Is Nasdaq (NDAQ) Above Fair Value After Rising 88% In Three Years?

Nasdaq stock has delivered a strong 88.3% return over the past three years. However, both the Excess Returns intrinsic value estimate and the market multiple checks currently point to the shares trading at a premium rather than as a clear bargain.

- Nasdaq's 88.3% gain over three years highlights how much expectations have risen. This raises the bar for what counts as good value today.

- Growing interest from international companies seeking U.S. listings can support Nasdaq's potential earnings over a longer horizon. At the same time, regulatory decisions around listing standards and trading rules may influence how much investors are willing to pay for that growth.

- With a value score of 2 out of 6, Nasdaq screens as leaning expensive rather than offering broad based cheapness on the core valuation checks.

The key question now is whether Nasdaq's current share price already reflects these strengths, or if the premium suggested by both the intrinsic value estimate and earnings multiples leaves limited room for further upside.

Is Nasdaq Getting Expensive on Excess Returns?

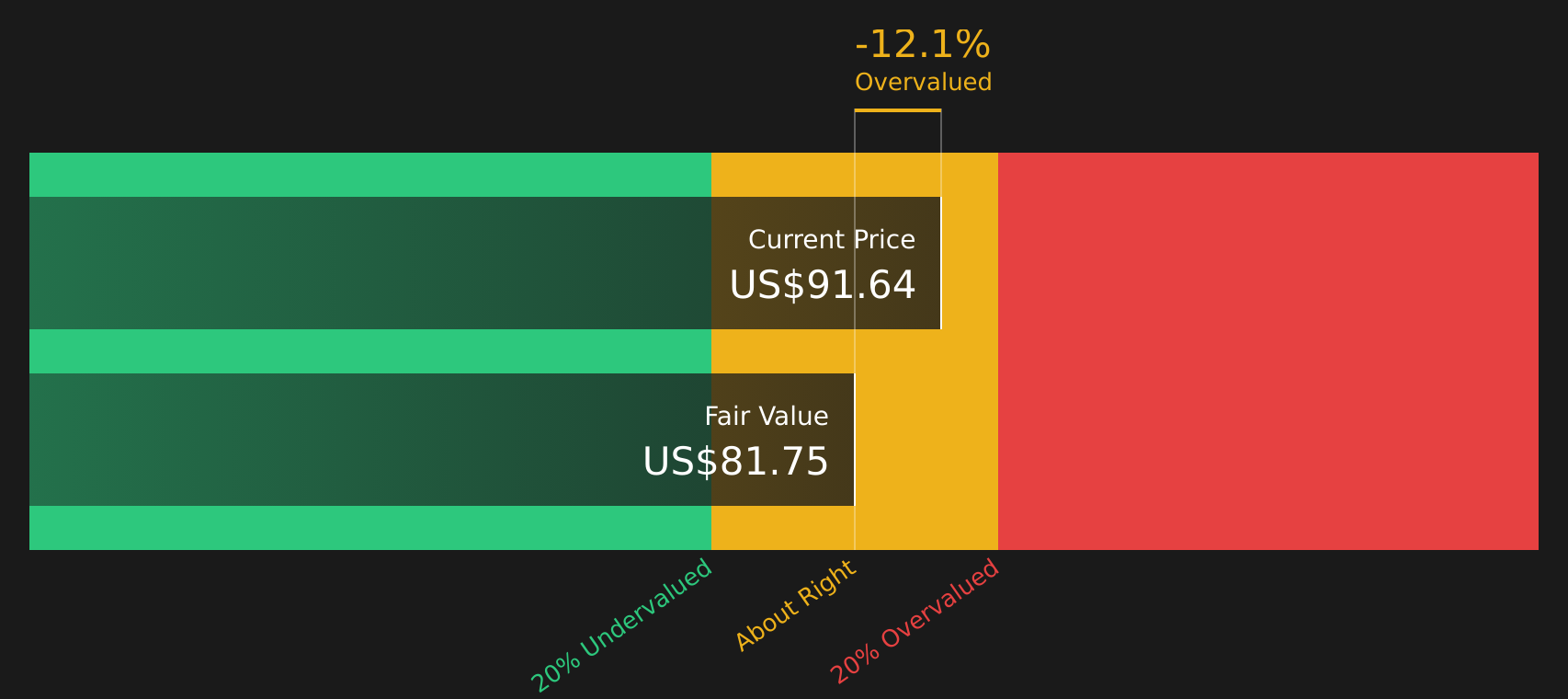

The Excess Returns model looks at how efficiently Nasdaq is expected to generate profits on its equity base over time relative to the return investors require. For Nasdaq, the inputs point to a mature but still profitable franchise, with stable earnings power rather than a high growth story.

The model uses a Book Value of $21.31 per share and a Stable EPS of $4.59 per share, compared with a Cost of Equity of $1.88 per share. That gap supports an Excess Return of $2.71 per share, built on an Average Return on Equity of 19.90% and a Stable Book Value of $23.05 per share. On these assumptions, the Excess Returns framework arrives at an intrinsic value of $81.64 per share, which is below the current market price and implies the stock screens as 12.2% overvalued.

Because recent analyst optimism has focused on Nasdaq’s ability to grow earnings through new market opportunities, the current premium suggests investors are already paying up for that potential.

On this Excess Returns view, Nasdaq stock currently looks overvalued relative to its modeled earnings power.

Our Excess Returns analysis suggests Nasdaq may be overvalued by 12.2%. Discover 47 high quality undervalued stocks or create your own screener to find better value opportunities.

Does Nasdaq Look Pricey on Earnings?

The P/E multiple is a useful way to think about what you are paying today for each dollar of Nasdaq earnings. Nasdaq currently trades at a P/E of 27.1x, which is below the Capital Markets industry average of 39.6x and also below the peer group average of 35.6x.

However, a more tailored fair P/E for Nasdaq, which factors in its size, risk profile and profitability, is estimated at 17.3x. That is materially under the current 27.1x. Even though the stock sits at a discount to broad industry and peer averages, it still screens as expensive relative to what this framework suggests would be a more grounded earnings multiple.

On this P/E view, Nasdaq stock appears overvalued relative to the earnings multiple indicated by the fair ratio model.

See what the numbers say about this price — find out in our valuation breakdown.

The Nasdaq Narrative: What Would Justify Today's Price?

Simply Wall St Narratives for Nasdaq pick up where the valuation puzzle leaves off by spelling out which growth, margin and earnings paths would need to play out for Nasdaq's stock to be worth materially more or less than today's price, as set out on the Community page. Rather than relying on a single multiple or model, each Narrative lays out its own fair value assumptions so you can compare them with Nasdaq's actual results over time.

Want to add your voice to the Nasdaq story? Share a Narrative that sets out your number driven case on whether developments like SK Hynix's record US$26.5b ADR listing on Nasdaq or the recent delisting decisions support where you think Nasdaq's growth, margins and execution go from here, and then track how that thesis holds up as new results and news are released.

Do you think there's more to the story for Nasdaq? Head over to our Community to see what others are saying!

The Bottom Line

For Nasdaq, both the Excess Returns intrinsic value estimate and the tailored P/E indicate the stock is overvalued, with current pricing already reflecting much of the anticipated earnings power. The broader checks behind the low value score also lean cautious rather than supportive. From here, the key question for investors is whether Nasdaq can maintain earnings quality and growth that are strong enough to justify that premium, or whether the market eventually settles on a lower multiple for the same cash flows.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com