Assessing Amylyx Pharmaceuticals (AMLX) Valuation After Insider Buying And AMX0114 Trial Progress

Amylyx Pharmaceuticals (AMLX) is back in focus after a director bought more than $100,000 of company stock, alongside encouraging early safety data from its AMX0114 ALS program and an expansion of a related clinical trial.

See our latest analysis for Amylyx Pharmaceuticals.

Despite the director buying and the AMX0114 updates, recent trading has been weak, with a 30 day share price return of a 19.58% decline and a 90 day return of a 15.34% decline, while the 1 year total shareholder return of 191.33% sits against a 3 year total shareholder return of a 67.90% decline. This suggests strong shorter term momentum following earlier longer term weakness.

If this kind of clinical news has your attention, it could be a good moment to look across other healthcare stocks that are moving on key trial and pipeline updates.

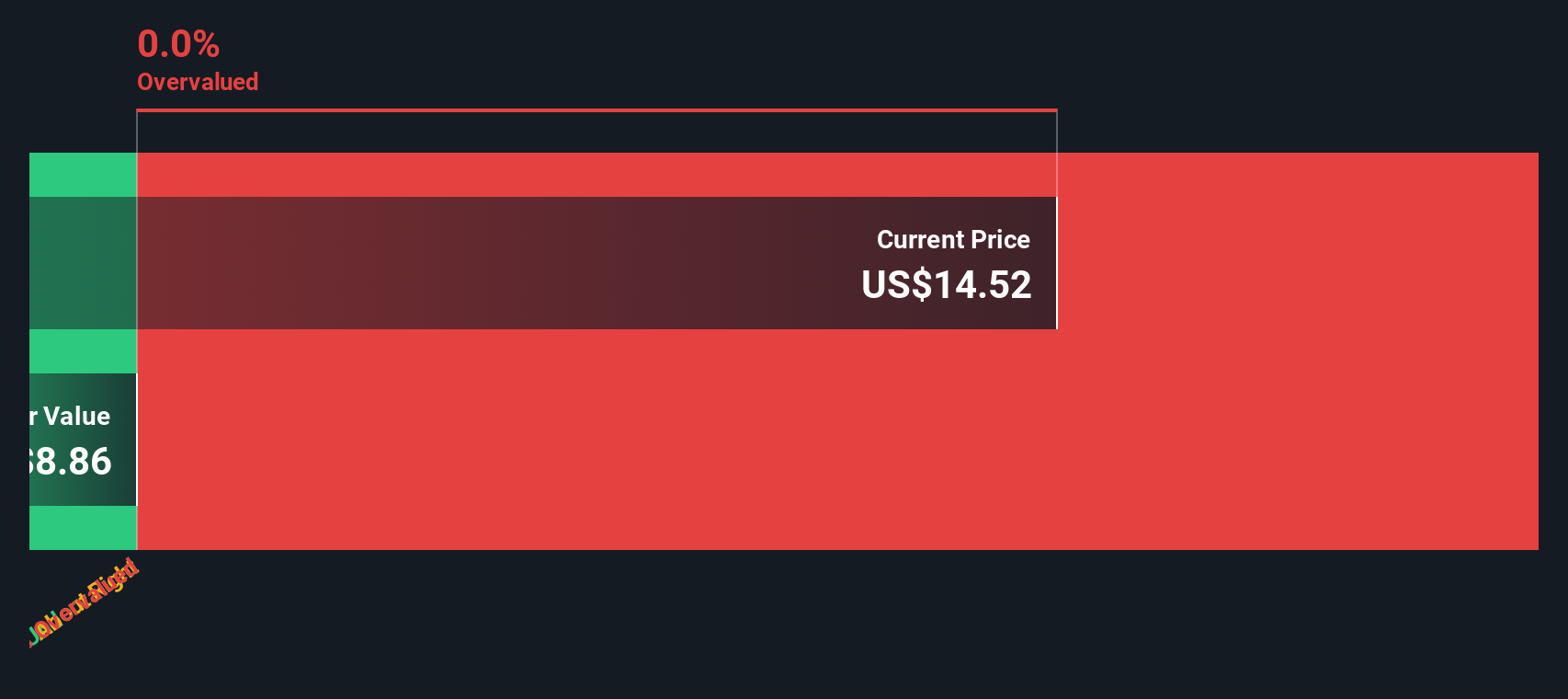

With Amylyx trading at US$11.42 and implied to sit at a steep discount to analyst targets and intrinsic value estimates, the key question is whether this gap reflects an opportunity or if the market already sees limited future growth.

Price to Book of 3.8x: Is it justified?

On a P/B of 3.8x at a last close of US$11.42, Amylyx looks expensive versus the broader US pharmaceuticals group, yet cheaper than its closer peers.

P/B compares a company's market value to its book value. This is particularly watched for drug developers where tangible assets and cash on hand matter more than current earnings. For Amylyx, this lens is useful because the business is still unprofitable and early in commercialisation, so earnings-based metrics like P/E are less meaningful.

Simply Wall St data flags that Amylyx trades on a P/B of 3.8x, above the US pharmaceuticals industry average of 2.6x. This suggests the market is paying a premium relative to many sector names. However, the same data also notes that 3.8x is below a 5.9x peer average set, indicating that within a closer comparison group investors are paying less for each dollar of book value.

See what the numbers say about this price — find out in our valuation breakdown.

Result: Price-to-book of 3.8x (ABOUT RIGHT)

However, this depends on a pipeline that is still in clinical trials, so any disappointing data or delays could quickly challenge the current valuation gap.

Find out about the key risks to this Amylyx Pharmaceuticals narrative.

Another take using our DCF model

While P/B at 3.8x points to Amylyx as roughly in line with peers, our DCF model presents a very different picture, with the shares trading about 78.2% below an estimated fair value of US$52.44. That kind of gap raises a simple question: is the market too cautious about future cash flows?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Amylyx Pharmaceuticals for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 875 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Amylyx Pharmaceuticals Narrative

If you interpret the numbers differently or prefer to stress test every assumption yourself, you can build a custom view in just a few minutes by starting with Do it your way.

A great starting point for your Amylyx Pharmaceuticals research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

Ready for more investment ideas?

If Amylyx has sharpened your thinking, do not stop here. Broadening your watchlist now can help you spot opportunities before they become crowded.

- Spot potential high risk high reward names early by scanning these 3571 penny stocks with strong financials that already show stronger underlying financials.

- Zero in on cash flow focused opportunities using these 875 undervalued stocks based on cash flows to surface companies where prices and fundamentals appear out of sync.

- Tap into the intersection of medicine and algorithms with these 29 healthcare AI stocks highlighting companies applying AI to real world healthcare problems.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com