Lubelski Wegiel Bogdanka S.A.'s (WSE:LWB) Share Price Is Matching Sentiment Around Its Revenues

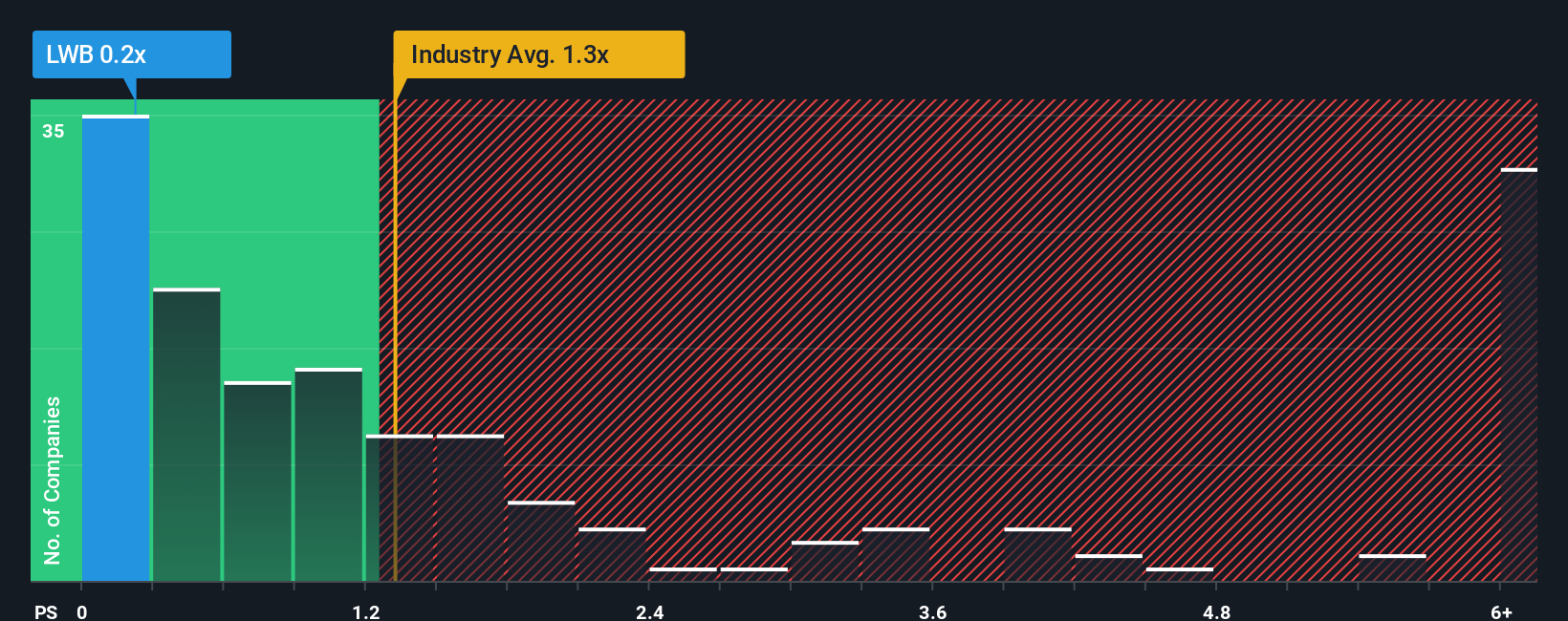

Lubelski Wegiel Bogdanka S.A.'s (WSE:LWB) price-to-sales (or "P/S") ratio of 0.2x might make it look like a buy right now compared to the Oil and Gas industry in Poland, where around half of the companies have P/S ratios above 1.3x and even P/S above 5x are quite common. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the reduced P/S.

Check out our latest analysis for Lubelski Wegiel Bogdanka

How Has Lubelski Wegiel Bogdanka Performed Recently?

With revenue that's retreating more than the industry's average of late, Lubelski Wegiel Bogdanka has been very sluggish. Perhaps the market isn't expecting future revenue performance to improve, which has kept the P/S suppressed. You'd much rather the company improve its revenue performance if you still believe in the business. Or at the very least, you'd be hoping the revenue slide doesn't get any worse if your plan is to pick up some stock while it's out of favour.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on Lubelski Wegiel Bogdanka.Is There Any Revenue Growth Forecasted For Lubelski Wegiel Bogdanka?

The only time you'd be truly comfortable seeing a P/S as low as Lubelski Wegiel Bogdanka's is when the company's growth is on track to lag the industry.

Retrospectively, the last year delivered a frustrating 20% decrease to the company's top line. This has soured the latest three-year period, which nevertheless managed to deliver a decent 11% overall rise in revenue. Accordingly, while they would have preferred to keep the run going, shareholders would be roughly satisfied with the medium-term rates of revenue growth.

Turning to the outlook, the next year should bring diminished returns, with revenue decreasing 7.1% as estimated by the only analyst watching the company. With the industry predicted to deliver 10% growth, that's a disappointing outcome.

In light of this, it's understandable that Lubelski Wegiel Bogdanka's P/S would sit below the majority of other companies. Nonetheless, there's no guarantee the P/S has reached a floor yet with revenue going in reverse. Even just maintaining these prices could be difficult to achieve as the weak outlook is weighing down the shares.

The Bottom Line On Lubelski Wegiel Bogdanka's P/S

Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

With revenue forecasts that are inferior to the rest of the industry, it's no surprise that Lubelski Wegiel Bogdanka's P/S is on the lower end of the spectrum. As other companies in the industry are forecasting revenue growth, Lubelski Wegiel Bogdanka's poor outlook justifies its low P/S ratio. It's hard to see the share price rising strongly in the near future under these circumstances.

The company's balance sheet is another key area for risk analysis. Take a look at our free balance sheet analysis for Lubelski Wegiel Bogdanka with six simple checks on some of these key factors.

If strong companies turning a profit tickle your fancy, then you'll want to check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.