Low Risk UK Stocks With Strong Balance Sheets and Staying Power

With inflation trends diverging across regions, central banks weighing their next moves, and energy prices swinging on geopolitics, many investors are looking for a way to stay invested while keeping portfolio risk in check. That is where the Low-Risk Leaders screener comes in. It focuses on what the model identifies as resilient companies with strong balance sheets and lower risk scores. Instead of chasing the hottest story, you can focus on stability and quality. In this article, you will see three stocks from the Low-Risk Leaders screener that fit this foundation-building approach.

Griffin Mining (AIM:GFM)

Overview: Griffin Mining is a London headquartered mining and investment company that focuses on extracting zinc, gold, silver, lead and other precious metals, primarily through its Caijiaying mine in Hebei Province, China.

Operations: Griffin Mining generates all of its US$137.5 million in revenue from the Caijiaying Zinc Gold Mine in China.

Market Cap: £529.8 million

Griffin Mining provides exposure to a single, producing asset that is currently profitable, with 2025 net income of US$22.06 million and net margins at 16%, up from 8.4% the year before. The company has reported strong recent earnings growth and analysts expect earnings to grow faster than the wider UK market. The stock currently trades below one DCF-based fair value estimate. On the other hand, a high P/E ratio, limited board independence at 17% and a funding profile that relies on external borrowing highlight governance and financial risks that investors may wish to consider. With production potential at Caijiaying reported to extend into 2054, the key consideration is how these strengths and risks compare over time.

Griffin Mining’s single asset profit story, rising margins and below estimate valuation leave one big question hanging over the stock’s trajectory: see how the analyst forecasts for Griffin Mining fits alongside its funding and governance trade offs.

Oxford Instruments (LSE:OXIG)

Overview: Oxford Instruments develops and supplies high end scientific equipment and services, from advanced microscopes and imaging systems to quantum and semiconductor tools, used by universities and commercial labs worldwide to measure, analyze and manufacture at the micro and nano scale.

Operations: Oxford Instruments generates most of its revenue from the Imaging & Analysis division at £314.7 million, with an additional £108.5 million from Advanced Technologies across markets including the USA (£103.9 million), China (£95 million) and wider Europe and Asia.

Market Cap: £1.56b

Oxford Instruments catches the eye because it sits at the crossroads of several long term themes you hear about often, from semiconductors and quantum technologies to high precision tools for energy and life sciences, yet its story is not just one of headline sectors. Earnings rose to £48.2 million on £423.2 million of revenue, margins have improved and analysts expect earnings and revenue growth to outpace the wider UK market, but that progress is balanced against currency headwinds, higher taxes and a funding structure built entirely on external borrowing. The stock trades on a rich P/E and analyst targets only sit modestly above the current price, so the real question is whether the quality of Oxford Instruments’ order book, regional shift toward North America and division level turnaround justify paying up today.

Oxford Instruments sits at the intersection of quantum, semiconductors and imaging. Yet the real story may be how its growth profile compares with a rich P/E and modest price targets, and whether the analyst forecasts for Oxford Instruments suggests that gap could close or widen next.

