Is United Bankshares (UBSI) Fully Valued As Softer Inflation Lifts Rate Cut Hopes?

Softer than expected inflation data prompted investors to reassess interest rate expectations, and United Bankshares (UBSI) moved higher alongside regional peers as markets evaluated the potential for relief on funding costs and loan demand.

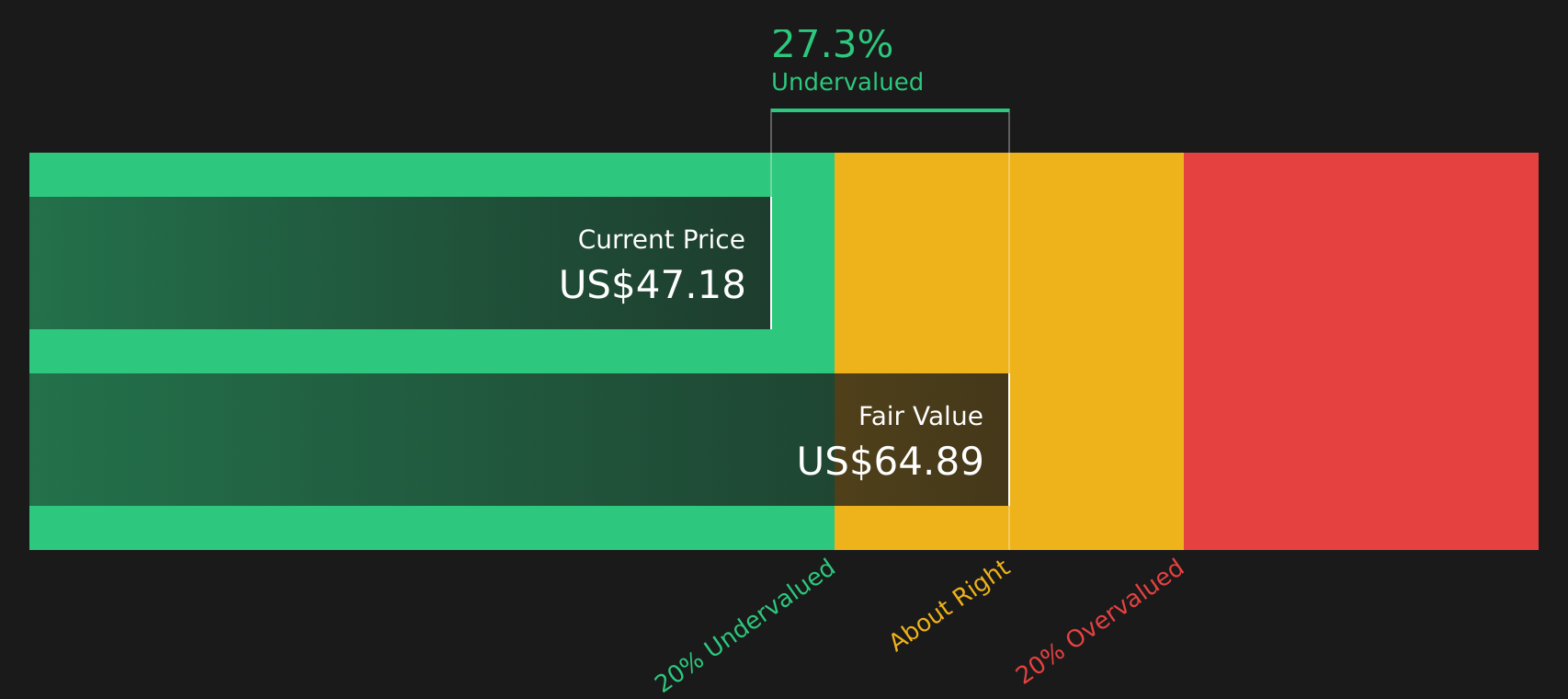

See our latest analysis for United Bankshares.

At a share price of $47.58, United Bankshares has a 1 month share price return of 7.67% and a year to date share price return of 23.94%. The 1 year total shareholder return of 32.45% and 5 year total shareholder return of 69.99% highlight the momentum that recent inflation and interest rate headlines have brought back into focus.

If the recent move in United Bankshares has you thinking about what else could benefit from changing rate expectations, it may be worth scanning 18 top founder-led companies

After United Bankshares' sharp move, the stock now sits only slightly below the average analyst target while some intrinsic value estimates imply a wider discount, so how far from fair value does the current price really look?

Price-to-Earnings of 13x: Is it justified?

On one hand, United Bankshares screens as good value on some models, with the SWS DCF model suggesting the stock is trading at a discount to an estimated future cash flow value of $64.89 and a separate fair value estimate implying it is trading 26.7% below that level. On the other hand, at a last close of $47.58, the stock is trading on a P/E of 13x, slightly above both its estimated fair P/E of 11.9x and the 12.5x average for the US Banks industry.

The P/E ratio compares the current share price to earnings per share and is a common way investors compare banks with relatively steady profit profiles. For United Bankshares, a 13x P/E suggests the market is willing to pay a modest premium for each dollar of current earnings, even though earnings and revenue growth expectations are described as slower than the broader US market and below the 20% threshold often associated with high growth.

Against peers, United Bankshares looks mixed, with its 13x P/E above the US Banks industry average of 12.5x yet below the peer group average of 16.4x. This could indicate the stock sits between a sector level valuation and what similar sized companies trade at. Compared to the estimated fair P/E of 11.9x, the current multiple is higher, a level the market could move towards if sentiment or growth expectations cool from here.

Explore the SWS fair ratio for United Bankshares

Result: Price-to-Earnings of 13x (ABOUT RIGHT)

However, the United Bankshares story could be tested if funding pressures squeeze margins further or if loan demand weakens more than markets currently anticipate.

Find out about the key risks to this United Bankshares narrative.

Another View on United Bankshares' Value

While the P/E comparison shows United Bankshares as only slightly above its fair ratio of 11.9x and the US Banks industry at 12.5x, the SWS DCF model offers a different lens, with a future cash flow value of $64.89 that sits well above the current $47.58 share price. That kind of gap can look appealing, but also raises a simple question: which view should carry more weight for you?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out United Bankshares for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 47 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If the mixed signals around United Bankshares have you uncertain, this is a good time to review the numbers yourself and form your own assessment by weighing the company's 3 key rewards

Looking for more investment ideas beyond United Bankshares?

If United Bankshares sharpened your focus, do not stop here. The same tools that surfaced this opportunity can help you spot others before they land on everyone else's radar.

- Spot potential overreactions by reviewing 20 elite penny stocks with strong financials that pair smaller market sizes with financials you can actually analyze.

- Target quality at a discount by scanning screener containing 20 high quality undiscovered gems that combine solid fundamentals with limited mainstream attention.

- Prioritize resilience by filtering for 84 resilient stocks with low risk scores that may better suit a portfolio built for steadier conditions.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com