Is Host Hotels & Resorts (HST) Stock Stretched Or Reasonable Today?

Host Hotels & Resorts has delivered a 92.6% return over the past five years, yet both the Discounted Cash Flow (DCF) intrinsic value estimate and market multiple checks currently point to the stock trading at a discount to what its fundamentals may justify. That mix of strong long term performance and an apparent valuation gap is drawing attention to whether the current share price of US$23.94 still leaves room for further upside.

- The 92.6% five year return suggests long term shareholders in Host Hotels & Resorts have already seen substantial gains, which makes the current discount signal from valuation models more striking.

- Expectations that Host Hotels & Resorts can continue to convert its hotel portfolio into steady cash flows may support the intrinsic value, while any pressure on occupancy, room rates, or financing costs could weigh on what investors are willing to pay.

- On Simply Wall St's checks, Host Hotels & Resorts screens as undervalued in 4 of 6 valuation tests, giving a mixed overall picture rather than a clear cut bargain.

The issue now is whether that combination of a 32.4% discount to intrinsic value and a solid multi year share price run leaves Host Hotels & Resorts attractively priced for investors coming to the stock today.

Is Host Hotels & Resorts Still Cheap on Cash Flow?

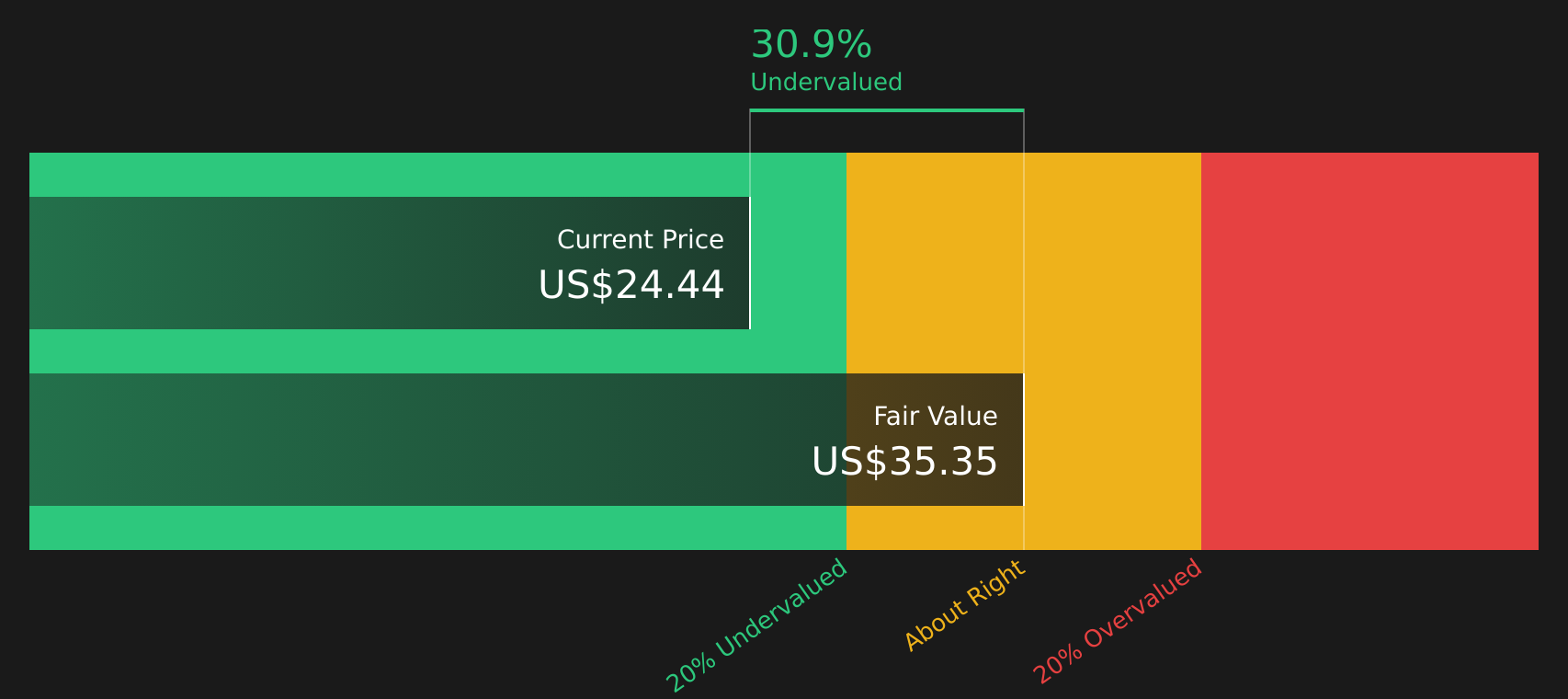

The Discounted Cash Flow (DCF) model here uses adjusted funds from operations to estimate what Host Hotels & Resorts might be worth based on its future cash generation. The latest twelve month free cash flow is reported at $1.44b, and the forecast path assumes broadly stable to growing cash flows over time rather than sharp swings.

Feeding those projections into the two stage model produces an intrinsic value estimate of about $35 per share, compared with the current share price of $23.94. That gap implies the stock is trading at roughly a 32.4% discount to the value implied by its cash flows. This suggests the market is valuing Host Hotels & Resorts more cautiously than this cash flow based model.

On this DCF view, Host Hotels & Resorts stock appears inexpensive relative to the cash flows analysts expect it to produce.

Our Discounted Cash Flow (DCF) analysis suggests Host Hotels & Resorts is undervalued by 32.4%. Track this in your watchlist or portfolio, or discover 47 more high quality undervalued stocks.

Is Host Hotels & Resorts a Bargain on Earnings?

P/E is a useful reference point for Host Hotels & Resorts because earnings remain a key anchor for how REIT stocks are often evaluated alongside cash flows. Host Hotels & Resorts currently trades on a P/E of about 16.2x, which sits above the Hotel and Resort REITs industry average of 14.7x but below the peer group average of 27.5x.

