Iridium (IRDM) Stock May Be 49% Undervalued Despite New PNT Chip Launch

Iridium Communications stock has surged 162.8% year to date, yet its valuation checks send mixed signals, with an intrinsic value estimate based on a Discounted Cash Flow (DCF) model suggesting the shares trade at a large discount while market multiples point to a richer pricing.

- Year to date, Iridium Communications is up 162.8%, which puts extra focus on whether the current price still leaves room against any estimate of intrinsic value.

- The launch of the Iridium PNT ASIC chip and the completed acquisition of Aireon may support expectations for future cash flows, but integration risks and execution around new positioning, navigation, and timing services can weigh on how much value investors are willing to assign today.

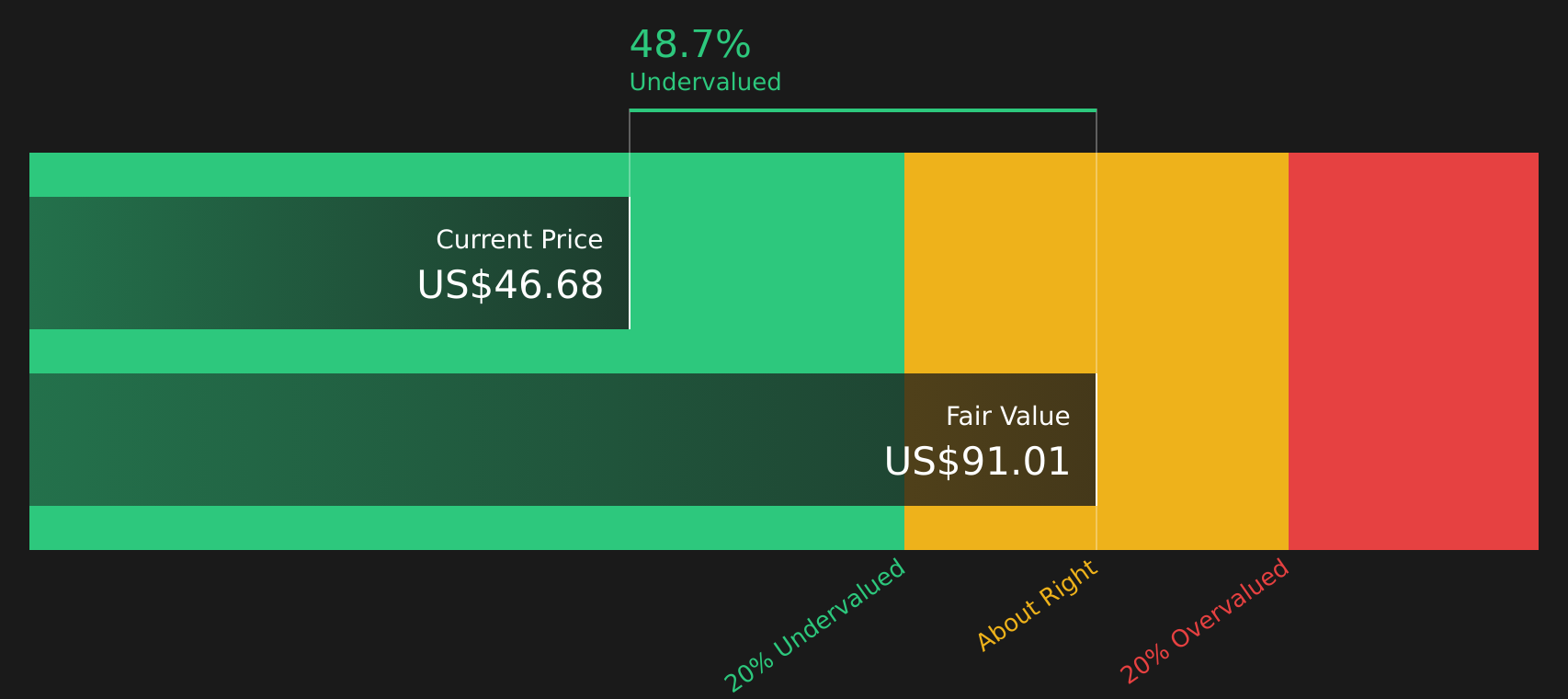

- The stock screens as undervalued on a Discounted Cash Flow (DCF) basis by about 48.7%. However, a low overall value score, with only 2 of 6 checks pointing to attractive pricing, suggests the broader set of valuation measures leans expensive rather than a clear bargain.

The issue now is whether Iridium Communications' strong year to date rally leaves enough upside relative to its intrinsic value estimate to justify the risks investors are taking on.

Is Iridium Communications a Bargain on Cash Flow?

The Discounted Cash Flow (DCF) method estimates what Iridium Communications could be worth based on the cash it is expected to generate for shareholders. On the latest twelve month figures, Iridium Communications produced around $323.0 million of free cash flow, and the model assumes these cash flows grow rather than contract over time, using a 2 Stage Free Cash Flow to Equity approach.

On these assumptions, the DCF points to an estimated intrinsic value of about $91 per share. Compared with the current share price, this implies the stock screens as 48.7% undervalued. Because the launch of the Iridium PNT ASIC and the Aireon acquisition give the market new information to digest, the discount suggests investors are applying caution to those cash flow projections even though the DCF indicates more value than the current price reflects.

Overall, Iridium Communications stock currently appears undervalued relative to what its discounted cash flows suggest it could be worth.

Our Discounted Cash Flow (DCF) analysis suggests Iridium Communications is undervalued by 48.7%. Track this in your watchlist or portfolio, or discover 47 more high quality undervalued stocks.

Does Iridium Communications Look Pricey on Earnings?

