STAAR Surgical (STAA) Stock Could Be 12% Undervalued On Q2 Sales Recovery

STAAR Surgical stock has staged a strong rebound over the past year, yet its valuation signals are split, with the Discounted Cash Flow (DCF) intrinsic value estimate pointing to some upside while traditional market multiples suggest the shares are not cheap.

- Over the past 5 years, STAAR Surgical has delivered a return of about 80% in decline, which puts the recent share price recovery in a very different light for long term holders.

- Recent sales momentum in Asia Pacific and recovering demand in China can support cash flow expectations, while geopolitical and macroeconomic uncertainties may limit how much investors are willing to pay for that growth.

- STAAR Surgical only passes 1 of 6 valuation checks, which leans more toward an expensive stock on the broader measures even though the intrinsic value estimate suggests it may be undervalued.

The issue now is whether the recent recovery in STAAR Surgical's share price already reflects the intrinsic value implied by cash flow estimates or still leaves a margin of safety for new money coming in.

Is STAAR Surgical a Bargain on Cash Flow?

The Discounted Cash Flow (DCF) method estimates what STAAR Surgical could be worth based on its expected future cash generation. For STAAR Surgical, the model starts from latest twelve month free cash flow of about $64.8 million in outflows, then assumes recovering cash flows that move into positive territory over time, using a 2 Stage Free Cash Flow to Equity approach.

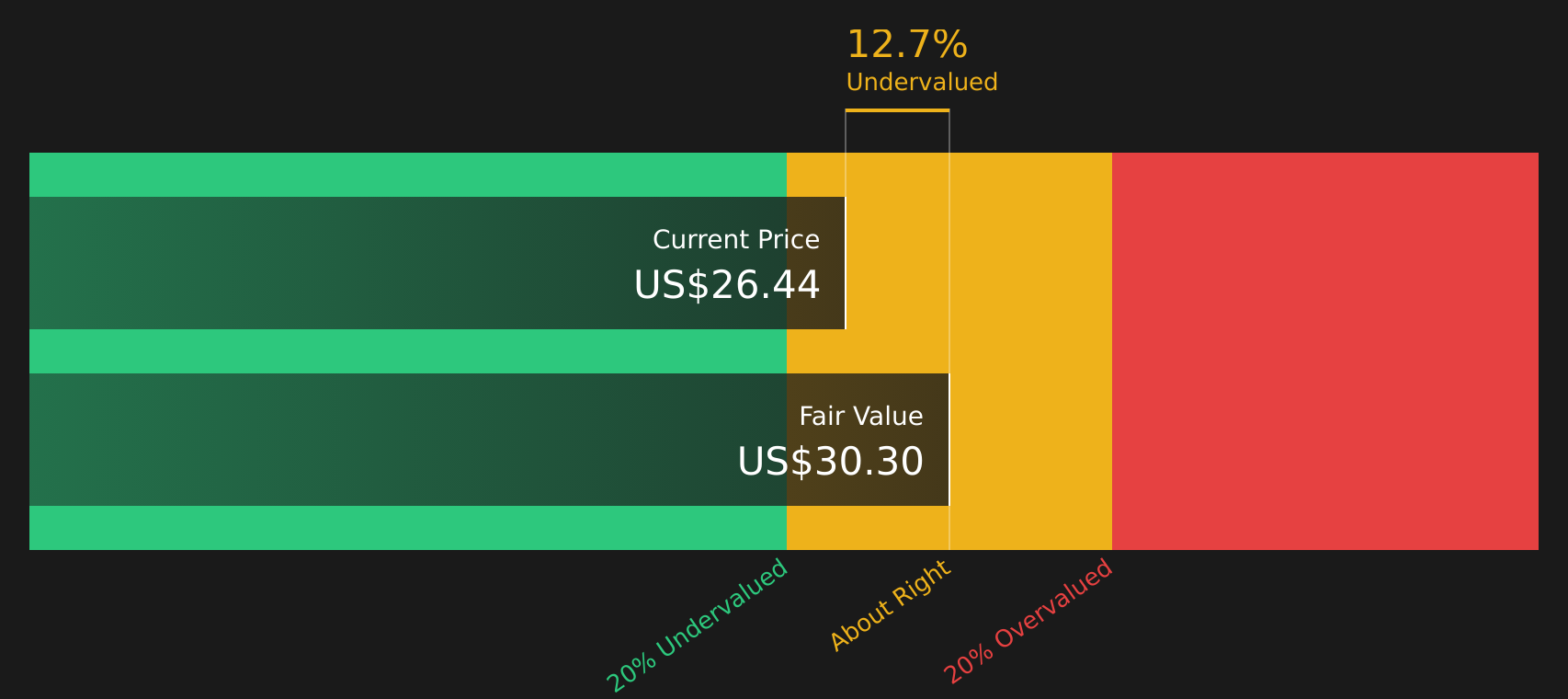

On these inputs, the DCF model points to an intrinsic value of about $30 per share, which implies the stock trades at roughly an 11.9% discount and screens as undervalued on this measure. Because preliminary Q2 2026 sales exceeded $90 million across regions, the recent trading price appears to reflect some of that momentum, yet the DCF output still suggests the market is not fully pricing in the projected cash flows.

Overall, the Discounted Cash Flow model indicates STAAR Surgical stock currently looks undervalued versus its estimated intrinsic value.

Our Discounted Cash Flow (DCF) analysis suggests STAAR Surgical is undervalued by 11.9%. Track this in your watchlist or portfolio, or discover 47 more high quality undervalued stocks.

Has STAAR Surgical Run Too Far on Sales?

