Sonos (SONO) Is Down 5.2% After LG and Samsung Target Its Core Market at CES 2026

- At CES 2026, LG and Samsung unveiled new audio products aimed squarely at Sonos’s core multi-room and home audio market, intensifying competitive pressure on the company’s ecosystem.

- This fresh wave of big-brand competition comes just as Sonos is working through missed financial targets and projected near-term revenue softness, sharpening investor focus on its ability to defend share and margins.

- We’ll now examine how this heightened competition from LG and Samsung could influence Sonos’s investment narrative built around platform-driven growth.

Find companies with promising cash flow potential yet trading below their fair value.

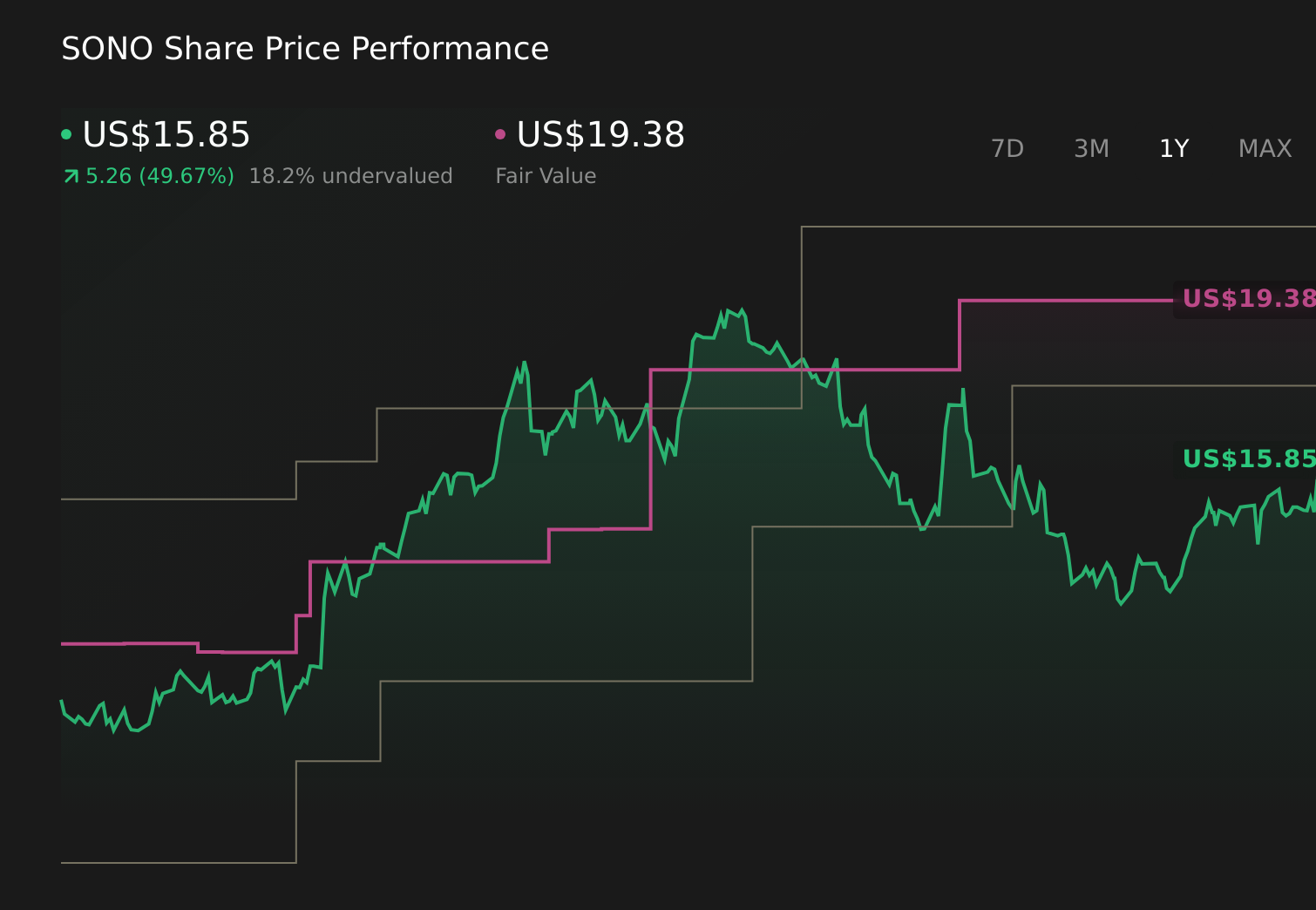

Sonos Investment Narrative Recap

To own Sonos today, you need to believe its multi-room audio platform and software ecosystem can stay relevant despite slow recent revenue growth, ongoing losses and intensifying big-brand competition. The CES 2026 launches from LG and Samsung add to the existing risk around tariffs, weak category demand and a lull in new hardware, but do not materially change the near term focus on Sonos’s ability to stabilize revenue and protect margins through its current product cycle.

The most relevant recent development alongside this CES news is the series of analyst price target increases, including Jefferies lifting its target to US$21.00 while reiterating a positive rating. That support from the analyst community sits against a backdrop of revenue declines, cost cuts and a delayed major hardware cycle, and keeps attention firmly on whether Sonos’s platform, software updates and category expansion can offset competitive and macro pressures.

But investors should also be aware that if increased tariffs force Sonos to choose between raising prices or absorbing costs, then...

Read the full narrative on Sonos (it's free!)

Sonos' narrative projects $1.6 billion revenue and $120.2 million earnings by 2028.

Uncover how Sonos' forecasts yield a $17.85 fair value, a 7% upside to its current price.

Exploring Other Perspectives

Four members of the Simply Wall St Community value Sonos between about US$6.21 and US$21.00, underlining how far apart individual views can be. Set against concerns about slowing hardware momentum and rising competition, these differing estimates invite you to explore several alternative viewpoints on how Sonos’s platform story might play out.

Explore 4 other fair value estimates on Sonos - why the stock might be worth less than half the current price!

Build Your Own Sonos Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- Our free Sonos research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Sonos' overall financial health at a glance.

No Opportunity In Sonos?

Our top stock finds are flying under the radar-for now. Get in early:

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 26 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- Rare earth metals are the new gold rush. Find out which 39 stocks are leading the charge.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com