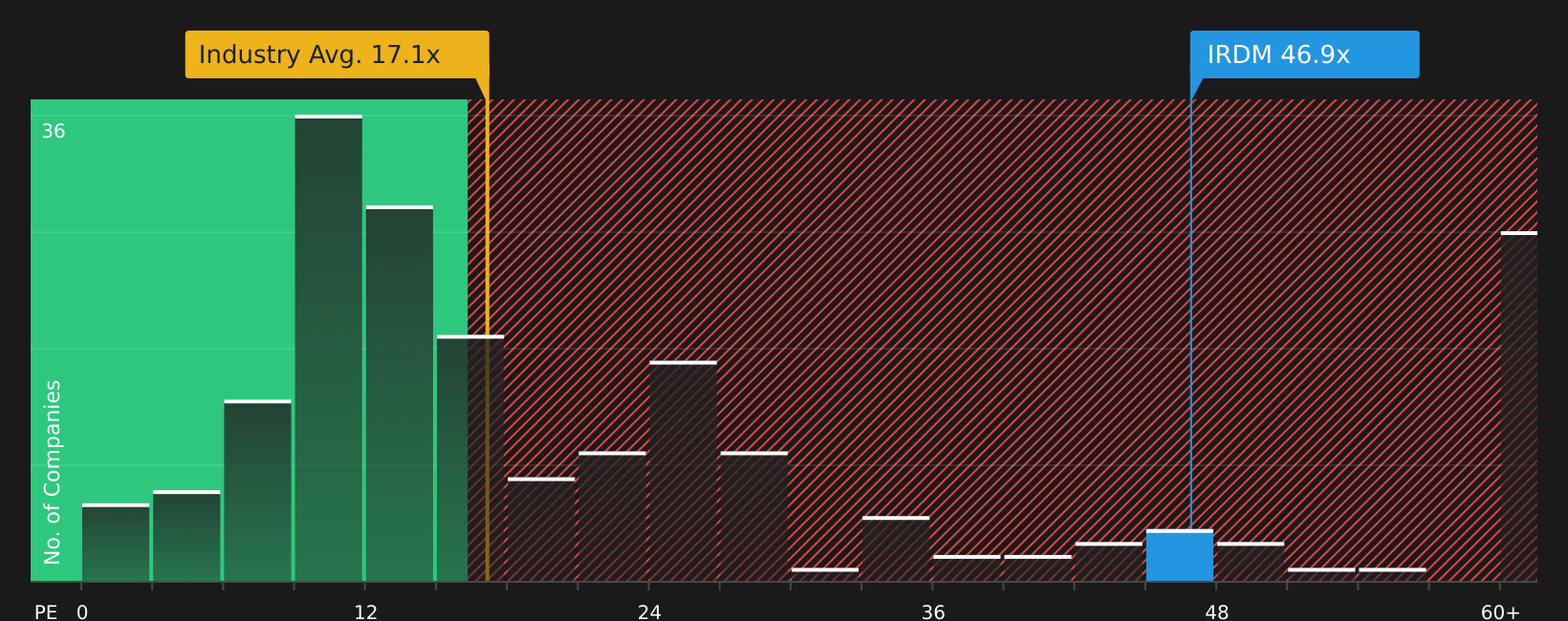

P/E is a useful lens for Iridium Communications because earnings remain a key anchor for how the market values established satellite and telecom operators. Iridium Communications currently trades on a P/E of about 46.9x, which is well above the broader telecom industry average of roughly 17.2x and also higher than the peer group average of around 8.7x.

The fair P/E ratio for Iridium Communications, based on its profile and risk factors, is estimated at about 18.8x. Compared with the current 46.9x multiple, the stock trades at a substantial premium to what this framework suggests would be a more typical level. Even with interest around the Iridium PNT ASIC chip and the Aireon acquisition, the current earnings multiple indicates that significant optimism is already reflected in the price.

On the P/E multiple, Iridium Communications stock appears expensive relative to both tailored and industry benchmarks.

See what the numbers say about this price — find out in our valuation breakdown.

The Iridium Communications Narrative: What Would Justify Today's Price?

Simply Wall St Narratives pick up where Iridium Communications' valuation puzzle leaves off by spelling out which assumptions about future growth, margins and earnings would need to hold for the stock to be worth materially more or less than today's price. Each one treats fair value as a thesis about how Iridium Communications' business might evolve over time, so you can watch how that view holds up, and they sit on the company's Community page.

Community views on Iridium Communications sit far apart, with one camp focused on spectrum and service upside and the other on execution and capital demands.

Bull case: 22% undervalued

"Bullish analysts who raised fair value estimates to the US$54 to US$60 range point to owned spectrum, Aireon exposure and service upgrades as key supports for higher long term earnings power and cash generation assumptions…"

Read the full Bull Case to see why Iridium Communications could be undervalued

Bear case: roughly fairly valued

"The deceleration in IoT (Internet of Things) service revenue growth now under double-digits in recent quarters despite ongoing partner and device expansion raises concerns about the sustainability of this core growth pillar…"

Read the full Bear Case to see why Iridium Communications could be overvalued

Do you think there's more to the story for Iridium Communications? Head over to our Community to see what others are saying!

The Bottom Line

For Iridium Communications, the Discounted Cash Flow (DCF) intrinsic value points to meaningful upside, but the market multiple view flags the stock as overvalued on earnings. That split largely comes down to how much weight you place on future cash flows in a capital intensive business versus today’s P/E and where peers trade. With a low overall value score, the broader set of checks is not as supportive as the DCF alone. The real swing factor from here is whether Iridium Communications can translate its positioning, navigation and timing ambitions into durable cash generation that justifies either the current multiple or a re rating over time.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com