Ferrotec (TSE:6890) After A 26% Monthly Slide, Is Its 24.7x P E Still Fair?

Ferrotec stock performance overview

Ferrotec (TSE:6890) has been on the radar for investors after a sharp 12.4% one day decline, extending its slide of about 22.9% over the past week and 25.7% over the past month.

Despite this recent weakness, the stock remains higher over the past 3 months and has recorded gains year to date, over the past year, 3 years and 5 years. This invites closer attention to what might be priced in now.

See our latest analysis for Ferrotec.

The recent pullback in Ferrotec’s share price, with a 1 day share price return of down 12.4% and a 30 day share price return of down 25.7%, contrasts with its 36.4% year to date share price return and very strong 1 year total shareholder return of 95.2%. This suggests that momentum has cooled in the short term, while longer term holders have still seen substantial gains.

If you are reassessing chip related opportunities after Ferrotec’s volatility, it could be a good moment to widen your search using our screener of 53 AI infrastructure stocks

After a drop like Ferrotec has just seen, yet with multi-year returns still strong, the question is whether the current valuation compensates you for the risks that are now clearer.

Preferred P/E multiple for Ferrotec: Is it justified?

With Ferrotec closing at ¥7,010 and trading on a P/E of 24.7x, the stock is priced slightly below both peer and industry averages on this earnings measure.

The P/E multiple compares the current share price to earnings per share and is widely used for semiconductor stocks, where profits are a key focus for investors. For Ferrotec, this lens matters because earnings are forecast to grow 13.1% per year, ahead of the broader JP market forecast of 10.1% per year, even though that growth is not classified as very high.

On current numbers, Ferrotec is described as trading at good value relative to peers and the wider JP semiconductor industry. Its 24.7x P/E is lower than both the industry average of 26.9x and the peer average of 29.3x. Our fair P/E estimate of 28.6x also sits above the current multiple, which points to a level the market could potentially move toward if earnings forecasts and sentiment toward the company hold.

Explore the SWS fair ratio for Ferrotec

Result: Price-to-earnings of 24.7x (ABOUT RIGHT)

However, Ferrotec’s story could change quickly if semiconductor demand cools or if earnings growth, currently forecast at 13.1% a year, falls short of expectations.

Find out about the key risks to this Ferrotec narrative.

Another view on Ferrotec's value

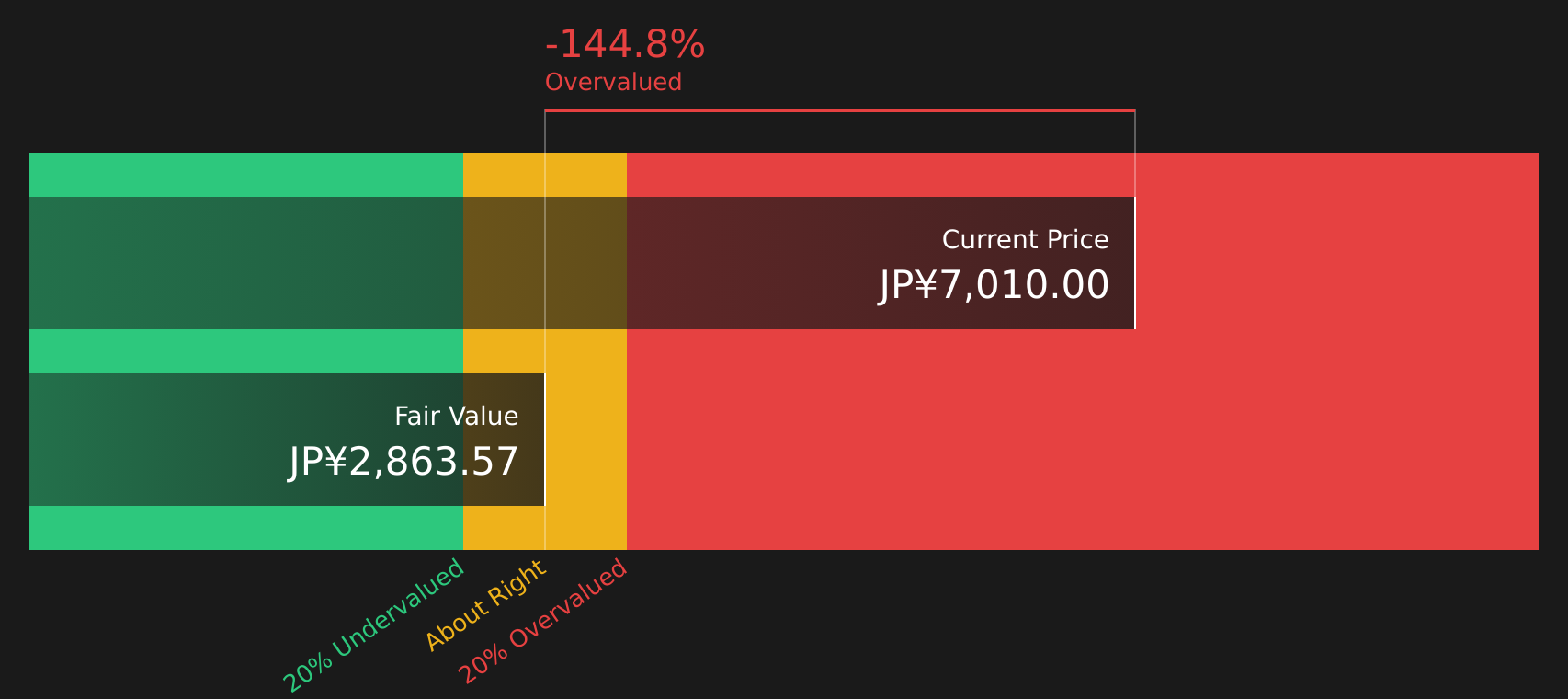

While Ferrotec’s 24.7x P/E looks reasonable against peers, the SWS DCF model tells a different story. On that measure, the current share price of ¥7,010 sits well above an estimated future cash flow value of ¥2,863.57. This points to the stock looking expensive on cash flow assumptions.

That gap highlights a simple question for investors: are earnings-based comparisons or long term cash flow estimates the better guide for judging Ferrotec at today’s price?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Ferrotec for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 17 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With mixed signals around Ferrotec’s recent moves, it makes sense to look past the headlines, carefully weigh the trade off between concerns and optimism, and review the 3 key rewards and 2 important warning signs.

Looking for more investment ideas beyond Ferrotec?

If Ferrotec has sharpened your focus on opportunities, do not stop here. Expanding your watchlist can help you spot more setups before the crowd reacts.

- Target resilience with companies that combine prudent leverage and robust fundamentals using the solid balance sheet and fundamentals stocks screener (37 results).

- Hunt for quality at a sensible price by scanning our list of 17 high quality undervalued stocks.

- Spot potential future standouts early by tracking the screener containing 60 high quality undiscovered gems.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com