Macy's Stock Leads This Value Screen After SpaceX Market Stress

With SpaceX stock under pressure, higher short interest and bond market stress are pushing some investors to reassess where they want to take risk in the space and aerospace theme. That is where a value-focused screener can help. By filtering for companies with market caps above $300 million, lower price multiples, moderate balance sheet risk and dividend potential, it aims to surface stocks that may be better aligned with a more cautious mood. This article walks through 3 stocks exposed to the latest SpaceX news and explains why some investors may see them as potential opportunities.

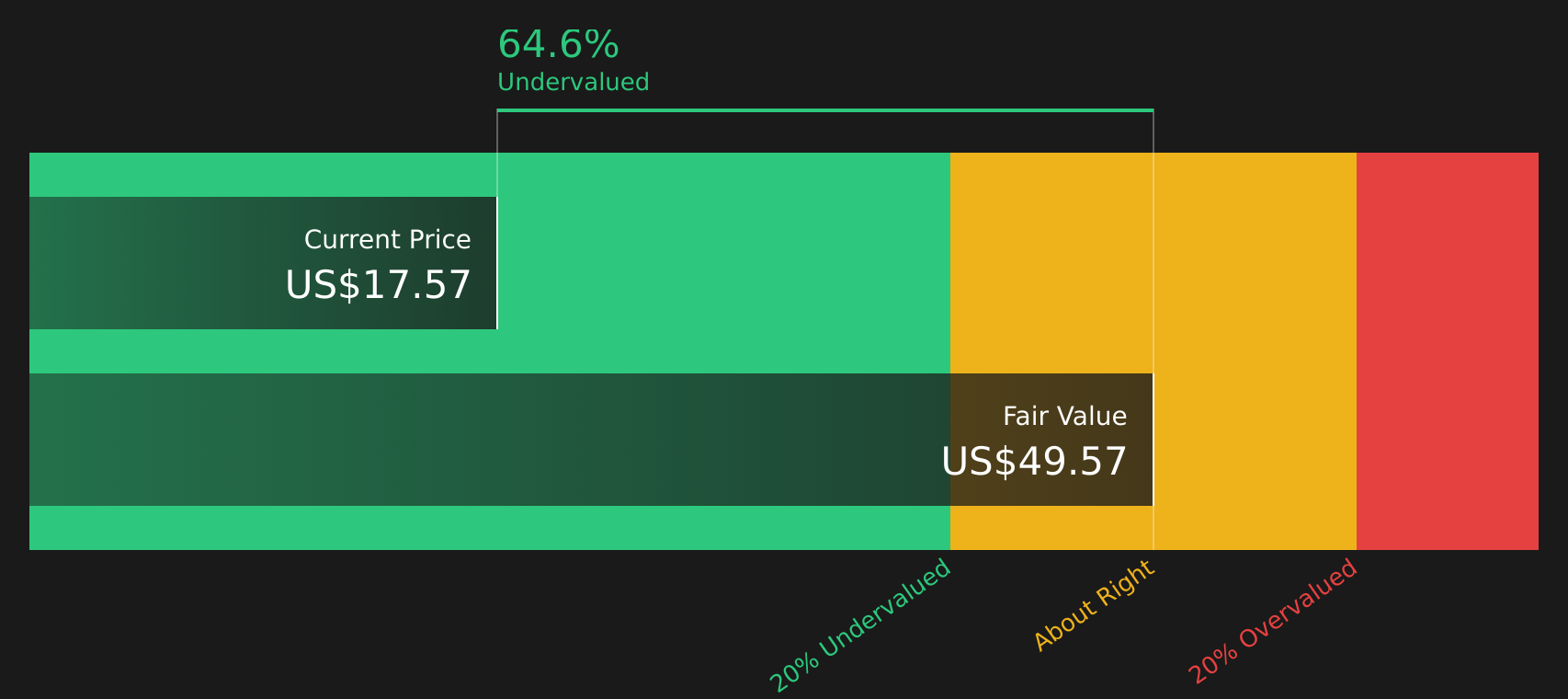

Macy's (M)

Overview: Macy's is a long-established US retailer that runs department stores, websites and apps under the Macy's, Bloomingdale's and Bluemercury brands, selling apparel, accessories, beauty products, home goods and other consumer items. It also licenses its brands for stores in Dubai and Kuwait, giving it an international presence alongside its core US footprint.

