Booz Allen (BAH) Stock Looks Discounted On Earnings Yet Weak On Price Trend

Booz Allen Hamilton Holding stock has had a tough run over the last few years, yet the valuation checks currently lean in the other direction and suggest the shares may be pricing in a lot of bad news already. With the price at US$65.21 and the broader metrics screening the company as relatively cheap, investors are weighing whether the recent share price weakness has gone too far.

- The stock is down about 40.3% over the past 3 years, which points to a period where sentiment has been weak even as the business continues to be assessed as relatively inexpensive on several metrics.

- Future project wins and the ability to convert contracted work into steady cash flow can support the case for a higher valuation, while any pressure on margins or delays in converting backlog into revenue remain key risks to that outlook.

- Booz Allen Hamilton Holding scores 5 out of 6 on the valuation checks, which means the broader set of metrics leans toward the stock being undervalued.

The issue now is whether Booz Allen Hamilton Holding's weak share price performance has created a genuine valuation opportunity or simply reflects ongoing business risks that the current multiples are correctly capturing.

Is Booz Allen Hamilton Holding a Bargain on Earnings?

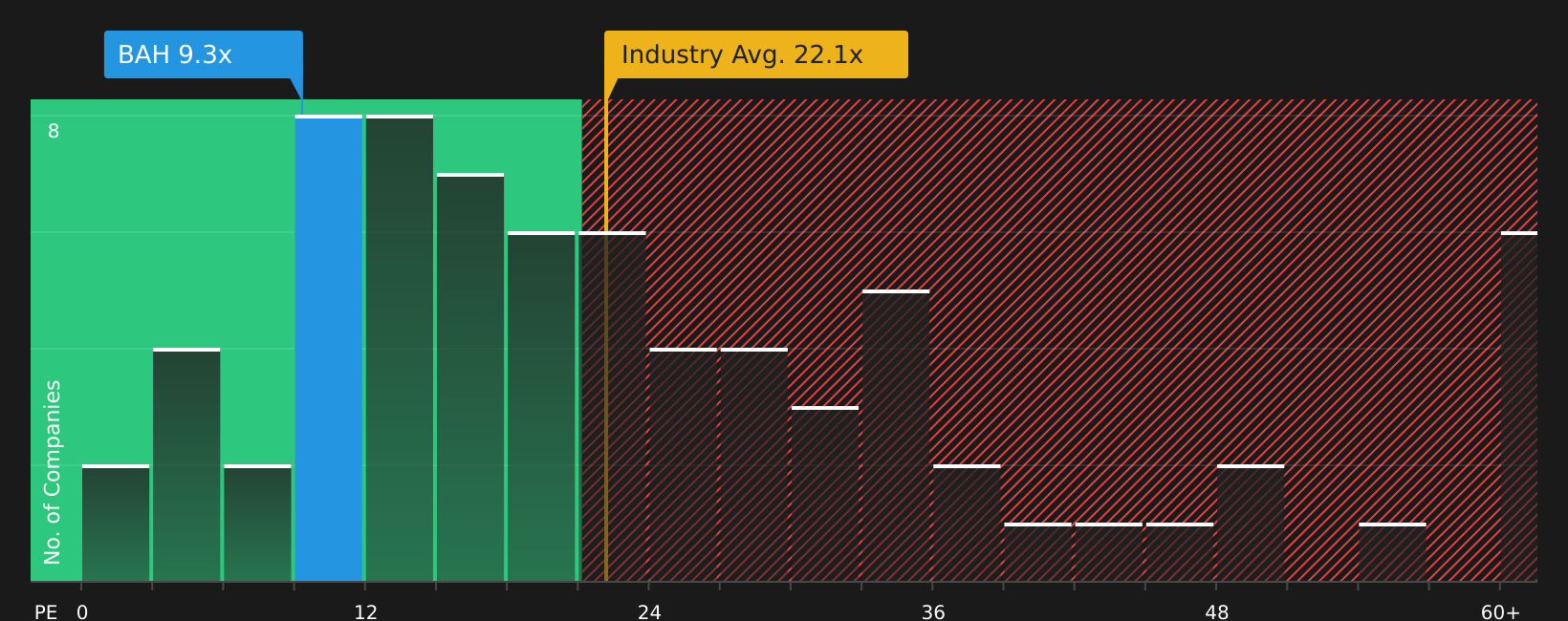

The P/E ratio is a useful way to think about Booz Allen Hamilton Holding because earnings are a key anchor for how the market is valuing the stock today. Booz Allen Hamilton Holding currently trades on a P/E of about 9.3x, which is well below the Professional Services industry average of around 21.3x and the broader peer group average of roughly 23.2x.

The model suggests a fair P/E ratio of about 15.2x for Booz Allen Hamilton Holding, based on its sector, size and risk profile. The current multiple therefore sits noticeably under that level. That gap indicates the market is pricing the stock at a discount to what these inputs imply, even after accounting for industry context.

On the P/E multiple alone, Booz Allen Hamilton Holding stock appears undervalued relative to both its tailored fair ratio and sector benchmarks.

See what the numbers say about this price — find out in our valuation breakdown.

The Booz Allen Hamilton Holding Narrative: What Would Justify Today's Price?

Simply Wall St Narratives for Booz Allen Hamilton Holding pick up where the valuation puzzle leaves off by explaining which paths for Booz Allen Hamilton Holding's growth, margins and earnings would need to occur for the stock to be worth materially more or less than it is today. Rather than relying on a single multiple or model point estimate, each narrative lays out its underlying assumptions so you can compare them with the company’s actual results over time on the Community page.

One of the top community narratives on Booz Allen Hamilton Holding: 5% undervalued

"Client preference is rapidly moving toward outcome-based, fixed-price contracts rather than traditional time-and-materials billing, which will intensify price competition and compress industry-wide margins..."

Read one of the top narratives on Booz Allen Hamilton Holding

Do you think there's more to the story for Booz Allen Hamilton Holding? Head over to our Community to see what others are saying!

The Bottom Line

For Booz Allen Hamilton Holding, the key takeaway is that the current market-multiple view points to the stock screening as undervalued relative to peers and its tailored P/E benchmark. That discount only becomes compelling if the company can sustain earnings power and convert its contracted work into dependable cash flow without a meaningful hit to margins.

The debate from here centers on whether the current valuation gap reflects an overly cautious mood or a fair cushion for contract risk and execution pressure. Your view on how Booz Allen Hamilton Holding manages margins and backlog conversion is likely to determine which side of that argument you support.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com