Packaging Corp (PKG) Stock Could Be Below Fair Value As Cash Flow Holds

Packaging Corporation of America stock has more than doubled over the past five years, yet the valuation signals are split, with the Discounted Cash Flow (DCF) intrinsic value estimate pointing to a large discount while market multiples paint a richer picture.

- Shareholders have seen a 102.1% return over 5 years, which puts the recent share price in focus for anyone thinking about what is already priced in.

- On the positive side, steady cash generation from packaging demand can support the DCF view of attractive intrinsic value. However, any pressure on margins or a sustained downturn in volumes may limit how much of that estimated upside the market is willing to recognize.

- The stock screens as undervalued on some checks but expensive on others, and with 3 of 6 valuation tests pointing to value, the overall picture is a mixed one rather than a clear bargain or a clear sell signal.

The issue now is whether Packaging Corporation of America's current price already reflects its long term cash flow potential or if the DCF based intrinsic value gap still offers meaningful upside.

Is Packaging Corporation of America Still Cheap on Cash Flow?

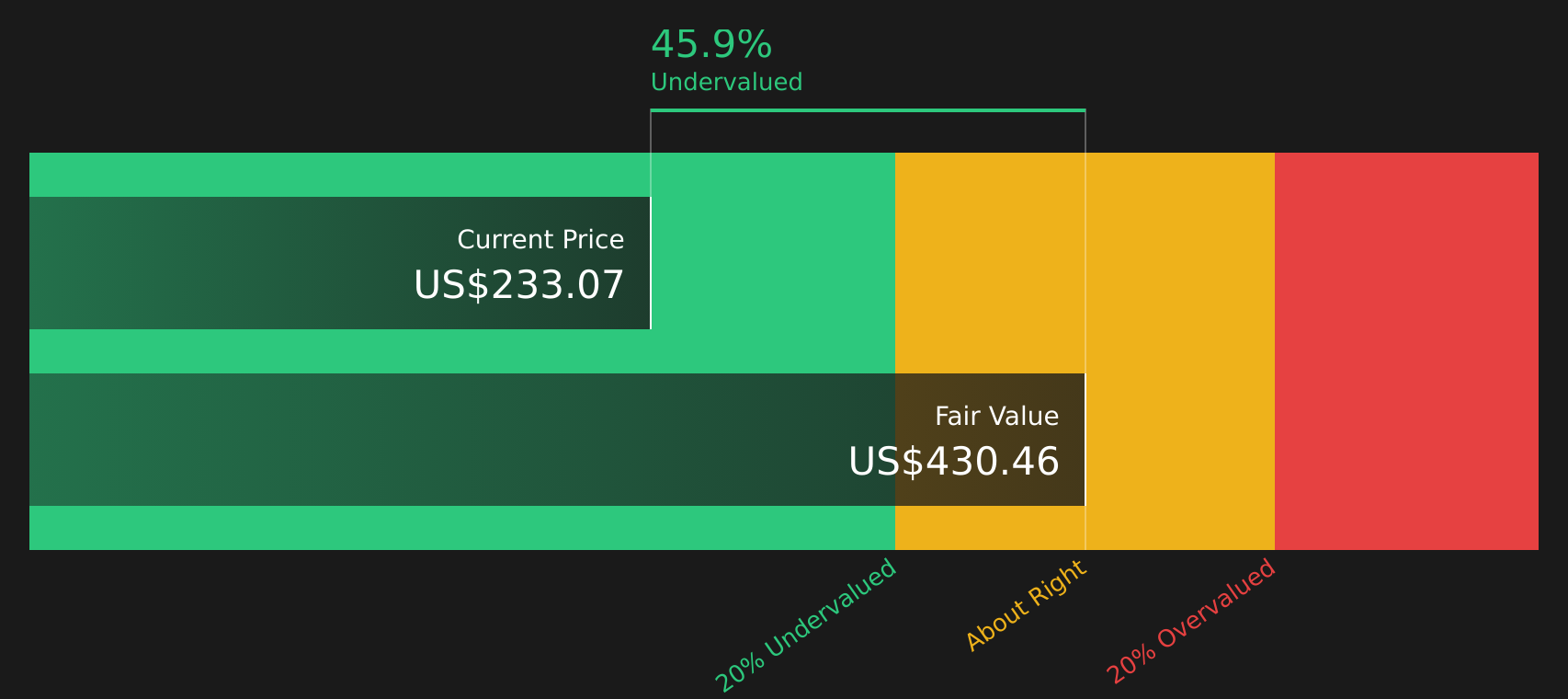

The Discounted Cash Flow (DCF) model estimates what Packaging Corporation of America is worth based on the cash it can generate for shareholders over time. The model starts from latest twelve month free cash flow of about $819.3 million and assumes that free cash flow continues growing from this base rather than shrinking. On that set of projections, the 2 Stage Free Cash Flow to Equity approach points to an intrinsic value of about $430 per share.

Compared with the current market price, that DCF estimate implies Packaging Corporation of America trades at roughly a 45.9% discount to intrinsic value. On this cash flow view, the stock appears undervalued. The key message for readers is that the company’s recent free cash flow level, combined with moderate growth assumptions, supports a valuation that is materially higher than where the shares currently change hands.

On the DCF numbers alone, Packaging Corporation of America stock appears undervalued relative to the cash it is projected to generate.

Our Discounted Cash Flow (DCF) analysis suggests Packaging Corporation of America is undervalued by 45.9%. Track this in your watchlist or portfolio, or discover 47 more high quality undervalued stocks.

Does Packaging Corporation of America Look Pricey on Earnings?

The P/E ratio is a useful cross check for Packaging Corporation of America because earnings quality and consistency matter for an established packaging business. Packaging Corporation of America currently trades on a P/E of about 28.0x, compared with a packaging industry average of roughly 16.1x and a peer group average of around 29.5x.

