Is Bank of N.T. Butterfield & Son (NTB) Fully Valued Or Still Cheap?

Bank of N.T. Butterfield & Son (NYSE:NTB) has drawn attention after recent trading left the stock at a last close of US$61.37. This has invited investors to weigh its current valuation and fundamental profile.

See our latest analysis for Bank of N.T. Butterfield & Son.

For context, Bank of N.T. Butterfield & Son's share price has eased 1.71% over the last day but is still up 5.70% over 30 days and 23.48% year to date. Its 1 year total shareholder return of 39.58% and 5 year total shareholder return of 133.55% point to momentum that has built over time rather than faded recently.

If Bank of N.T. Butterfield & Son is already on your radar, this could be a good moment to broaden your watchlist with 18 top founder-led companies

The stock now sits almost exactly in line with analyst targets, yet still appears to trade at a wide discount to some intrinsic value estimates. Is the market’s caution on Bank of N.T. Butterfield & Son misplaced or well earned?

Most Popular Narrative: 10% Overvalued

At a last close of $61.37, Bank of N.T. Butterfield & Son sits slightly above the most followed fair value estimate of $61.33, which is built on detailed earnings and cash flow projections using a 7.11% discount rate.

Continued expansion and tailored offerings in high-growth international wealth management and private trust sectors (e.g., in the Channel Islands, Bahamas, Switzerland, and Singapore) position Butterfield to benefit from the ongoing increase in global wealth among high-net-worth clients, supporting fee-based revenue growth and higher net margins. Butterfield's strong reputation as a market leader in regulated offshore banking jurisdictions (such as Bermuda and the Cayman Islands), combined with heightened global regulatory scrutiny, is likely to attract high-quality clients seeking transparency and compliance, contributing to deposit growth and a more stable revenue base.

Want to see what sits behind that $61.33 fair value for Bank of N.T. Butterfield & Son? The narrative leans on faster revenue growth, changing profit margins and a lower future earnings multiple than many peers. Curious how those moving parts come together across the next few years and what they imply for shareholder returns versus today’s price?

Result: Fair Value of $61.33 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, Bank of N.T. Butterfield & Son's reliance on large, potentially non sticky deposits, along with its exposure to island economies tied to tourism, could still upset that fair value story.

Find out about the key risks to this Bank of N.T. Butterfield & Son narrative.

Another View: What Market Ratios Say About Bank of N.T. Butterfield & Son

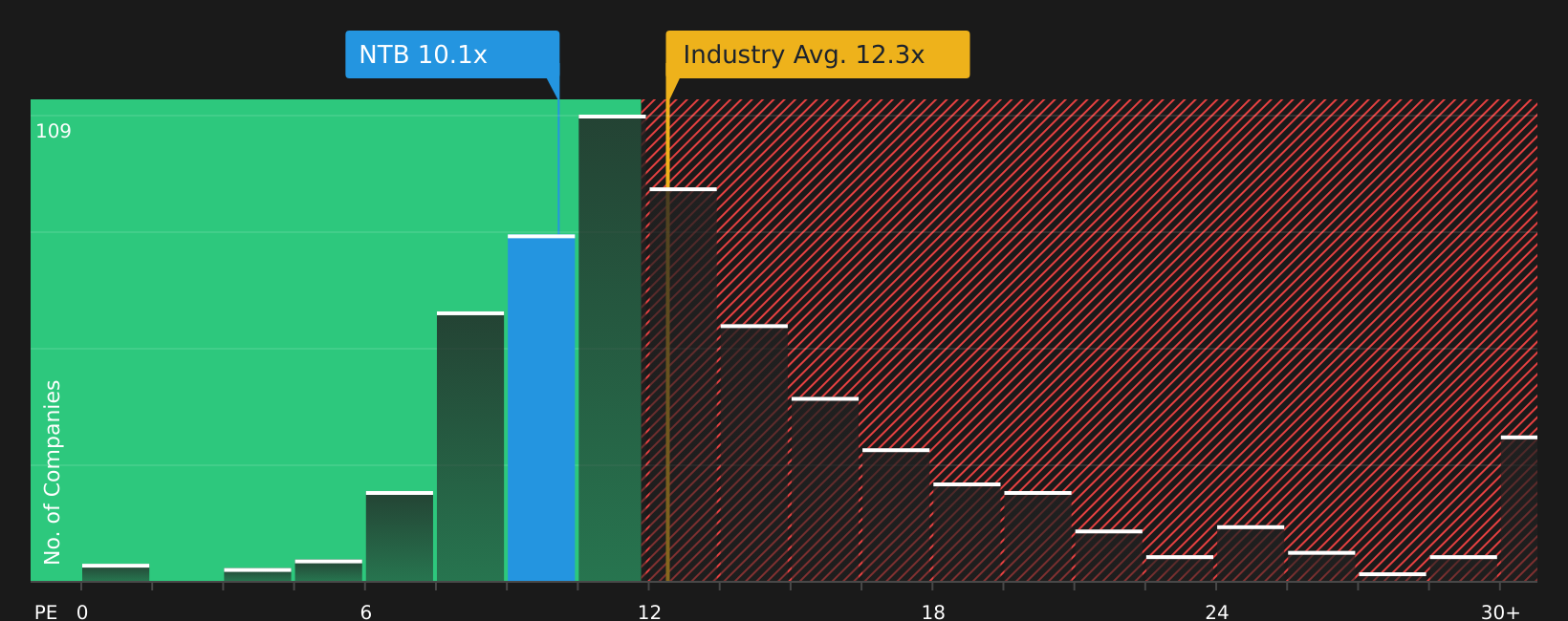

While the most followed narrative frames Bank of N.T. Butterfield & Son as about 10% overvalued against a $61.33 fair value, the current P/E of 10.1x tells a different story. It sits below the US Banks industry at 12.5x, below peer average at 13.7x, and below a 14.3x fair ratio. This implies the market is pricing in extra risk. Is that caution excessive or justified by the bank’s specific credit and deposit profile?

See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

Mixed messages on Bank of N.T. Butterfield & Son's valuation and risk-reward trade off so far? Take a closer look at the full risk and reward profile before the market mood shifts and ground your own view in the 5 key rewards and 3 important warning signs.

Looking for more investment ideas beyond Bank of N.T. Butterfield & Son?

If you stop at Bank of N.T. Butterfield & Son, you could miss other opportunities that better match your goals, risk comfort, and income needs.

- Scan for quality at a discount by checking companies in the 47 high quality undervalued stocks that pair stronger fundamentals with prices that may not fully reflect them yet.

- Strengthen your income stream by reviewing the 8 dividend fortresses and focus on businesses that seek to combine higher yields with more resilient cash flows.

- Sleep easier at night by studying stocks in the 84 resilient stocks with low risk scores where balance sheets, earnings profiles, and risk scores suggest more resilience across different market conditions.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com