Japanese Growth Stocks With High Insider Ownership That Investors May Want To Track

Global inflation is easing in several regions, rate expectations are shifting, and energy and commodity prices are still shaping costs for companies and consumers. In this kind of cross current, many investors are looking for stocks where growth expectations are supported not only by analysts but also by company insiders who keep meaningful stakes in their own businesses. This Fast Growing Stocks With High Insider Ownership screener focuses on exactly that combination, aiming to highlight companies where management’s interests are closely aligned with shareholders. In this article, you will see 3 of the stocks that currently pass this filter.

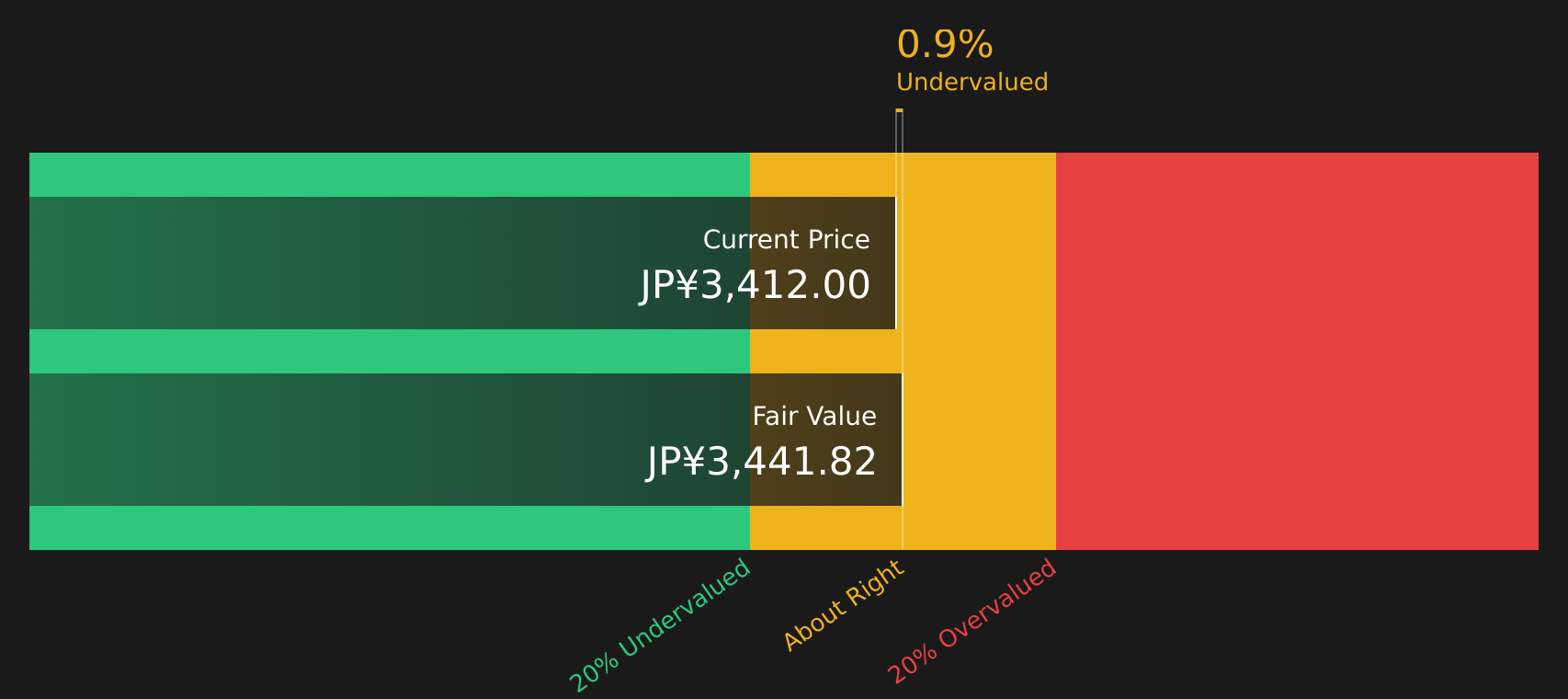

Capcom (TSE:9697)

Overview: Capcom is a Japanese video game publisher that creates, sells, and distributes home console and mobile games such as action and horror franchises, while also running arcade venues, supplying amusement machines, and licensing its characters across various entertainment formats worldwide.

Operations: Capcom generates the bulk of its revenue from Digital Content at ¥144,277m, with additional contributions from Arcade Operations at ¥25,656m, Amusement Equipment at ¥17,780m, and Other activities at ¥7,650m, supported by a geographically balanced mix across Japan, the United States, Europe, and other regions.

