A Look At APi Group (APG) Valuation After Share Issuance For Preferred Dividend

APi Group (NYSE:APG) has reshaped its share base by issuing 15,212,810 new common shares to satisfy the 2025 annual dividend on its Series A preferred stock, resulting in modest dilution for existing common shareholders.

See our latest analysis for APi Group.

At a share price of $38.97, APi Group’s recent 12.89% 90 day share price return sits alongside a very strong 1 year total shareholder return of 60.24% and a 5 year total shareholder return of 245.48%. This points to momentum that has been building rather than fading as investors reassess growth prospects and risk around moves like the preferred dividend share issuance.

If this kind of restructuring has you thinking about where else capital might work hard, it could be worth widening your search with fast growing stocks with high insider ownership.

With APi Group trading at $38.97, sitting below the US$43.40 analyst price target and with an indicated 33.55% intrinsic discount, the key question is whether this represents a genuine opportunity or if the market already reflects future growth.

Most Popular Narrative Narrative: 9.2% Undervalued

With APi Group last closing at $38.97 against a widely followed fair value estimate of about $42.90, the narrative frames the shares as discounted while hinging on a sharp shift in profitability and valuation expectations.

The analysts have a consensus price target of $41.0 for APi Group based on their expectations of its future earnings growth, profit margins and other risk factors. In order for you to agree with the analyst's consensus, you would need to believe that by 2028, revenues will be $8.9 billion, earnings will come to $746.5 million, and it would be trading on a PE ratio of 30.1x, assuming you use a discount rate of 8.7%.

Curious what kind of revenue mix, margin expansion and earnings ramp support that valuation path, and how those assumptions tie back to today’s price? The full narrative lays out the specific growth, profitability and valuation hurdles that need to line up for APi Group to close that gap.

Result: Fair Value of $42.90 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, there are still hinges in this story, including pressure on materials and labor costs, as well as the risk that acquisitions or digital projects do not deliver as expected.

Find out about the key risks to this APi Group narrative.

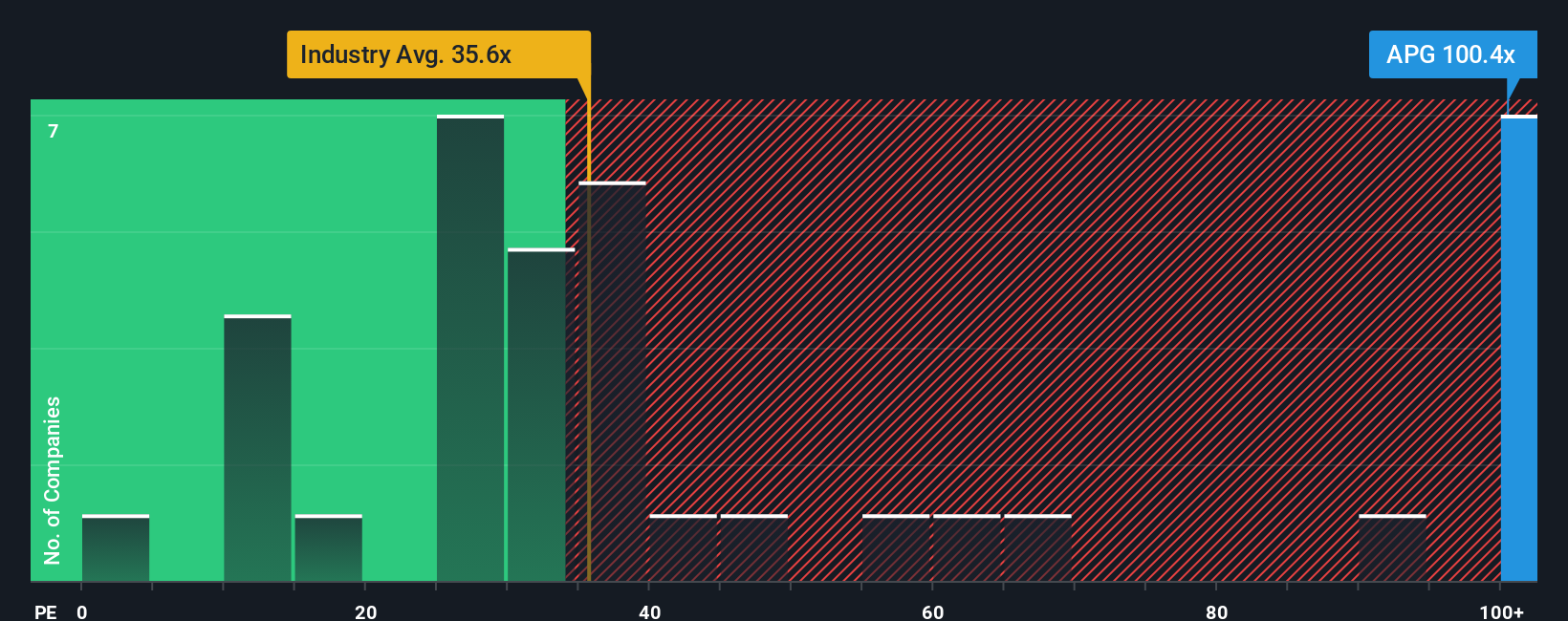

Another View: What The P/E Ratio Is Saying

There is also a very different read coming from the P/E ratio. APi Group trades on about 103.9x earnings, while the US Construction industry sits closer to 30.5x and a fair ratio for the shares is estimated at 54.2x. That gap suggests investors are paying a heavy premium today. How comfortable are you with that kind of valuation stretch if expectations change?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own APi Group Narrative

If you interpret the numbers differently or want to test your own assumptions, you can build a custom APi Group story in just a few minutes, starting with Do it your way.

A great starting point for your APi Group research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If APi Group has sharpened your focus, now is the time to broaden your watchlist so potential opportunities do not slip past you while attention is elsewhere.

- Spot potential mispricing by scanning these 870 undervalued stocks based on cash flows that may offer a wider margin between share prices and their underlying cash flow strength.

- Ride powerful tech trends by zeroing in on these 25 AI penny stocks that connect artificial intelligence themes with listed companies.

- Expand your income watchlist by reviewing these 14 dividend stocks with yields > 3% that combine higher yields with listed equity exposure.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com