Operations: Macy's generates about US$22.7b in annual revenue almost entirely from its US department store operations.

Market Cap: US$6.3b

For investors watching the shift out of high growth stories like SpaceX into more grounded value ideas, Macy's is sometimes viewed as combining established fundamentals with ongoing business change. The stock trades on relatively low earnings multiples and Simply Wall St provides a cash flow estimate that is above the current price. Management is also reshaping the business through omni-channel upgrades, store optimization and a bigger push into higher margin luxury and beauty. At the same time, forecasts referenced in the article point to revenue pressure and modest returns on equity, and the company still relies on external borrowing and has an uneven dividend record. How those factors interact is where the potential opportunities and risks for Macy's investors may arise.

Macy's valuation story is getting interesting, with low earnings multiples and a Simply Wall St cash flow estimate above the current price hinting that the market may be missing a key angle. The DCF valuation analysis for Macy's could show whether that gap reflects hidden strength or something more uncomfortable beneath the surface.

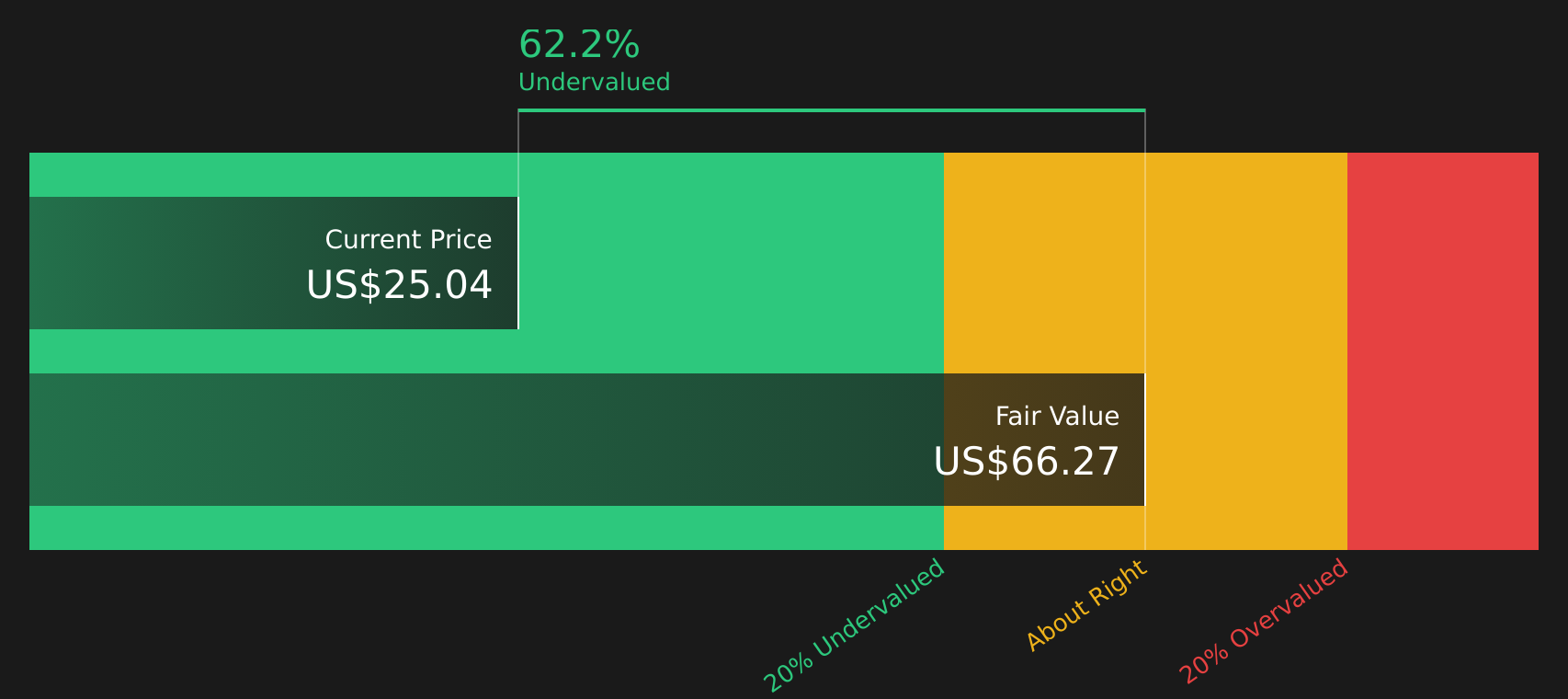

Kohl's (KSS)

Overview: Kohl's is a US omnichannel retailer selling apparel, footwear, accessories, beauty products and home goods through its nationwide department stores and website, anchored by private labels like Apt. 9, Sonoma Goods for Life and Jumping Beans alongside partnerships such as Simply Vera Vera Wang. Founded in 1988 and based in Menomonee Falls, Wisconsin, Kohl's targets value-focused households looking for branded products at accessible prices.

Operations: Kohl's generates about US$15.5b in revenue from its US department store operations.

Market Cap: US$2.0b

For investors looking at the SpaceX reset and rethinking how much risk to take, Kohl's stands out as a lower multiple, cash-generative retailer where expectations are already subdued. The stock screens as deeply discounted relative to some fair value estimates. The business is still producing profits, has recently improved margins to 1.8% and is working on cost discipline, private label growth and its Sephora rollout to support earnings. At the same time, weak traffic from core middle income shoppers, an unstable dividend, heavy reliance on external borrowing and a long history of pressured earnings mean this is not a straightforward value story. How those conflicting signals add up is what makes Kohl's a potential candidate for a cautious value watchlist.

Kohl's valuation story looks heavily discounted, yet the business is still producing profits and reshaping its model, so the real question is what the analysis report for Kohl's reveals about the next twist in this reset.

