3 US Materials Stocks Investors Are Watching as Tariff Pressure Builds

Potential new US tariffs on Canadian goods linked to the wildfire fallout are putting fresh attention on US materials and building supplies stocks. Higher input costs on items like aluminum and lumber, possible retaliation from Canada, and legal uncertainty around tariff authority all feed into pricing power, margins, and project demand. For investors, that tension can create both pressure and opportunity, depending on how each company sources materials and manages risk. This article walks through 3 US materials and building supplies stocks exposed to this tariff story, each with business models that could be positively affected if current conditions persist or intensify.

REalloys (ALOY)

Overview: REalloys is a North American rare earth metals and permanent magnet producer, supplying elements like neodymium, dysprosium and scandium, as well as high performance magnets used in defense, aerospace, automotive and industrial applications. Founded in 2024 and based in Ohio, the company is positioning itself as a domestic source of materials that are often imported from abroad.

Market Cap: US$673.4 million

Investors watching US materials stocks for potential tariff beneficiaries may find REalloys interesting because it is focused on North American rare earth supply at a time when new US tariffs on Canadian inputs could push buyers to domestic sources. The company is still very early stage, with revenue of less than US$1 million in 2025 and sizeable losses, and auditors have raised going concern questions, so the risk profile is high. At the same time, revenue growth has been very large off this small base. Analyst expectations in available research point to the possibility of positive earnings within the next several years, and REalloys has secured partnerships with the U.S. Army and multiple feedstock providers that could be important if policy continues to favor domestic critical minerals.

REalloys is an early-stage, high-risk company tied to US critical mineral policy. This makes understanding its potential upside particularly important, so review the 2 key rewards and 3 important warning signs (1 is major!)

TriMas (TRS)

Overview: TriMas is a Michigan based industrial company that designs and manufactures packaging dispensers, closures, and steel gas cylinders used in everyday consumer products, aerospace and defense applications, and a range of industrial uses around the world.

Operations: TriMas generates most of its revenue from its Packaging segment at US$547.1 million, with an additional US$114.4 million coming from its Specialty Products steel cylinder business.

Market Cap: US$1.5b

TriMas catches attention because it combines a large, global packaging platform with benefits of being a domestic supplier at a time when new US tariffs on Canadian inputs could push more demand toward US made components. Management is focused on improving margins through automation and integration, and analysts expect earnings growth to outpace its more modest revenue outlook, supported by an active buyback program and a small dividend. At the same time, a high P/E relative to packaging peers, reliance on external borrowing, tariff exposure across its global footprint, and recent insider selling mean investors need to weigh execution and policy risks carefully before deciding how TriMas fits into a portfolio focused on resilient materials and building supply stocks.

TriMas’ earnings story, margin focus and tariff exposure raise big questions about how much is already priced in. Review the analyst forecasts for TriMas to see what might be hiding behind the headline numbers.

