What Devon Energy (DVN)'s Analyst Upgrades and Bakken Capital Efficiency Focus Mean For Shareholders

- In recent weeks, Roth/MKM reaffirmed its positive rating on Devon Energy after reviewing its 2026 output model and capital efficiency in the Bakken, while UBS upgraded the stock on expectations of an improved oil backdrop and planned US$1.00 billion debt reduction around mid-2026.

- These analyst views emphasize how Devon’s operational data and balance sheet plans are shaping sentiment around its ability to manage commodity cycles and capital needs.

- Now, we'll explore how renewed analyst confidence tied to Devon's Bakken capital efficiency could influence the company's broader investment narrative.

We've found 14 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

Devon Energy Investment Narrative Recap

To own Devon Energy, you need to be comfortable with a business that is tightly linked to U.S. shale productivity and commodity prices, while counting on its capital efficiency to support cash flows and shareholder returns. The recent analyst updates around Bakken efficiency and planned debt reduction reinforce this focus on disciplined capital use, but they do not fundamentally change the key near term catalyst, which remains execution on cost control, or the primary risk from ongoing exposure to volatile oil and gas prices.

Against this backdrop, Devon’s ongoing share repurchase program, which has retired more than 14% of its shares since 2021, is the announcement that most directly ties into the current analyst optimism around capital discipline and debt reduction. How effectively Devon balances continued buybacks, its growing fixed dividend, and the planned US$1,000,000,000 debt paydown will be central to how resilient its investment case looks if commodity prices weaken again.

Yet investors should also understand how quickly high decline shale wells can pressure Devon’s capital needs if...

Read the full narrative on Devon Energy (it's free!)

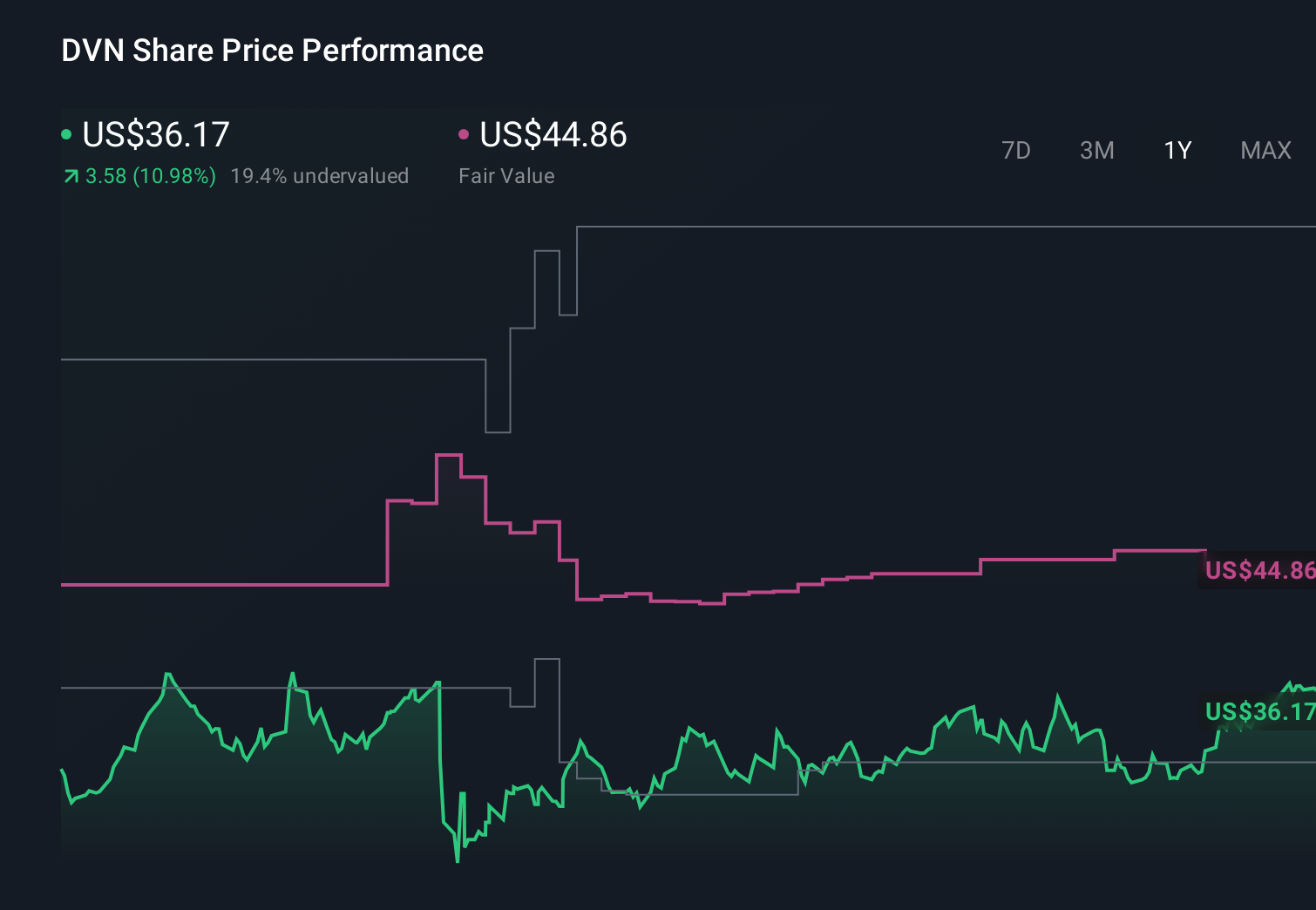

Devon Energy's narrative projects $19.3 billion revenue and $3.0 billion earnings by 2028.

Uncover how Devon Energy's forecasts yield a $44.86 fair value, a 18% upside to its current price.

Exploring Other Perspectives

Members of the Simply Wall St Community have published 11 fair value estimates for Devon, spanning roughly US$31 to US$117 per share. These differing views sit alongside the central catalyst of improving drilling efficiency, reminding you to weigh multiple outlooks on how that could influence future cash flows.

Explore 11 other fair value estimates on Devon Energy - why the stock might be worth over 3x more than the current price!

Build Your Own Devon Energy Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Devon Energy research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Devon Energy research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Devon Energy's overall financial health at a glance.

Looking For Alternative Opportunities?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- These 14 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com