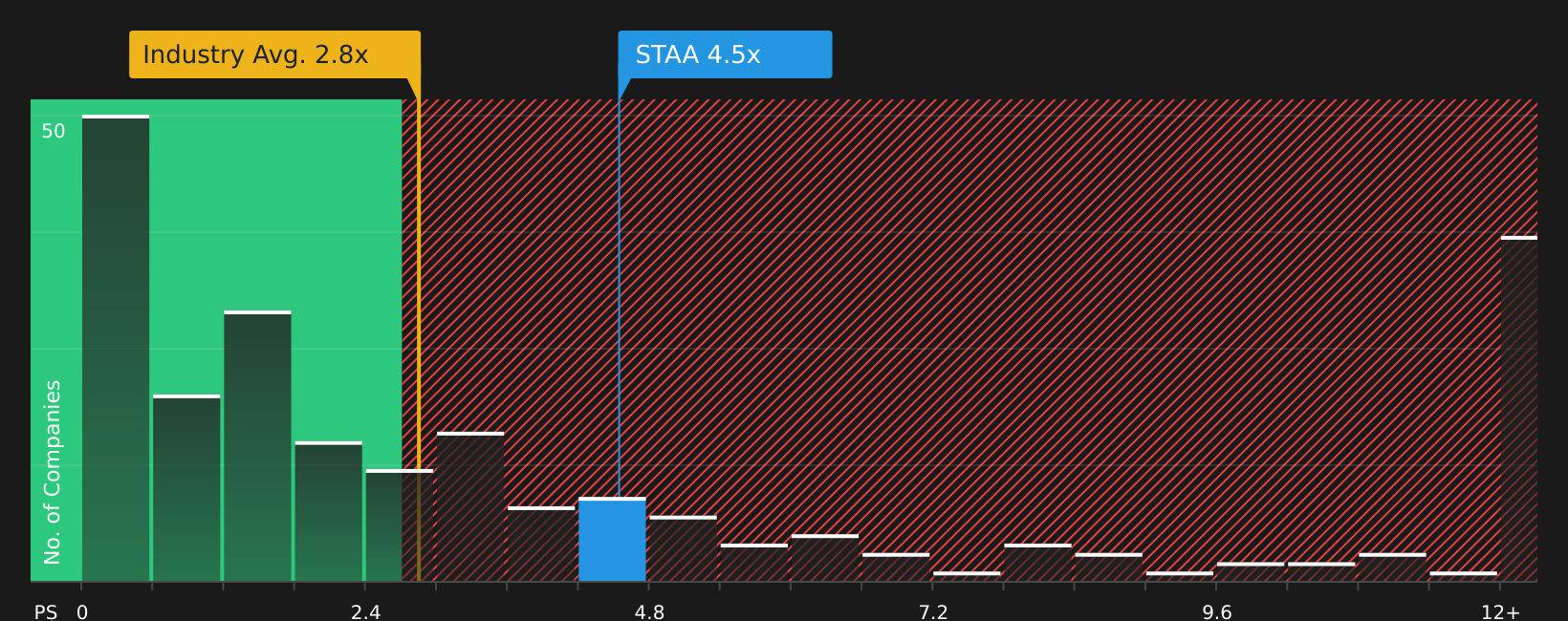

The P/S multiple suits STAAR Surgical because revenue is a cleaner yardstick when free cash flow and earnings are not yet a steady guide. Right now, STAAR Surgical trades at about 4.5x P/S, compared with an industry average of roughly 2.8x and a peer group average near 1.6x.

The tailored fair P/S ratio for STAAR Surgical is estimated at about 3.5x, which already factors in its growth profile, margins, size and risk. That puts the current 4.5x multiple meaningfully above this fair level. This suggests investors are paying a premium for the stock’s revenue base relative to what the model would expect.

On this P/S framework, STAAR Surgical stock screens as overvalued compared with both its fair ratio and sector benchmarks.

See what the numbers say about this price — find out in our valuation breakdown.

The STAAR Surgical Narrative: What Would Justify Today's Price?

Simply Wall St Narratives pick up where this valuation split for STAAR Surgical leaves off, making clear which combinations of future growth, margins and earnings would need to occur for the stock to be worth meaningfully more or less than the current price on the market. Each one sets out STAAR Surgical's fair value as a specific thesis about the business that can be tracked over time, and they are available on Simply Wall St's Community page.

Community views on STAAR Surgical sit far apart, with one camp focusing on a China and margin recovery, and the other on concentration and geopolitical risk.

Bull case: 11% undervalued

"STAAR Surgical has significant cash reserves and no debt, providing a strong financial base to navigate the current challenges, reduce production outputs temporarily, and invest selectively in growth initiatives, potentially stabilizing earnings and providing upside if conditions improve…"

Read the full Bull Case to see why STAAR Surgical could be undervalued

Bear case: 15% overvalued

"STAAR’s heavy reliance on intraocular collamer lens (ICL) products, without significant portfolio diversification, exposes the company to concentrated product risk, leaving future revenues and earnings highly vulnerable to rapid changes in surgical preferences and potential technological disruption from alternative, less-invasive vision correction therapies…"

Read the full Bear Case to see why STAAR Surgical could be overvalued

Do you think there's more to the story for STAAR Surgical? Head over to our Community to see what others are saying!

The Bottom Line

For STAAR Surgical, the Discounted Cash Flow (DCF) intrinsic value estimate points to some undervaluation, while the richer revenue multiple argues the stock is already priced at a premium to peers. That gap comes down to what you trust more: the long term cash flow profile or the market’s current growth and sentiment assumptions embedded in the P/S ratio. With broader valuation checks looking weak despite the DCF signal, the key question is whether revenue growth and margins can progress enough to justify staying on a premium multiple rather than the stock settling closer to its fair ratio.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com