The fair P/E ratio suggested by the model is about 23.9x, which is lower than where the stock trades today. That gap indicates investors are paying a higher price for each dollar of Packaging Corporation of America earnings than the model implies, even after accounting for its size, margins and risk profile. Placed alongside the DCF results, this suggests that while cash flow signals one thing, the earnings multiple points to a richer price tag.

On the P/E yardstick, Packaging Corporation of America stock appears overvalued relative to what the model and industry benchmarks indicate.

See what the numbers say about this price — find out in our valuation breakdown.

The Packaging Corporation of America Narrative: What Would Justify Today's Price?

Simply Wall St Narratives pick up where this valuation split for Packaging Corporation of America leaves off, by spelling out which paths for revenue, margins and earnings would need to play out for the stock to be worth materially more or less than today’s price, and they sit on the company’s Community page. Rather than focusing on a single model output, each one lays out its own fair value assumptions so you can compare those inputs with actual results over time.

The community is split on Packaging Corporation of America, with one camp seeing solid pricing power and efficiency gains and the other focused on structural demand and cost risks.

Bull case: roughly fairly valued

"Strong execution on price increases and new box plant efficiency suggest potential for improved net margins and earnings growth…"

Read the full Bull Case to see why Packaging Corporation of America could be undervalued

Bear case: 26% overvalued

"Advancing digitalization, automation, and evolving environmental regulations are slowly undermining demand, squeezing margins, and raising compliance costs for traditional paper-based packaging…"

Read the full Bear Case to see why Packaging Corporation of America could be overvalued

Do you think there's more to the story for Packaging Corporation of America? Head over to our Community to see what others are saying!

The Bottom Line

The Discounted Cash Flow (DCF) intrinsic value estimate suggests Packaging Corporation of America could be worth materially more than the current share price, while the market multiple view flags the stock as overvalued on earnings. That gap comes down to what investors trust more: the durability and timing of future cash flows, or the growth expectations and sentiment embedded in current P/E levels. With broader valuation checks landing in mixed territory, the key question is whether Packaging Corporation of America can sustain cash generation and margins strongly enough for the market to keep backing the richer earnings multiple rather than treating the DCF gap as a value trap.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com