Acadia Healthcare (ACHC) Stock May Stay Cheap As Options Signal A Big Move

Acadia Healthcare Company stock has surged 141.4% year to date, and the valuation checks now suggest the shares lean cheap rather than stretched despite that strong run.

- Year to date, Acadia Healthcare Company has returned 141.4%, which puts recent price action firmly in focus for anyone assessing what is already priced in.

- Options market activity pointing to elevated implied volatility can support a case that investors expect a meaningful shift in the earnings outlook, but cuts to earnings estimates introduce the risk that expectations for the business may have run ahead of updated forecasts.

- On Simply Wall St's broader checklist, Acadia Healthcare Company screens as undervalued in 5 of 6 valuation tests, which tilts the overall picture toward the stock looking inexpensive on the numbers.

The issue now is whether Acadia Healthcare Company's current share price still offers enough valuation cushion after such a strong year to date move.

Is Acadia Healthcare Company Still Cheap on Sales?

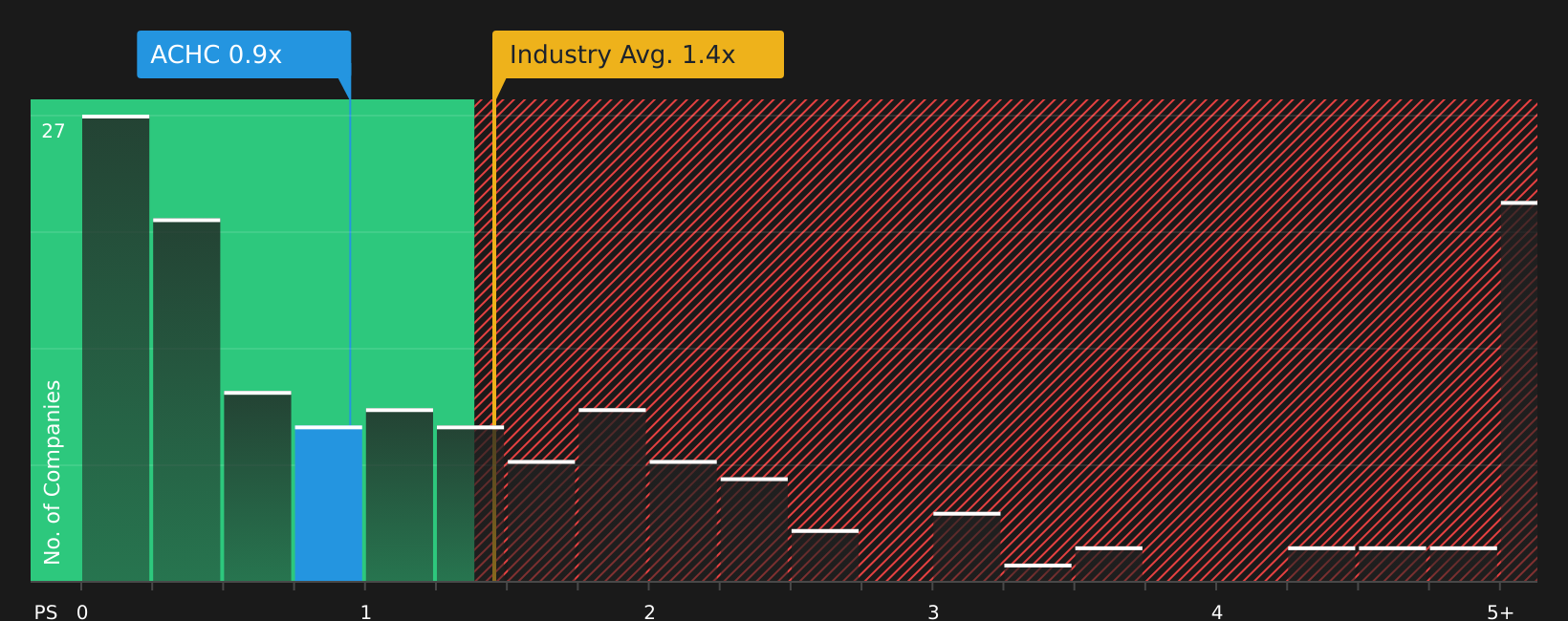

The P/S multiple fits Acadia Healthcare Company reasonably well because revenue is a cleaner yardstick when free cash flow and earnings are currently messy. Right now the stock trades on a P/S of 0.9x, which sits below both the healthcare industry average of around 1.4x and the peer group average of about 1.5x.

The tailored fair P/S ratio for Acadia Healthcare Company is estimated at 1.3x, which is higher than where the shares currently change hands. That gap indicates the market is pricing the company at a discount to what might be expected given its size, risk profile and sector, even as options activity points to expectations of bigger swings ahead. Taken together, the sales-based checks suggest the market is not paying a premium for the revenue Acadia Healthcare Company already generates.

On the P/S multiple, Acadia Healthcare Company stock currently screens as undervalued based on this metric.

See what the numbers say about this price — find out in our valuation breakdown.

The Acadia Healthcare Company Narrative: What Would Justify Today's Price?

Simply Wall St Narratives for Acadia Healthcare Company sit alongside the valuation checks you have just seen, explaining which combinations of future growth, margins and earnings would need to occur for the stock to be worth meaningfully more or less than its current price. Each Narrative links a fair value estimate to a particular story about Acadia Healthcare Company's potential catalysts and risks, so you can track over time which version appears to be unfolding on the Community page.

Community views on Acadia Healthcare Company sit at opposite ends of the spectrum, with one camp seeing meaningful upside and the other flagging material downside risk.

Bull case: 12% undervalued

"Analyst consensus anticipates additional beds transitioning from losses to profitability and supporting EBITDA from 2026, but management commentary and faster-than-expected facility openings suggest the ramp may occur much sooner, potentially leading to an outsized acceleration in both revenue and EBITDA as early as the latter part of 2025..."

Read the full Bull Case to see why Acadia Healthcare Company could be undervalued

Bear case: 189% overvalued

"The biggest risk for Acadia is not demand, it’s execution..."

Read the full Bear Case to see why Acadia Healthcare Company could be overvalued

Do you think there's more to the story for Acadia Healthcare Company? Head over to our Community to see what others are saying!

The Bottom Line

Acadia Healthcare Company screens as undervalued on its sales-based multiples, which suggests the current price is not assigning a premium to the revenue already in place. The key question for you is whether that discount reflects genuine mispricing or fairly captures the execution risks highlighted by the bear case. From here, the crux is whether management can convert capacity and facility expansion into reliable, profitable growth without major setbacks. If that execution holds, the current valuation could look conservative. However, if operational missteps persist, the apparent discount may prove to be a value trap.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com