The Bull Case For Transcontinental (TSX:TCL.A) Could Change Following METRO Contract Renewal News – Learn Why

- In December 2025, Transcontinental Inc. announced a three-year extension of its agreement to provide METRO with marketing services, including continued participation in its raddar® flyer in both print and digital formats across Quebec and potential additional Canadian markets, alongside broader printing, in-store marketing, and content solutions.

- This renewed commitment with a large grocery retailer underscores the resilience of Transcontinental’s marketing platform and strengthens the visibility of a key revenue stream within its Retail Services and Printing operations.

- We’ll now examine how the renewed multi-year METRO contract could influence Transcontinental’s investment narrative and expectations for earnings stability.

The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 25 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

Transcontinental Investment Narrative Recap

To own Transcontinental, you need to believe its mix of flexible packaging and resilient Retail Services and Printing can offset volume pressure and regional headwinds. The renewed three-year METRO contract supports the near term earnings stability story, but does not fully resolve the overarching risk of structurally lower volumes in packaging and flyer-related businesses.

The recent 10 year renewal of the Globe and Mail printing agreement is especially relevant here, because it reinforces the same theme as METRO: multi year visibility on core printing volumes while the company continues cost optimization and raddar rollout across its Retail Services and Printing operations.

Yet despite these long term contracts, investors should still be aware of the risk that...

Read the full narrative on Transcontinental (it's free!)

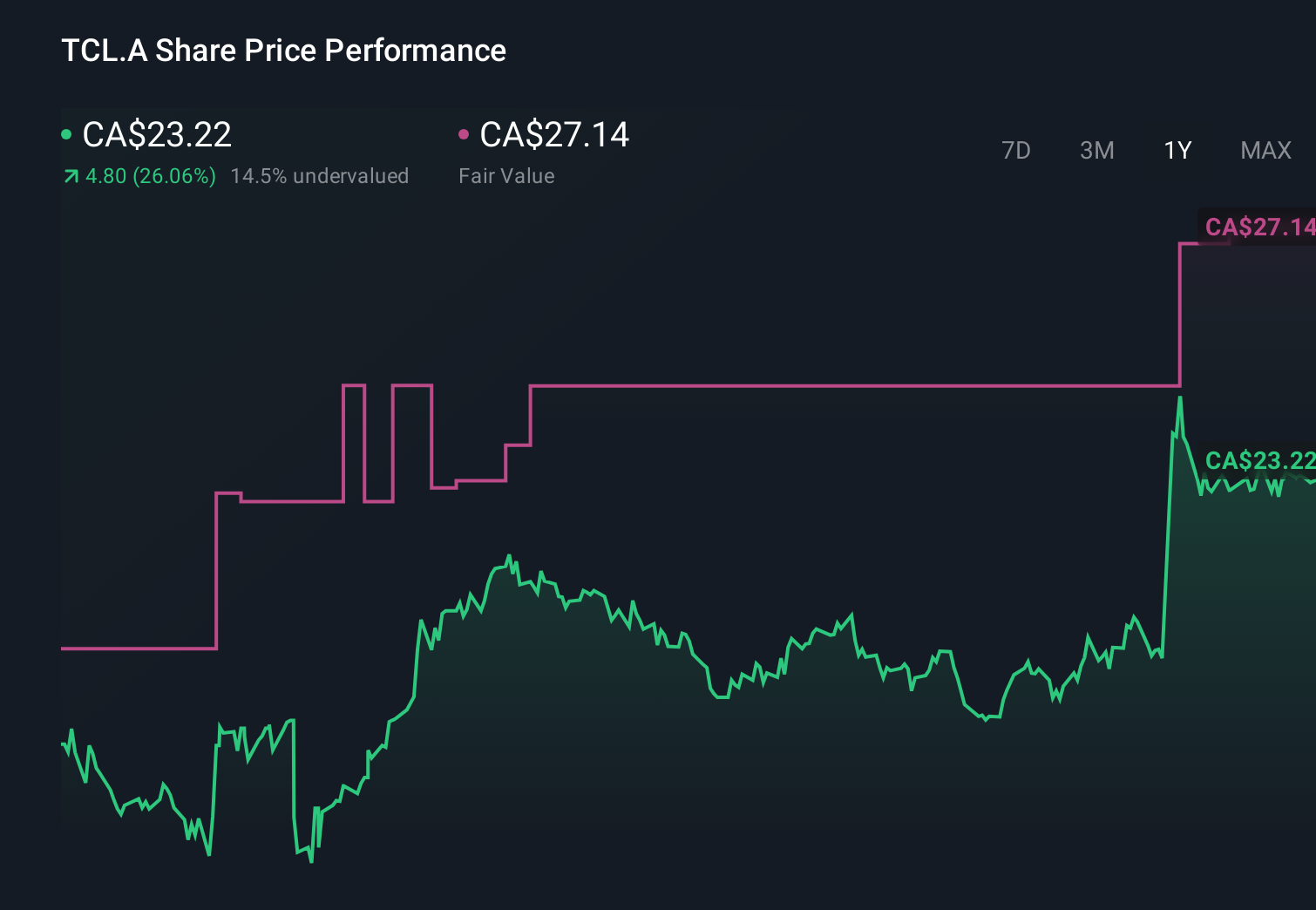

Transcontinental's narrative projects CA$2.8 billion revenue and CA$170.9 million earnings by 2028.

Uncover how Transcontinental's forecasts yield a CA$27.14 fair value, a 17% upside to its current price.

Exploring Other Perspectives

Three fair value estimates from the Simply Wall St Community currently span about C$14.50 to C$27.14, showing how far apart individual views can be. When you set that against the risk of ongoing volume declines in packaging and retail services, it underlines why many investors choose to compare several independent viewpoints before making up their mind.

Explore 3 other fair value estimates on Transcontinental - why the stock might be worth as much as 17% more than the current price!

Build Your Own Transcontinental Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Transcontinental research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Transcontinental research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Transcontinental's overall financial health at a glance.

Ready For A Different Approach?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

- Find companies with promising cash flow potential yet trading below their fair value.

- Rare earth metals are the new gold rush. Find out which 38 stocks are leading the charge.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com