Vericel (VCEL) Stock Looks Stretched On Earnings While Its 32% Return Stays Strong

Vericel stock has delivered a 32.0% return over the past year, yet its current valuation checks lean expensive, raising the question of how much of the story is already reflected in the share price.

- Over the last 1 year, Vericel has returned 32.0%. This puts recent shareholder gains front and center in any discussion of what the stock is worth today.

- For a company like Vericel, expectations around sustaining growth in its therapies can support the current pricing. However, any setback in execution or profitability may quickly pressure how much investors are willing to pay.

- With a value score of 1 out of 6, Vericel does not screen as a clear bargain on the broader valuation checks.

The issue now is whether Vericel's recent share price strength leaves enough valuation cushion if the business underdelivers against current expectations.

Find out why Vericel's 32.0% return over the last year is lagging behind its peers.

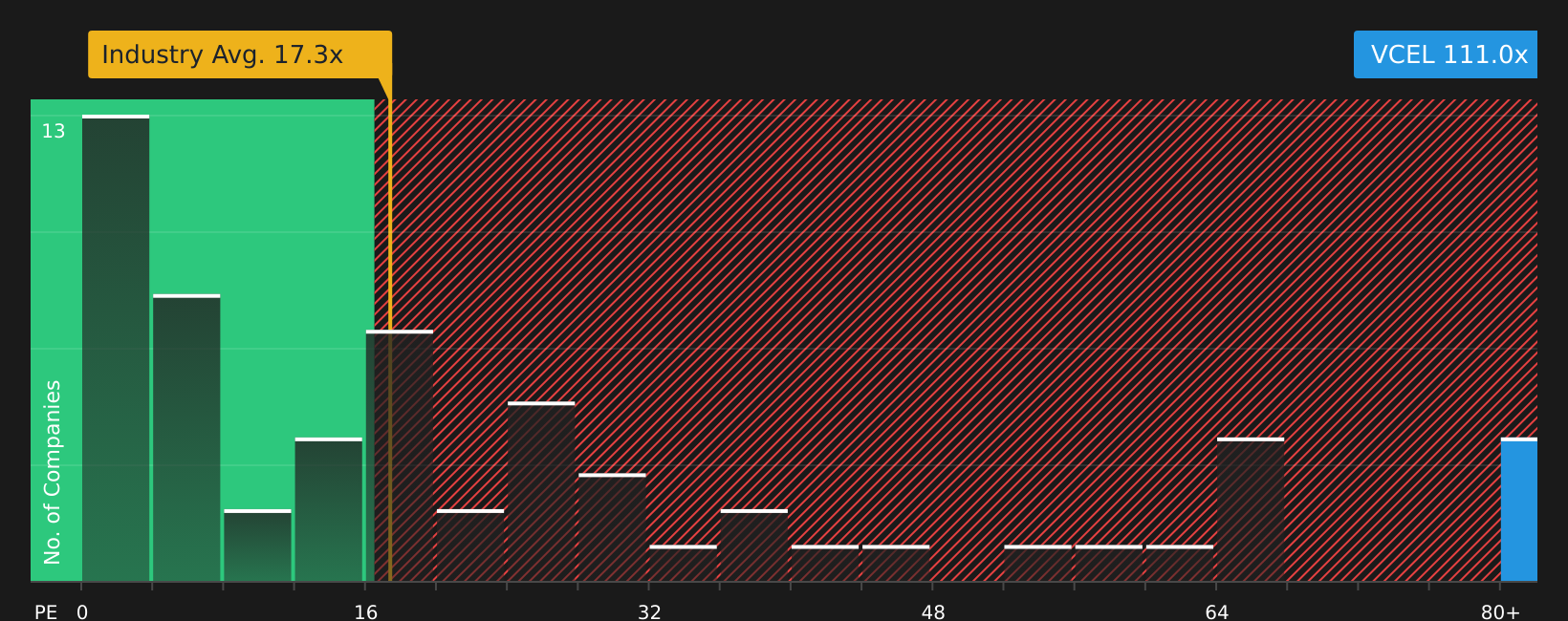

Does Vericel Look Pricey on Earnings?

P/E is a useful lens for Vericel because the company is generating earnings that can be compared directly to what investors are paying for each dollar of profit. Vericel currently trades on a P/E of about 111.0x, which is far above the Biotechs industry average of 17.3x and also well ahead of the peer group average of 16.1x. That means investors are paying a much higher price for Vericel earnings than for many other profitable biotech stocks.

The fair P/E ratio implied by the broader checks is about 29.0x, and the gap to the current 111.0x level is very wide. The model is heavily penalising Vericel for its risk profile and cash flow characteristics. As a result, this fair value marker is better viewed as a signal that the stock screens as very expensive on earnings, rather than a pinpoint target. For you as an investor, it suggests that a lot is already being asked of Vericel’s future performance to justify today’s earnings multiple.

On a P/E basis, Vericel stock currently looks overvalued relative to both its own fair multiple and the wider biotech sector.

See what the numbers say about this price — find out in our valuation breakdown.

The Vericel Narrative: What Would Justify Today's Price?

Simply Wall St Narratives for Vericel pick up where this valuation puzzle leaves off by spelling out which assumptions about Vericel's growth, margins and earnings would need to hold for the stock to be worth materially more or less than its current price. Each narrative ties a fair value estimate to a specific mix of potential catalysts and risks, so you can see over time which version of Vericel's story appears to be taking shape on the Community page.

Community views on Vericel sit far apart, with some investors seeing a growing cell therapy platform and others focused on execution and cost risk.

Bull case: 18% undervalued

"Ongoing operational initiatives such as automation, new manufacturing facility ramp, and salesforce expansion are increasing plant utilization and operational leverage, supporting steady gross margin expansion and bottom-line (EBITDA) growth as scale increases..."

Read the full Bull Case to see why Vericel could be undervalued

Bear case: 11% overvalued

"Operating multiple facilities at once and absorbing related costs could pressure gross margin and adjusted EBITDA margin before efficiency gains are fully realized..."

Read the full Bear Case to see why Vericel could be overvalued

Do you think there's more to the story for Vericel? Head over to our Community to see what others are saying!

The Bottom Line

Vericel screens as overvalued on market multiples, with a very wide gap between its current P/E and the sector benchmarks. That points to a stock where investors are already paying up for a specific outlook and leaving little room for disappointment. For you, the key question is whether Vericel can deliver the margin progress and execution needed to make that premium feel justified, or whether the current multiple proves too rich if those expectations slip.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com