Is It Time To Reassess Estée Lauder (EL) After Its 45% One Year Share Price Rebound

- If you are wondering whether Estée Lauder Companies is still worth considering at around US$105.27, the key question is how that price stacks up against its underlying value.

- The stock has returned 0.5% over the last 7 days and 2.4% over the past month, sits on a 1.4% decline year to date, yet is up 45.4% over the last year. However, the 3 year and 5 year returns of 57.8% and 55.9% declines show a very different longer term picture.

- Recent headlines have focused on Estée Lauder's position in premium beauty and its efforts to adjust to changing consumer demand across key regions, including travel retail and skincare. At the same time, investors have been reacting to updates around brand performance and cost efficiency, which helps explain some of the share price volatility seen in recent years.

- Simply Wall St's valuation model currently gives Estée Lauder Companies a value score of 1 out of 6, which means it screens as undervalued on just one of six checks. The rest of this article will walk through what different valuation methods say about that price, before finishing with a broader way to think about valuation that goes beyond the numbers alone.

Estée Lauder Companies scores just 1/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

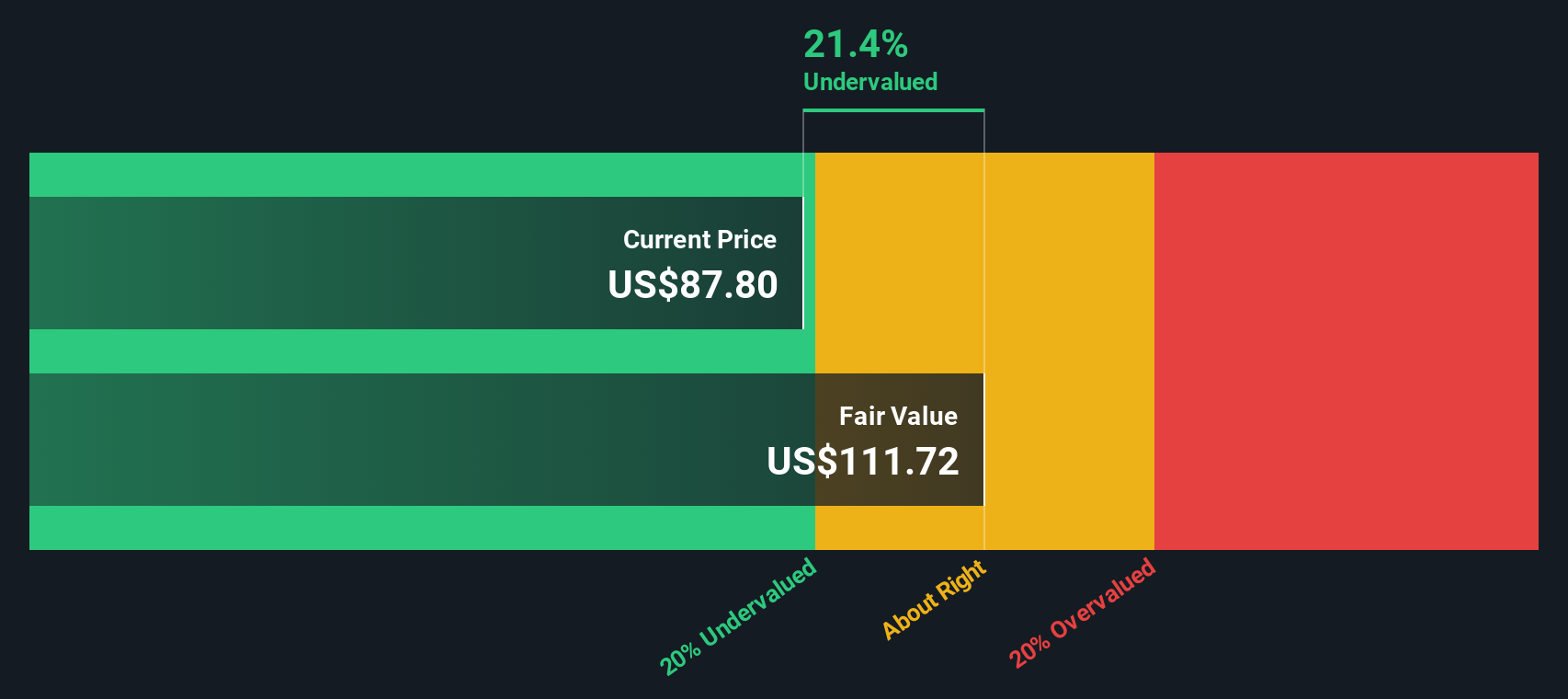

Approach 1: Estée Lauder Companies Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model takes Estée Lauder Companies’ expected future cash flows and discounts them back into today’s dollars to estimate what the entire business might be worth right now.

In this model, Estée Lauder Companies is valued using a 2 Stage Free Cash Flow to Equity approach. The latest twelve month free cash flow is about $816.6 million. Analysts and internal estimates project free cash flow rising to $1,998 million by 2030, with a detailed path that includes projected free cash flow of $573.3 million in 2026 and $1,336.6 million in 2027. Simply Wall St uses direct analyst inputs for the nearer years and then extends the trend to build a full 10 year cash flow profile.

When all those projected cash flows are discounted back and aggregated, the model arrives at an estimated intrinsic value of about $109.48 per share. Compared with the current share price of around $105.27, the DCF output indicates the stock is trading at roughly a 3.8% discount, which is a small gap.

