share price fairly reflects those growth ambitions or leaves too little margin for disappointment in the years ahead.

Has Tesla Run Too Far on Sales?

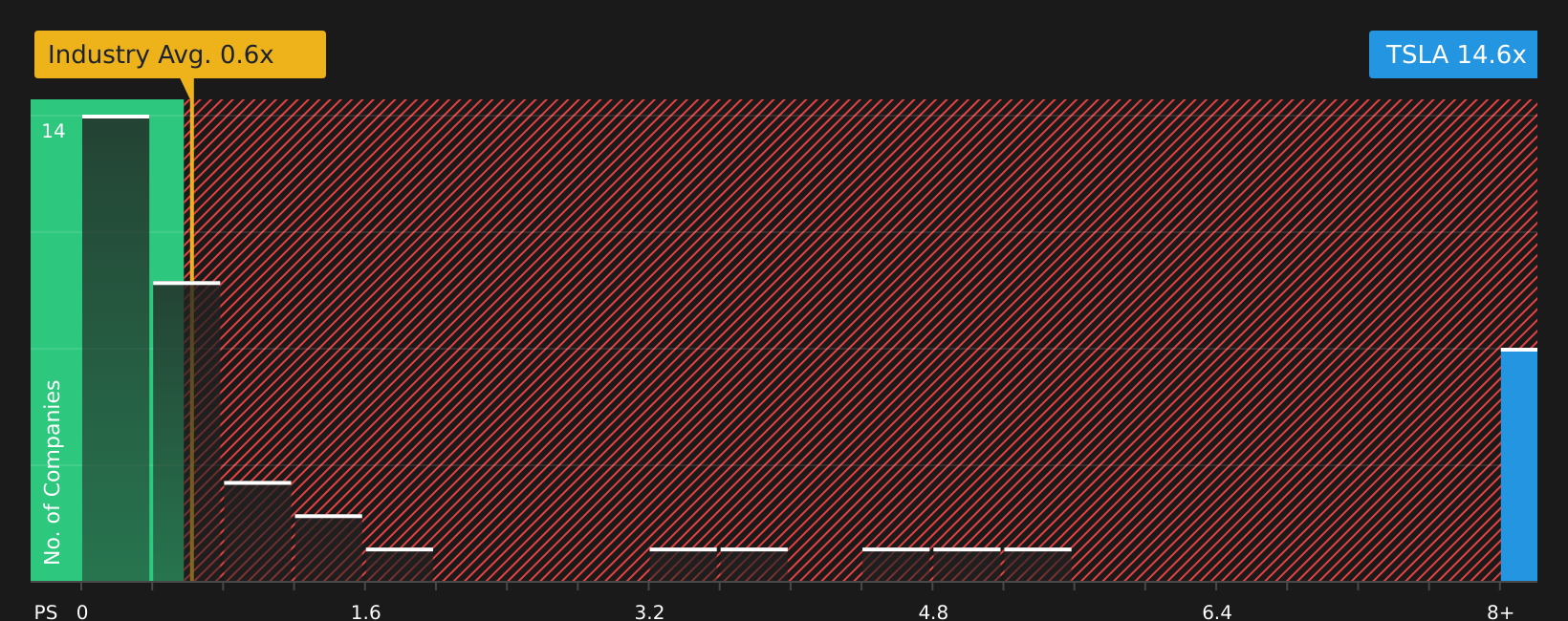

The P/S ratio suits Tesla because a lot of the story investors focus on is still tied to revenue growth across EVs, energy storage and software, not just current earnings. Right now, Tesla trades on a P/S of about 14.6x, compared with an auto industry average of 0.6x and a peer average of about 1.5x, so the stock sits at a very large premium to both traditional carmakers and closer peers.

Our fair P/S ratio of roughly 3.3x is the multiple you might expect for Tesla after considering its sector, size, margins and risk profile. This model comes out far below the current 14.6x because it heavily penalises the uncertainty around how much future profit will emerge from areas like robotaxis and Optimus. Even with recent enthusiasm around Tesla’s Miami robotaxi rollout and strong Q2 deliveries, the valuation still implies investors are paying a high price for that future revenue story today rather than getting it at a discount.

On this P/S framework, Tesla stock screens as clearly overvalued, with the current multiple far above what the fundamentals model supports.

See what the numbers say about this price — find out in our valuation breakdown.

The Tesla Narrative: What Would Justify Today's Price?

Simply Wall St Narratives pick up where the Tesla valuation puzzle above leaves off by spelling out, in plain terms, what specific paths for Tesla's revenue growth, margins and earnings would need to hold for the stock to be worth materially more or less than today's price on Simply Wall St's Community page. Where a single ratio or model gives one headline figure, these frameworks lay out the future that figure assumes, so you can monitor whether Tesla's actual progress still lines up with those embedded expectations.

The Tesla community on Simply Wall St is split between those who see a future "Physical AI" platform and those who see a richly priced case study in market enthusiasm.

Bull case: 43% undervalued

"Just as the iPhone created the App Store economy, Optimus is poised to create the "Labor Economy"...

Read the full Bull Case to see why Tesla could be undervalued

Bear case: 1169% overvalued

"The company’s price-to-earnings ratio sits at around 330x, so it is worth pausing on what this implies...

Read the full Bear Case to see why Tesla could be overvalued

Do you think there's more to the story for Tesla? Head over to our Community to see what others are saying!

The Bottom Line

Tesla looks overvalued on market multiples, with a very wide gap between its current P/S ratio and the level suggested by the tailored fair multiple. That points to a stock where a lot of expected success in robotaxis, Optimus and energy is already embedded in the price, rather than offering much valuation slack. For now, the single assumption that really splits bulls and bears is whether Tesla can turn those ambitious projects into durable, high margin revenue that ultimately justifies such a premium, or whether the multiple simply settles closer to peers as expectations cool.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com