Clover Health’s Member Data Breach Might Change The Case For Investing In Clover Health Investments (CLOV)

- Earlier this month, Clover Health Investments reported that a hacker used social engineering to access three non-managerial employee accounts on July 4, exposing some personal and protected health information but not its core financial or claims systems.

- The incident highlights how frontline operational roles, such as visit schedulers and broker-facing staff, can become critical entry points for attackers seeking sensitive member data.

- We’ll now examine how this cybersecurity breach, particularly the exposure of member health information via compromised employee accounts, may influence Clover’s investment narrative.

Uncover the next big thing with 20 elite penny stocks that balance risk and reward.

Clover Health Investments Investment Narrative Recap

To own Clover Health, you need to believe its technology-focused Medicare Advantage model can translate member growth into sustainable profitability, while keeping medical costs and regulatory exposure in check. The recent cybersecurity incident appears operational rather than financially material in the near term, but it reinforces data privacy as a real risk that could affect trust and, indirectly, membership and margins if such events recur.

In this context, Clover’s recent interoperability announcements, including going live on the CMS Aligned Network and TEFCA with real-time patient-directed data sharing, feel particularly relevant. These initiatives deepen Clover’s dependence on secure, connected data flows, which may enhance the value of its Clover Assistant platform but also raise the stakes around information security, a key consideration alongside upcoming earnings and the path toward GAAP profitability.

Yet even if near term financial catalysts play out as hoped, the cybersecurity and compliance risks around member data remain something investors should be aware of...

Read the full narrative on Clover Health Investments (it's free!)

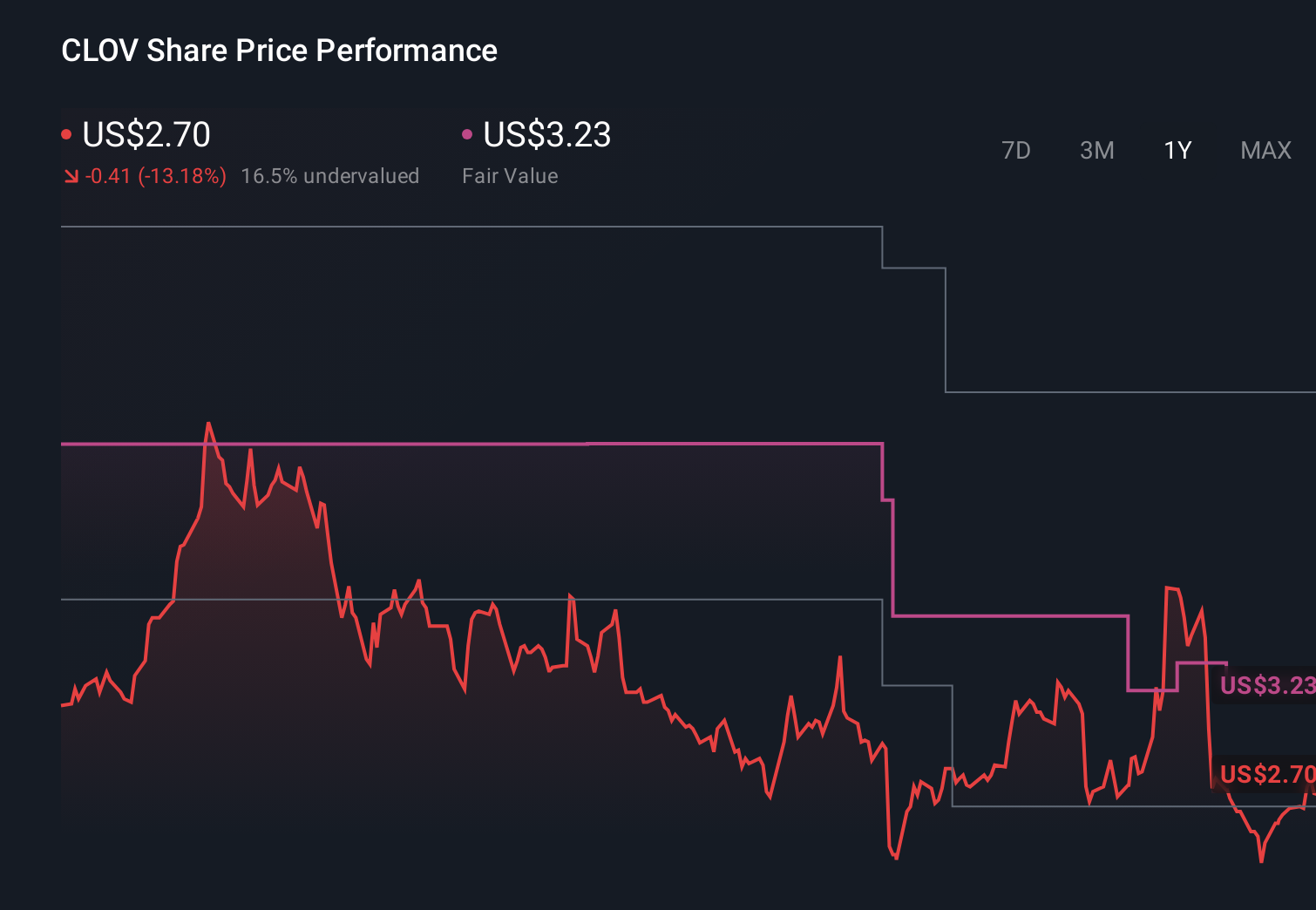

Clover Health Investments’ narrative projects $4.0 billion revenue and $30.9 million earnings by 2029.

Uncover how Clover Health Investments' forecasts yield a $4.15 fair value, a 10% downside to its current price.

Exploring Other Perspectives

While the baseline view leans on tech-driven efficiency, the most pessimistic analysts were already cautious, assuming about US$3.8 billion in 2029 revenue and only US$26.3 million in earnings, and this kind of cybersecurity event could prompt you to reconsider how much weight you give to those more conservative scenarios.

Explore 4 other fair value estimates on Clover Health Investments - why the stock might be worth over 7x more than the current price!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Clover Health Investments research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Clover Health Investments research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Clover Health Investments' overall financial health at a glance.

Seeking Other Investments?

Our top stock finds are flying under the radar-for now. Get in early:

- Invest in the nuclear renaissance through our list of 90 elite nuclear energy infrastructure plays powering the global AI revolution.

- The latest GPUs need a type of rare earth metal called Neodymium and there are only 29 companies in the world exploring or producing it. Find the list for free.

- Capitalize on the AI infrastructure supercycle with our selection of the 53 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com