The Fair Ratio model, which adjusts for factors such as growth profile, margins, scale and risk, points to a P/E of about 28.3x for Host Hotels & Resorts. Set against the current 16.2x, that suggests the stock trades at a sizeable discount to what this framework indicates might be reasonable, even though it is not the lowest valued company in its sector on simple averages alone.

On this P/E measure, Host Hotels & Resorts stock appears undervalued compared with the multiple implied by its fundamentals and peer context.

See what the numbers say about this price — find out in our valuation breakdown.

The Host Hotels & Resorts Narrative: What Would Justify Today's Price?

Simply Wall St Narratives for Host Hotels & Resorts pick up where this valuation puzzle leaves off. They spell out which paths for Host Hotels & Resorts' growth, margins and earnings would make the stock worth significantly more or less than today's price. Rather than relying on a single multiple or model, each narrative lays out the assumptions behind its fair value so you can weigh them against Host Hotels & Resorts' results as new data arrives, all within Simply Wall St's Community page.

Community views on Host Hotels & Resorts sit on a wide spectrum, from cautious upside to concern that recent strength already prices in a lot of good news.

Bull case: roughly fairly valued

"Prudent balance sheet management, with low leverage and ample liquidity, positions Host to continue capital recycling, share buybacks, and accretive reinvestment…"

Read the full Bull Case to see why Host Hotels & Resorts could be undervalued

Bear case: 14% overvalued

"Host Hotels & Resorts anticipates a 6% increase in wage and benefit expenses in 2025, impacting overall hotel operating expenses and placing downward pressure on net margins…"

Read the full Bear Case to see why Host Hotels & Resorts could be overvalued

Do you think there's more to the story for Host Hotels & Resorts? Head over to our Community to see what others are saying!

The Bottom Line

For Host Hotels & Resorts, both the Discounted Cash Flow (DCF) intrinsic value view and the P/E based Fair Ratio model suggest the stock may be undervalued rather than fully priced. The broader checks are mixed rather than overwhelmingly strong, so the apparent discount is not a one way signal. The central issue for investors is whether Host Hotels & Resorts can sustain the cash generation and earnings profile that these models assume, despite cost pressures and any shifts in demand. If those fundamentals hold up, the current gap between intrinsic value and share price becomes the key consideration, rather than recent share price history.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com