Market Cap: ¥1.43t

Capcom may appeal to investors who focus on growth alongside insider commitment. Its digital games business combines profitability and forecast returns on equity of around 20%, supported by globally known franchises such as Resident Evil, Monster Hunter, and Street Fighter, which can accommodate recurring releases and expansions. At the same time, the stock trades close to one DCF-based fair value estimate and on a higher P/E than many domestic peers, which suggests that current expectations already reflect continued execution. Investors weighing this profile might consider the combination of forecast earnings and revenue growth relative to the wider Japanese market and a rising dividend profile, alongside factors such as non-cash earnings, reliance on external borrowing, and concentration in a few key franchises. The overall picture includes both an appealing growth narrative and a set of notable risks.

Capcom’s globally recognised franchises and forecast 20% returns on equity are only half the story. The real question is whether expectations are already stretched or still underappreciating the analyst forecasts for Capcom

Lasertec (TSE:6920)

Overview: Lasertec designs and sells highly specialized inspection and measurement equipment that chipmakers and electronics manufacturers use to check wafers, photomasks, and materials for defects, particularly in advanced semiconductor production. Its tools sit in critical steps of the manufacturing process, helping customers maintain yield and reliability as chip designs become more complex.

Operations: Lasertec generates all of its ¥252,181m in revenue from designing, manufacturing, and selling inspection and measurement equipment, with sales spread across Japan, Europe, Taiwan, South Korea, other parts of Asia, and the United States.

Market Cap: ¥3.75t

Investors considering fast growing companies with aligned management may find Lasertec worth a closer look. The company reports high quality earnings, a 35.2% net margin, and a 39.4% return on equity, alongside earnings growth that has averaged 33.8% per year over five years. Revenue and profit for the recent nine month period both increased year on year, and the stock has attracted attention during tech led rallies, which indicates investor interest in its role in semiconductor tooling. At the same time, a P/E above the broader industry, a price that sits above one cash flow based value estimate, high share price volatility, and reliance on external borrowing all mean the growth profile comes with meaningful risk trade offs.

Lasertec’s rapid earnings expansion and premium P/E suggest that the market is pricing in a big future, but not every investor is weighing the analyst forecasts for Lasertec that could explain or challenge that confidence

Rakuten Group (TSE:4755)

Overview: Rakuten Group is a Japanese platform company that brings together e-commerce, fintech, mobile and digital content services, running everything from online shopping and travel booking to credit cards, banking, securities, insurance, payments and mobile telecoms in Japan and abroad.

Operations: Rakuten Group generates revenue primarily from Internet Services at ¥1.38t, FinTech at ¥1.03t, and Mobile at ¥503.3b, partly offset by ¥335.4b of intercompany transactions and other items.

Market Cap: ¥1.74t

Rakuten Group is interesting for investors because it is trying to turn a large ecosystem of shoppers, cardholders and mobile users into a single data driven platform, while earnings are still in the red and funded entirely by external borrowing. Forecast revenue growth in the mid single digits and a move from losses to profit over the next few years sit alongside plans to reorganize the FinTech arm, push AI cost savings and use partnerships in telecoms and cloud to lift margins. At the same time, the mobile segment’s path to profitability, reliance on partners and ongoing net losses highlight real execution and balance sheet risk, which is exactly what makes the current valuation debate around Rakuten Group so contested.

Rakuten Group’s push to turn a loss making ecosystem into a unified profit engine is only part of the picture; the real question is whether the market is misreading the analyst forecasts for Rakuten Group

The three stocks in this article are only a starting point, and the full Fast Growing Stocks With High Insider Ownership screen uncovers 92 more companies with equally compelling insider backed growth stories you can review through the Fast Growing Stocks With High Insider Ownership screener. Use Simply Wall St to identify, filter, and analyze the specific catalysts and narratives that matter to you so you can focus on the highest conviction growth and insider ownership combinations.

Take Control of Your Investment Journey

If Rakuten Group or any of these companies have caught your attention, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value and track any new developments as they happen. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Beyond These Stocks?

New ideas can move quickly, and the most interesting stocks often gain momentum before they hit everyone’s radar. Scan these focused shortlists while it matters and get in early.

- Spot potential cash rich opportunities before momentum takes off by reviewing the curated 17 high quality undervalued stocks that currently combine quality with what may be cheaper entry points.

- Ride long term income themes by checking the carefully filtered 46 dividend fortresses that aim to pair higher yields with businesses focused on maintaining their payouts.

- Get ahead of long cycle infrastructure and energy shifts by researching the targeted 90 nuclear energy infrastructure stocks that concentrate on companies tied to potential power grid upgrades.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com