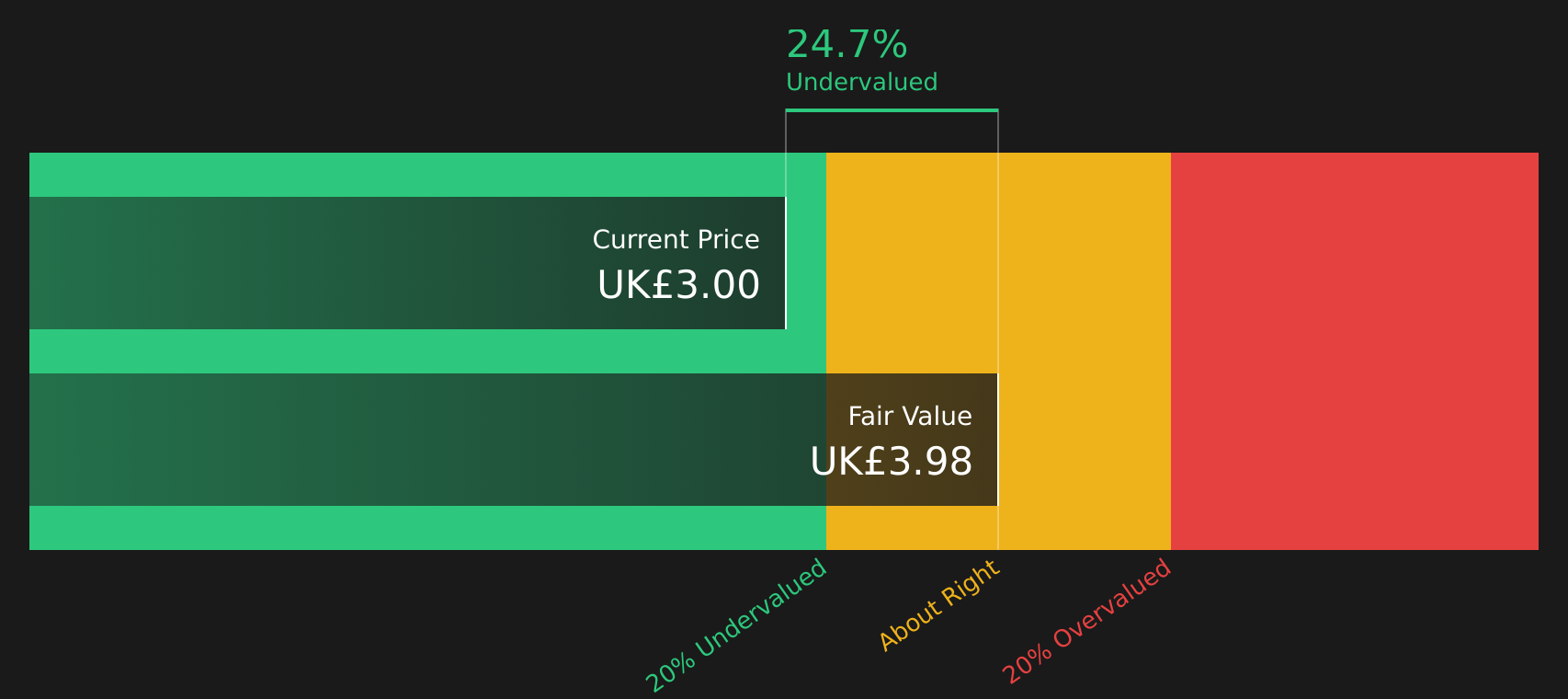

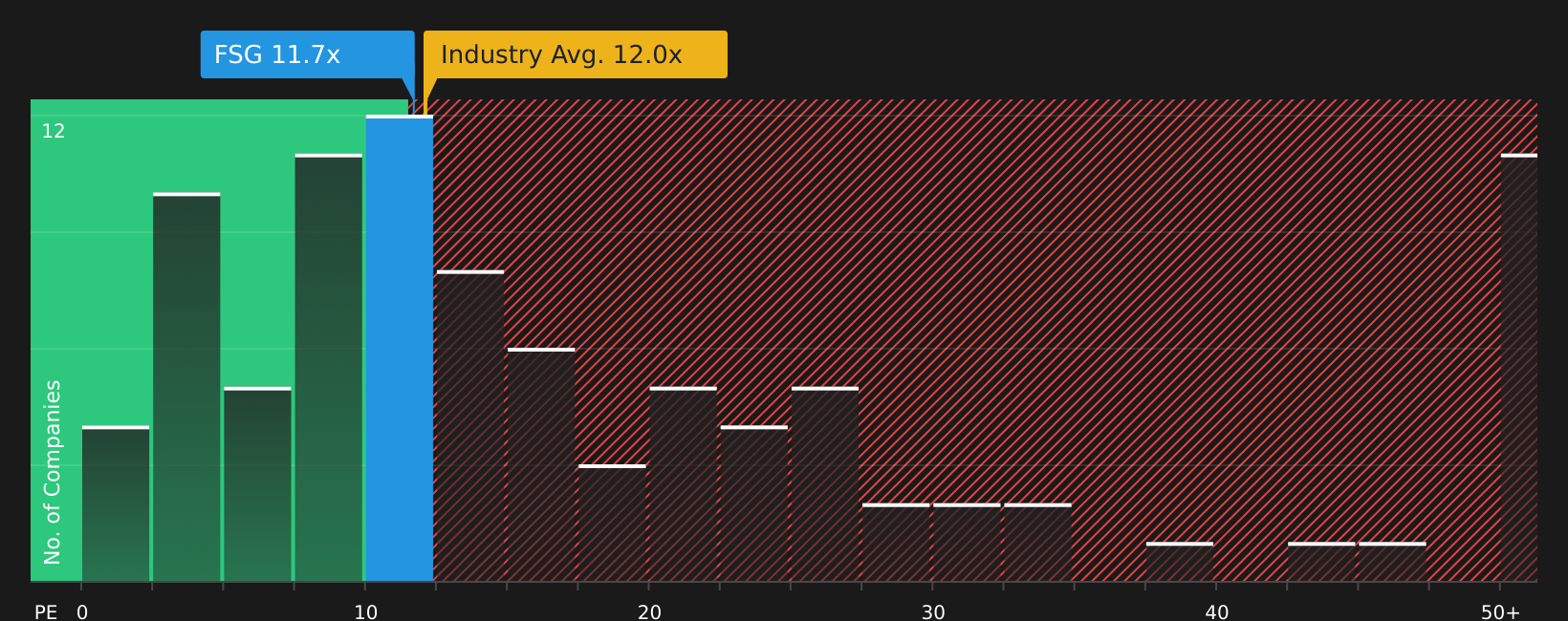

Foresight Group Holdings (LSE:FSG)

Overview: Foresight Group Holdings is a London based asset manager that invests in infrastructure, private equity and venture capital, with a particular focus on renewable energy, social and digital infrastructure, and sustainable real assets for institutional and retail clients.

Operations: Foresight Group Holdings generates £114.8 million of revenue from Real Assets and £50.1 million from Private Equity, with most revenue coming from the United Kingdom at £126.4 million and a further £25.7 million from Australia.

Market Cap: £529.1 million

Foresight Group Holdings may appeal if you want exposure to the energy transition and real assets through an asset manager that is already earning a 27.7% net margin and reports return on equity of 47.8%. The shares trade on a P/E below both peer and industry averages. Analysts have highlighted potential for higher earnings and a re rating, supported by underpenetrated markets, a higher fee product mix and ongoing share buybacks. However, the story is not risk free, with external borrowing, reliance on performance fees and heavy UK and European exposure all worth close attention. The key question is whether Foresight’s plans for scaling assets under management and expanding into new products are sufficient to offset these funding and regulatory pressures over time.

Foresight Group’s high margins and return on equity hint at an earnings engine that many investors may be underestimating. See how the analyst forecasts for Foresight Group Holdings squares with its fee mix and performance driven income before the full picture clicks into place.

The three stocks covered here are only a starting point, and the full Low-Risk Leaders screener surfaces 4 more companies with equally compelling low risk narratives that could help round out your core holdings. Use Simply Wall St to identify and analyze the specific catalysts, balance sheet strength and risk scores that matter to you so you can focus on the highest conviction opportunities in this foundation building group.

Take Control of Your Investment Journey

If Griffin Mining or any of these companies have caught your attention, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value and track any new developments as they happen. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Beyond Today?

Fresh breakout stories and quiet momentum shifts can fly past while you stay locked on familiar stocks. Scan these curated shortlists before the best entry points drop out of reach, and consider acting promptly when opportunities align with your strategy.

- Spot early strength in established operators by checking companies already generating cash flow across the 62 profitable AI stocks that aren't just burning cash before the crowd starts chasing the next AI headline.

- Hunt for income ideas that aim to pay you while you hold by filtering companies in the 5 dividend fortresses before yields change as more investors take notice.

- Track companies positioned in a crucial part of tomorrow’s energy system by reviewing the 90 nuclear energy infrastructure stocks while these stories may still be under the radar.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com