MannKind (MNKD) Stock Stays Cheap On Its 28% YTD Slump

MannKind stock has fallen 28.0% year to date, yet valuation checks suggest the market price may still sit below an estimate of intrinsic value based on a Discounted Cash Flow (DCF) approach and earnings multiples. For investors, that sets up a tension between weak recent returns and signals that both the intrinsic value estimate and market multiples point to undervaluation.

- Year to date, MannKind is down 28.0%, which means any case for upside now relies more on valuation support than on recent share price momentum.

- The recent FDA approval expanding Afrezza to pediatric use can support expectations for MannKind's future cash flows, while the risks around execution of clinical studies and real world adoption may still weigh on how investors price that potential.

- MannKind screens as undervalued across 4 of 6 valuation checks, a mixed picture that leans toward the stock being cheaper than many of its fundamentals alone might suggest, according to the valuation summary.

The issue now is whether MannKind's current share price already reflects this DCF based intrinsic value estimate or still leaves a meaningful margin between market price and fundamentals.

Find out why MannKind's 7.2% return over the last year is lagging behind its peers.

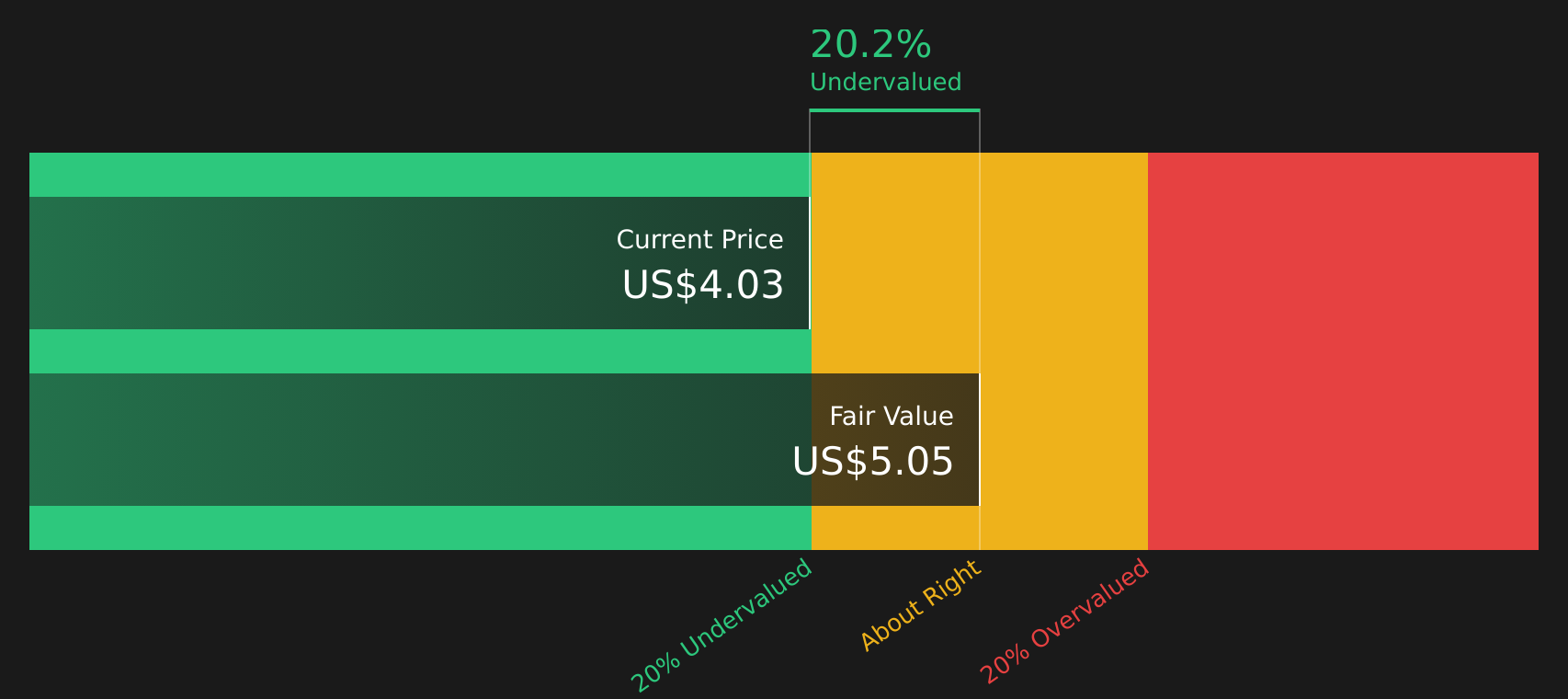

Is MannKind Still Cheap on Cash Flow?

The Discounted Cash Flow (DCF) model here values MannKind based on projected cash that could flow to shareholders. The latest twelve month free cash flow is a loss of $1.27 million, so the model assumes that cash generation recovers and grows from that low base over time. On those projections, the DCF points to an estimated intrinsic value of about $5.09 per share.

Against the current share price, this implies MannKind trades at roughly a 20.8% discount to that DCF estimate, which indicates that the market price sits below what the cash flow model supports. Because the recent FDA approval expanding Afrezza to pediatric use introduces a fresh potential growth driver, yet the stock still screens below the intrinsic value estimate, the price gap appears more tied to execution and adoption risks than to the absence of potential cash flows.

On this cash flow view, MannKind stock currently appears undervalued relative to the model’s estimate of intrinsic value.

Our Discounted Cash Flow (DCF) analysis suggests MannKind is undervalued by 20.8%. Track this in your watchlist or portfolio, or discover 47 more high quality undervalued stocks.

Is MannKind a Bargain on Sales?

The P/S multiple is often a cleaner way to look at MannKind because revenue is in place even while profits and free cash flow are still uneven.

MannKind currently trades at a P/S of 3.5x, which is below the broader Biotechs industry average of 11.3x and slightly above the peer group average of 3.3x. A Fair P/S Ratio of 5.0x, which reflects MannKind's specific mix of growth prospects, margins, size and risk profile, sits meaningfully higher than where the stock is priced today.

On this framework, MannKind would screen as cheaper than what that tailored fair multiple implies, suggesting the current valuation does not fully reflect the revenue base and expectations embedded in the model.

On the preferred P/S multiple, MannKind stock appears inexpensive relative to the fair ratio suggested by its own fundamentals and risk profile.

See what the numbers say about this price — find out in our valuation breakdown.

The MannKind Narrative: What Would Justify Today's Price?

Simply Wall St Narratives for MannKind pick up where the valuation checks stop. They set out the specific assumptions on MannKind's future growth, margins and earnings that would need to hold for the stock to be worth meaningfully more or less than today's price on the Community page. Instead of a single output from a ratio or model, Narratives lay out the underlying future those numbers rely on, so you can watch in real time whether the story they describe is actually playing out.

One of the top community narratives on MannKind: 47% undervalued

"Afrezza's growth, new indications, and expanded global reach support higher revenue, with inhaled pipeline progress promising significant future diversification…"

Read one of the top narratives on MannKind

Do you think there's more to the story for MannKind? Head over to our Community to see what others are saying!

The Bottom Line

For MannKind, both the Discounted Cash Flow (DCF) intrinsic value estimate and the P/S based view currently lean toward the stock looking undervalued, even if the broader valuation checks are only mixed rather than emphatic. That means the market is still pricing in meaningful uncertainty around execution, especially on Afrezza's broader use and the pipeline's progress, despite model based support for a higher valuation. What matters from here is whether MannKind can translate its existing products and approvals into steadier cash generation. This would help show whether the current discount is an opportunity or a sign that the risks remain appropriately priced in.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com