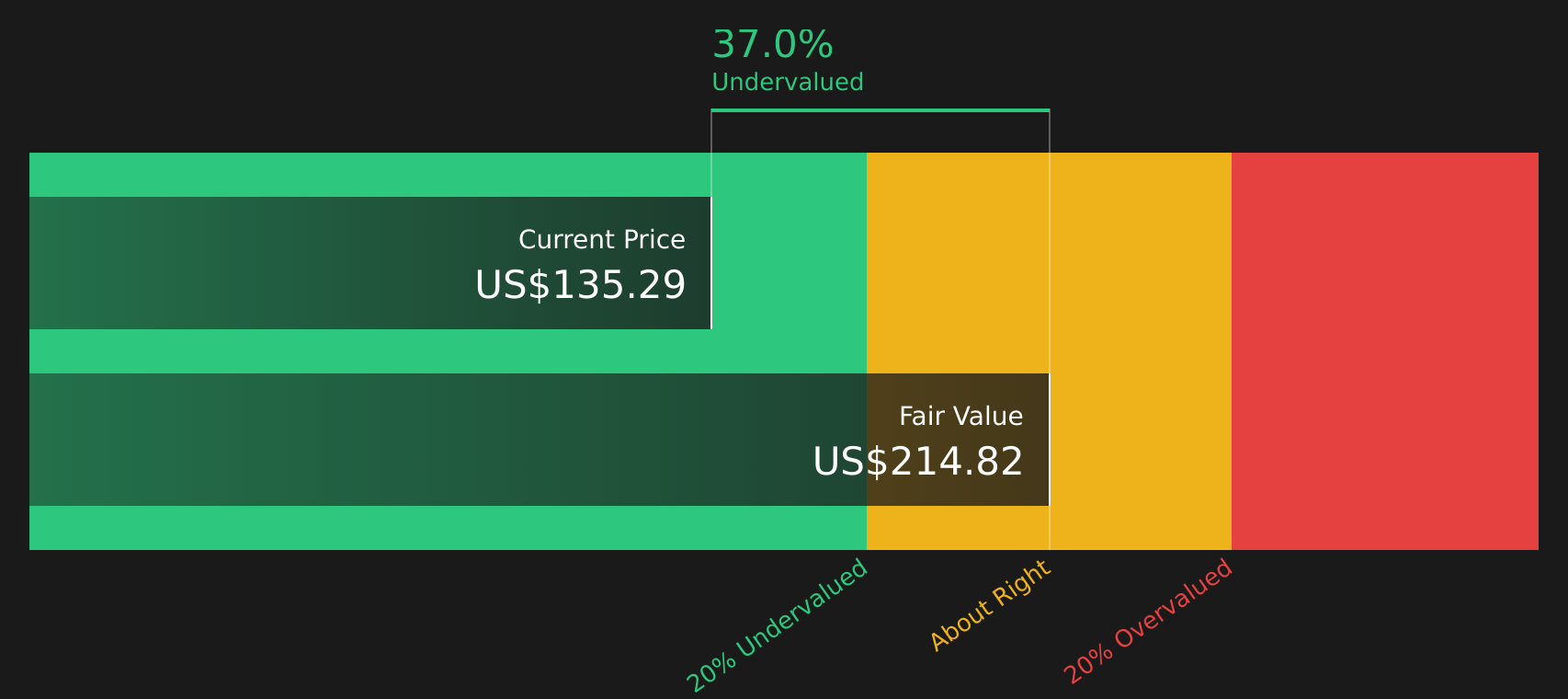

DuPont de Nemours (DD)

Overview: DuPont de Nemours is a US based materials and chemicals company that supplies high performance products for healthcare, water treatment, construction, electronics, automotive, aerospace and protective garments, including brands such as Tyvek, Styrofoam insulation and Corian surfaces.

Operations: DuPont de Nemours generates US$3.6b of revenue from its Diversified Industrials segment and US$3.3b from Healthcare & Water Technologies.

Market Cap: US$18.1b

Investors watching US materials stocks for potential tariff beneficiaries may want DuPont de Nemours on the radar because it couples a large US manufacturing footprint with specialty products that sit at the intersection of construction, healthcare and clean water, areas that remain in focus even as trade rules shift. The recent move back to profitability, earnings growth forecasts in the low 20% range and a Simply Wall St valuation estimate above the current share price create an interesting contrast with a high P/E, PFAS legal overhang and heavy use of external borrowing. How that balance plays out if US sourced materials gain more pricing power under fresh tariff pressure is a key question for anyone considering DuPont in this screener.

DuPont de Nemours looks like earnings momentum and a Simply Wall St fair value estimate could be masking one crucial detail about its risk reward trade off, start with the 4 key rewards and 2 important warning signs

The three US materials and building supplies stocks covered here are only a starting point, as the full US Domestic Materials and Building Supplies screener surfaces 25 more companies with equally compelling narratives around domestic sourcing, balance sheet strength and tariff exposure. Use Simply Wall St to identify, filter and analyze the specific catalysts that matter to you so you can focus on the highest conviction US materials and building supplies plays without getting buried in noise.

Take Control of Your Investment Journey

If DuPont de Nemours or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Beyond Tariff Plays?

Tariff exposed stocks may not stay under the radar for long, and once momentum is flying, early entry can vanish before the crowd notices, so timing is important.

- Spot smaller opportunities before they become headlines by running through the curated 20 high quality undiscovered gems while they are still under the radar for now.

- Capture income ideas that aim to keep paying even when markets are choppy by scanning the hand picked 8 dividend fortresses right as yields look most appealing.

- Position ahead of potential infrastructure momentum by checking the focused 33 power grid technology and infrastructure stocks while it still reflects early stage build out stories, not crowded trades.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com