Result: ABOUT RIGHT

Estée Lauder Companies is fairly valued according to our Discounted Cash Flow (DCF), but this can change at a moment's notice. Track the value in your watchlist or portfolio and be alerted on when to act.

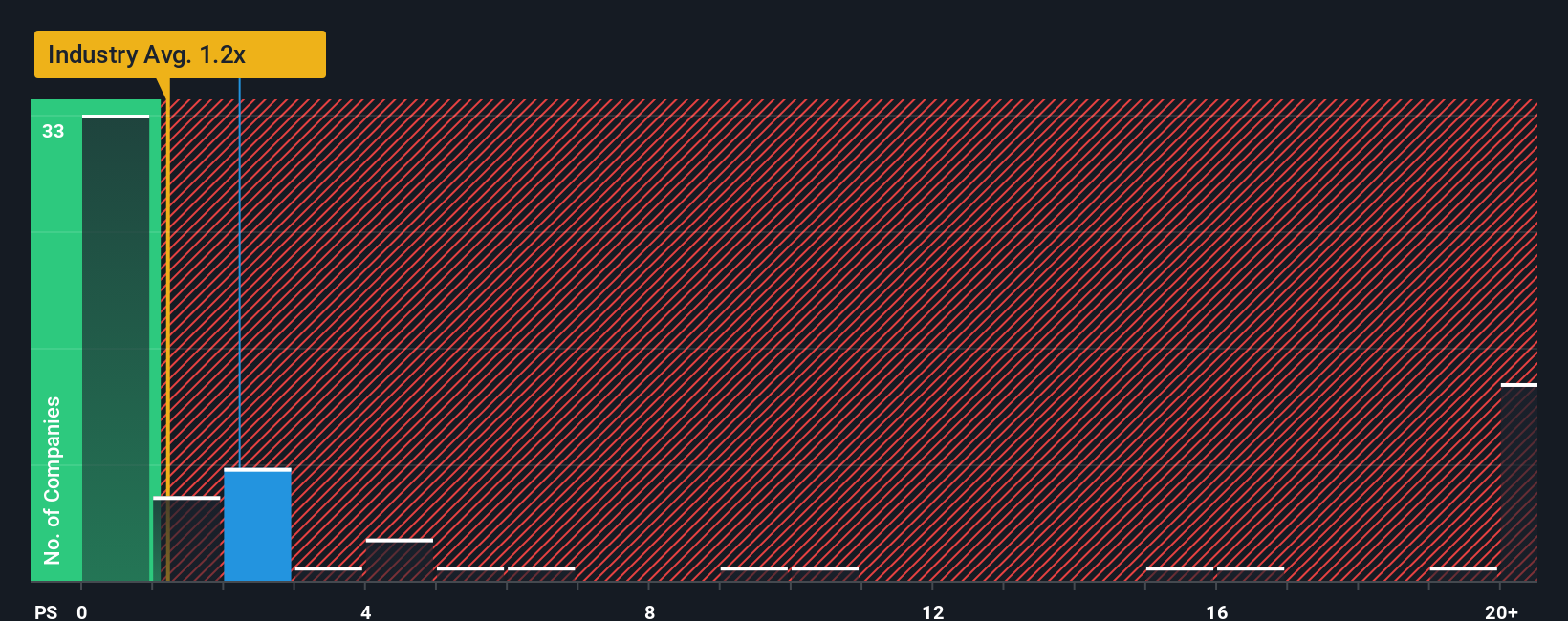

Approach 2: Estée Lauder Companies Price vs Sales

For companies where profits can be uneven, the P/S ratio is often a useful cross check because it compares what investors are paying to the revenue the business generates, rather than to short term earnings swings.

What counts as a “normal” or “fair” P/S ratio usually reflects how quickly investors expect sales to grow and how much risk they see in those expectations. Higher growth and perceived resilience often justify a higher multiple, while slower growth or higher risk tend to point to a lower one.

Estée Lauder Companies currently trades on a P/S of 2.63x. That sits above the Personal Products industry average of 0.81x and above the peer group average of 1.41x. Simply Wall St also calculates a proprietary “Fair Ratio” of 2.17x, which is the P/S level it estimates for Estée Lauder Companies after weighing factors such as revenue growth expectations, margins, industry, market cap and risk profile.

This Fair Ratio can be more tailored than a simple peer or industry comparison because it adjusts for company specific characteristics rather than assuming one size fits all. Setting the actual 2.63x P/S against the 2.17x Fair Ratio suggests the stock is trading above that tailored estimate.

Result: OVERVALUED

P/S ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1449 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Estée Lauder Companies Narrative

Earlier we mentioned that there is an even better way to understand valuation. On Simply Wall St’s Community page you can explore Narratives, where investors lay out a clear story for Estée Lauder Companies, link that story to specific forecasts for revenue, earnings and margins, connect those forecasts to a fair value, then compare that fair value to the current share price. The whole view updates as new news or earnings arrive. For example, you might see one investor arguing for a fair value near US$120 based on confidence in digital commerce and fragrance growth, while another anchors closer to US$61 because of concerns around travel retail, China exposure and restructuring. You can then decide which story feels closer to your own.

Do you think there's more to the story for Estée Lauder Companies? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com