LKQ (LKQ)

Overview: LKQ is a global distributor of vehicle parts and accessories, supplying collision and mechanical repair shops, car dealerships and retail customers with everything from body panels and engines to aftermarket upgrades and recycled components.

Operations: LKQ generates most of its revenue from Europe at about US$6.4b and North America at about US$5.7b, with smaller contributions from its Specialty segment and internal eliminations.

Market Cap: US$6.6b

LKQ may attract investors rotating out of high growth stories such as SpaceX and into steadier, underappreciated stocks, because it combines comparatively low P/E multiples with a global parts business tied to everyday vehicle repairs. The company has reported recent guidance cuts, weaker margins and a legal overhang from the Uni Select acquisition, which have kept sentiment more muted. Management has been pursuing cost reductions, a review of the Specialty division and ongoing share repurchases, while also paying a regular dividend. That combination of operational changes, legal considerations and capital returns is one reason some investors are taking a closer look at LKQ.

LKQ looks like a classic valuation story in motion, with a low P/E, cost cuts and capital returns that may be masking a bigger question: the DCF valuation analysis for LKQ could reshape how you view the risk-reward trade-off.

The three stocks covered here are only the starting point, as the full Value Stocks screener surfaces 30 more companies that fit this value theme and come with equally compelling narratives waiting to be analyzed. Use Simply Wall St to identify and analyze the specific catalysts, balance sheet traits and dividend profiles that matter to you, so you can focus on the value stocks that best match your highest conviction ideas.

Take Control of Your Investment Journey

If Macy's or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Alternatives Before Everyone Else?

Fresh ideas can move quickly, and the stocks that look quiet today can be the ones breaking out tomorrow. Instead of waiting until momentum is already strong, consider researching opportunities earlier.

- Identify resilient payers before yields change by scanning 8 dividend fortresses, which is built around income opportunities that still look under the radar for now.

- Research the buildout of AI-related infrastructure while prices still appear reasonable by checking 53 AI infrastructure stocks, which focuses on companies involved in data centers and related infrastructure.

- Explore infrastructure spending themes by using 33 power grid technology and infrastructure stocks, which highlights businesses supporting grid upgrades, storage and transmission while broader attention may be focused elsewhere.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com