How Investors May Respond To Deere (DE) Granting Broader Right-to-Repair Access After FTC Settlement

- In early July 2026, Deere & Company reached an agreement with the Federal Trade Commission and five states to give farmers and independent technicians broader access to diagnostic and repair tools for both current and future equipment, formally ending a matter filed in early 2025.

- This settlement locks in ongoing regulatory oversight of Deere’s repair practices, potentially reshaping the balance between equipment sales, high-margin service revenue, and customer control over maintenance.

- Next, we’ll examine how this right-to-repair agreement, and its impact on Deere’s service business model, affects the company’s investment narrative.

We've uncovered the 8 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

Deere Investment Narrative Recap

To own Deere, you need to believe its mix of iron, software, and services can remain attractive even as farm and construction cycles move around. The new right to repair settlement adds some uncertainty around high margin service revenue, but it does not change the near term focus on stabilizing large ag demand and managing tariff and cost pressures, which remain the key catalyst and the biggest risk.

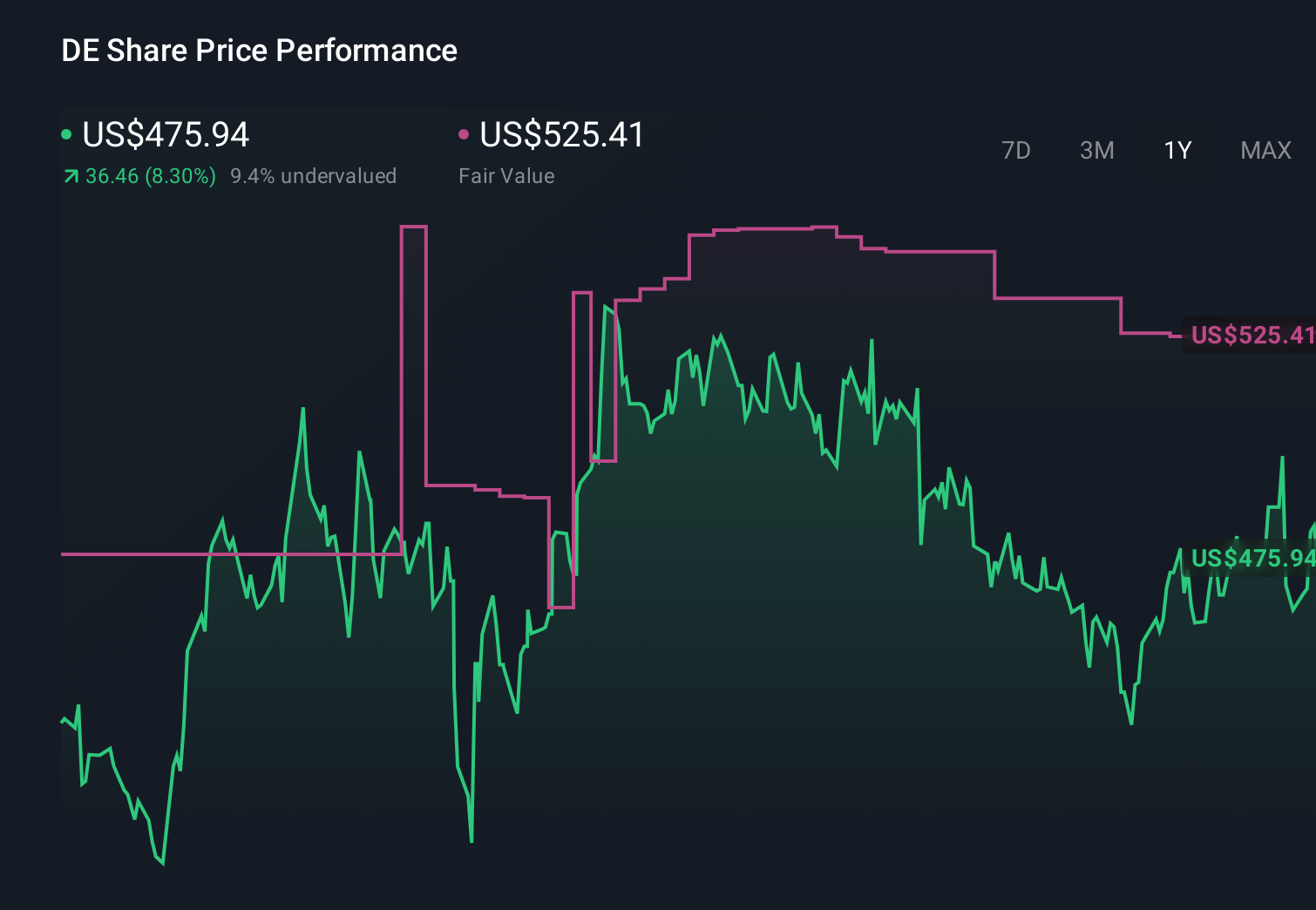

Recent commentary that Deere stock screens as undervalued on discounted cash flow and earnings multiples is especially relevant here, because those models hinge on future margin and cash flow assumptions. The right to repair agreement could influence how much value Deere can sustain from its aftermarket service model, which is central to many of those intrinsic value estimates.

Yet behind the appeal of more flexible repair options, there is a material risk investors should be aware of around Deere’s reliance on high margin service income...

Read the full narrative on Deere (it's free!)

Deere's narrative projects $48.4 billion revenue and $9.3 billion earnings by 2029. This assumes fairly flat yearly revenue growth and an earnings increase of about $4.5 billion from $4.8 billion today.

Uncover how Deere's forecasts yield a $644.21 fair value, a 8% upside to its current price.

Exploring Other Perspectives

Some of the lowest analysts were already cautious, assuming earnings of about US$6.1 billion by 2029 and a lower PE, so you should expect views on margin risk from right to repair to diverge even more from here.

Explore 3 other fair value estimates on Deere - why the stock might be worth just $644.21!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Deere research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Deere research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Deere's overall financial health at a glance.

Seeking Other Investments?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- Invest in the nuclear renaissance through our list of 90 elite nuclear energy infrastructure plays powering the global AI revolution.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 29 best rare earth metal stocks of the very few that mine this essential strategic resource.

- The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com