Assessing Wells Fargo (WFC) Valuation After Strong Recent Share Price Returns

Why Wells Fargo is on investors’ radar today

Wells Fargo (WFC) is drawing attention after a recent move in its share price, prompting investors to reassess how its current valuation lines up with its recent returns and fundamentals.

See our latest analysis for Wells Fargo.

That latest move comes after a steady run, with the share price at US$95.20 and a 90 day share price return of 17.33% alongside a 1 year total shareholder return of 35.04%, suggesting momentum has been building.

If Wells Fargo’s recent gains have you reviewing your portfolio, it could be a good moment to compare it with other leading banks and financials using fast growing stocks with high insider ownership.

With Wells Fargo trading near its analyst price target and an estimated intrinsic discount of about 21%, the key question is whether the recent 35.04% 1 year return leaves further upside or if the market is already pricing in future growth.

Most Popular Narrative Narrative: 0.7% Overvalued

Compared with the last close at US$95.20, the most followed narrative pegs Wells Fargo’s fair value at US$94.50, suggesting the current price is slightly ahead.

The analysts have a consensus price target of $87.0 for Wells Fargo based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $95.0, and the most bearish reporting a price target of just $72.0.

Want to see what is baked into that near inline value? The narrative leans heavily on compounded earnings, steady margins, and a richer future earnings multiple. Curious?

Result: Fair Value of $94.50 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, there is still the risk that slower digital execution or lingering regulatory and compliance costs could cap profitability and limit how much investors are willing to pay.

Find out about the key risks to this Wells Fargo narrative.

Another View: Market P/E Sends a Different Signal

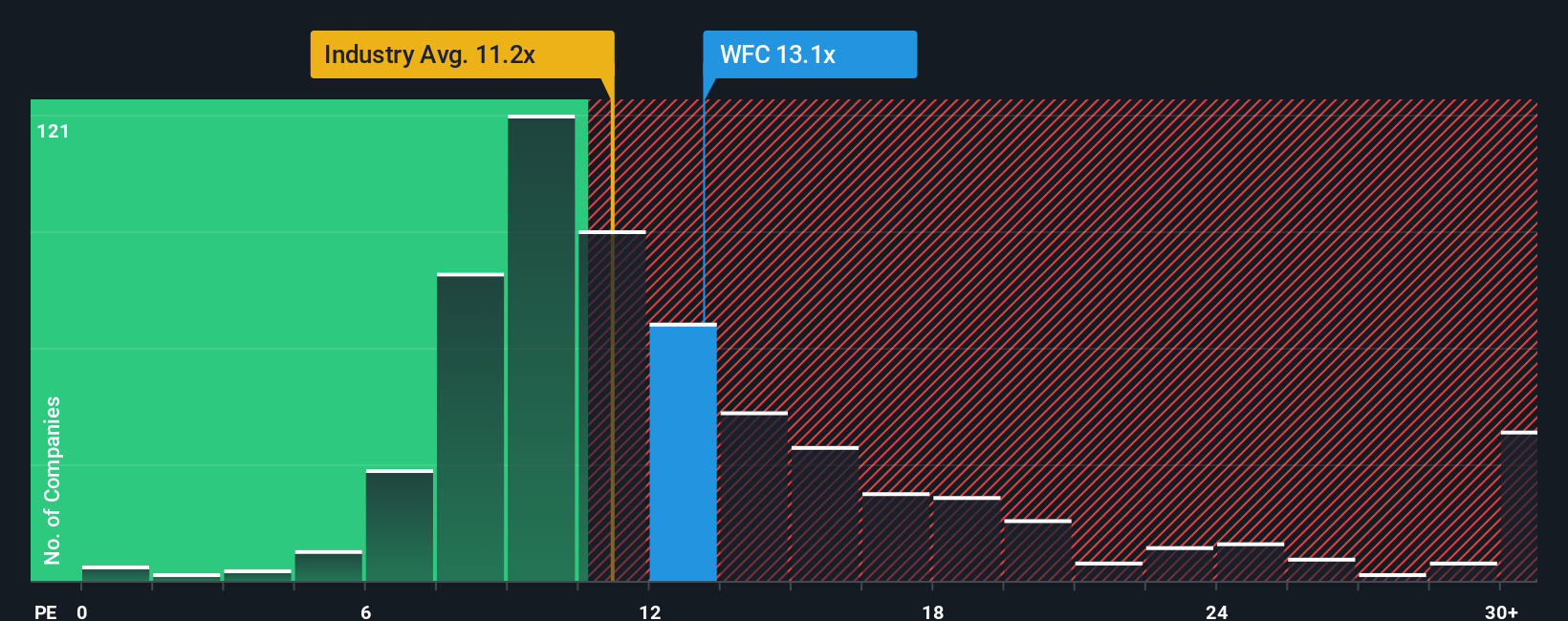

While the narrative fair value of US$94.50 frames Wells Fargo as 0.7% overvalued, the P/E picture is less one sided. The shares trade on 15x earnings versus a fair ratio of 16.1x, yet above peers at 14x and the wider US banks at 11.8x. Is the market paying up for quality or just paying too much?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Wells Fargo Narrative

If you see the story differently, or simply prefer to weigh the numbers yourself, you can build a custom view in just a few minutes. Start with Do it your way.

A great starting point for your Wells Fargo research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If Wells Fargo has you thinking more carefully about your next move, do not stop here. Broaden your watchlist with focused stock ideas tailored to different themes.

- Spot potential value with these 870 undervalued stocks based on cash flows that line up with your view on pricing and cash flows.

- Zero in on income opportunities by checking out these 14 dividend stocks with yields > 3% that might fit a yield focused approach.

- Get ahead of emerging trends by reviewing these 79 cryptocurrency and blockchain stocks shaping parts of the digital asset space.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com