RenaissanceRe (RNR) Stock Still Looks Cheap As Catastrophe Risks Loom

RenaissanceRe Holdings stock has delivered a 124.7% return over the past 5 years, and the current valuation checks indicate that the shares may still be inexpensive relative to the company’s fundamentals.

- RenaissanceRe Holdings' 124.7% 5-year return indicates that long-term holders have already seen solid gains, so any further upside may depend on whether current expectations for the business remain intact.

- For a reinsurer like RenaissanceRe Holdings, the outlook for underwriting profitability and the impact of large loss events can influence how investors are willing to price the stock.

- The company screens as undervalued on most of Simply Wall St's checks, with 5 out of 6 suggesting the shares trade below what the fundamentals may justify.

The key question now is whether RenaissanceRe Holdings' share price already reflects this strong period of returns, or if the current valuation still leaves a reasonable margin of comfort for new capital.

Is RenaissanceRe Holdings a Bargain on Earnings?

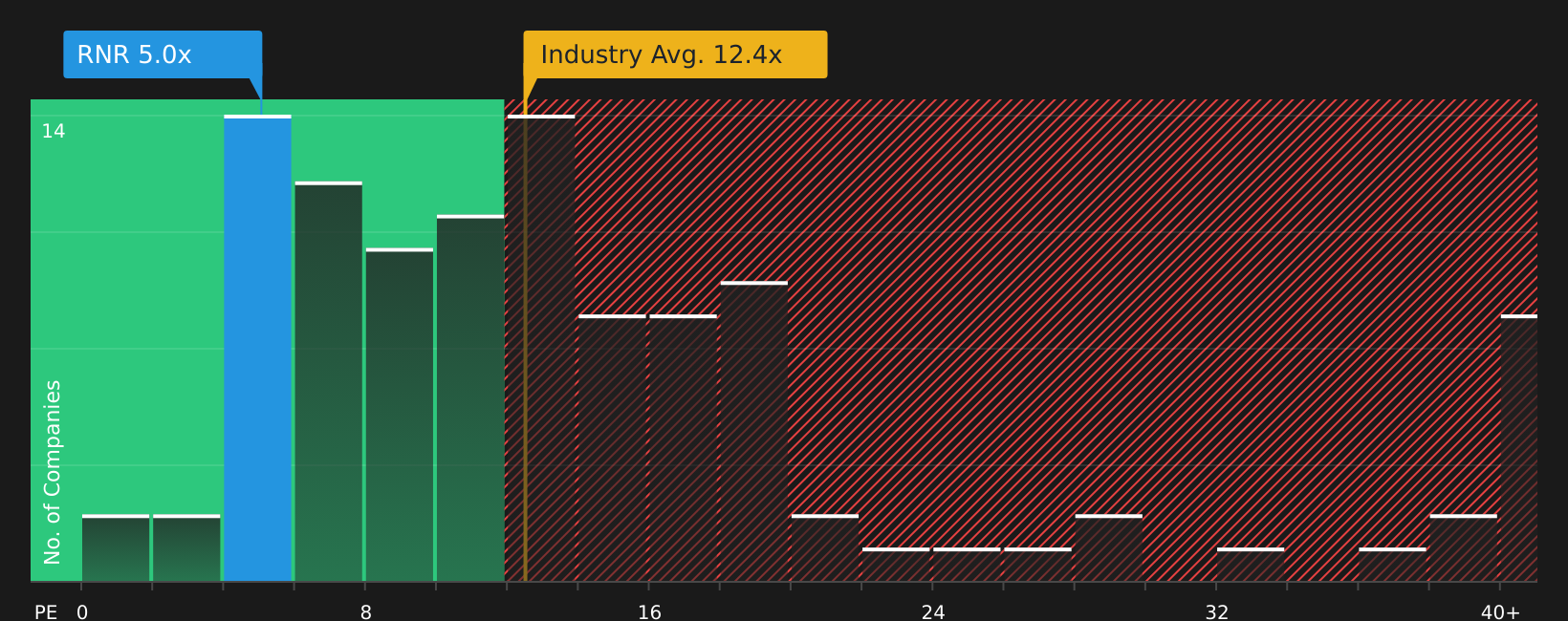

The P/E ratio is a useful way to look at RenaissanceRe Holdings because earnings are a key yardstick for insurers and reinsurers. RenaissanceRe trades on a P/E of about 5.1x, which is below both the Insurance sector average of around 12.2x and the peer group average of 8.4x. That puts the stock on a lower earnings multiple than many comparable insurers.

Simply Wall St’s model suggests a fair P/E ratio of roughly 8.2x for RenaissanceRe Holdings, based on factors such as its sector, earnings profile and risk. Set against that benchmark, the current 5.1x implies the market is pricing the company’s earnings at a discount to what this framework suggests could be reasonable.

On the P/E multiple alone, RenaissanceRe Holdings appears attractively valued relative to both peers and the model’s tailored fair ratio.

See what the numbers say about this price — find out in our valuation breakdown.

The RenaissanceRe Holdings Narrative: What Would Justify Today's Price?

Simply Wall St Narratives for RenaissanceRe Holdings aim to connect the valuation puzzle above with clear, explicit assumptions about what would need to happen to RenaissanceRe Holdings' earnings, growth and margins for the stock to be worth materially more or less than it is today. These narratives sit on the company’s Community page. Each one links its figure to a specific view on how growth, profitability and risk might evolve, giving you a reference point you can revisit as fresh information becomes available.

The RenaissanceRe Holdings community is split between those who see the current setup as roughly fair value with supportive capital returns and those who focus on softer reinsurance pricing and concentration risks.

Bull case: roughly fairly valued

"RenaissanceRe's integrated third-party capital management platform has scaled rapidly, with fee income from capital partners doubling since 2023 and now contributing consistently to earnings with minimal capital requirement..."

Read the full Bull Case to see why RenaissanceRe Holdings could be undervalued

Bear case: 8% overvalued

"The increasing frequency and severity of natural catastrophes driven by accelerating climate change exposes RenaissanceRe to more frequent large loss events, which will erode capital adequacy and depress net earnings despite any advances in modeling or risk selection..."

Read the full Bear Case to see why RenaissanceRe Holdings could be overvalued

Do you think there's more to the story for RenaissanceRe Holdings? Head over to our Community to see what others are saying!

The Bottom Line

RenaissanceRe Holdings screens as undervalued on earnings multiples, with the current P/E sitting below both sector and peer averages as well as the tailored fair ratio. For you as an investor, the key question is whether this discount reflects undue caution or a reasonable buffer for underwriting and catastrophe risk. The key issue is whether RenaissanceRe Holdings can sustain earnings that justify a re rating of the P/E, or whether concerns about large loss events and reinsurance pricing keep the stock anchored where it is.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com