Is It Time To Reassess Blackstone (BX) After Recent Share Price Weakness?

- If you are wondering whether Blackstone's current share price lines up with its underlying worth, you are not alone. That is exactly what this article tackles next.

- Blackstone closed at US$153.59, with a 7 day return of a 0.4% decline, a 30 day return of 1.5%, a year to date return of a 3.3% decline, a 1 year return of a 9.0% decline, a 3 year return of 102.4% and a 5 year return of 185.3%.

- Recent headlines around Blackstone have continued to focus on its position as a major global alternative asset manager and the role it plays in private markets, real estate and credit. This backdrop helps frame how investors are reacting to the stock's recent mix of shorter term weakness and much stronger multi year returns.

- Right now Blackstone has a valuation score of 0 out of 6 on our checks. Next we will look at how different valuation approaches arrive at that view, and why there may be an even better way to think about what the market is pricing in.

Blackstone scores just 0/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Blackstone Excess Returns Analysis

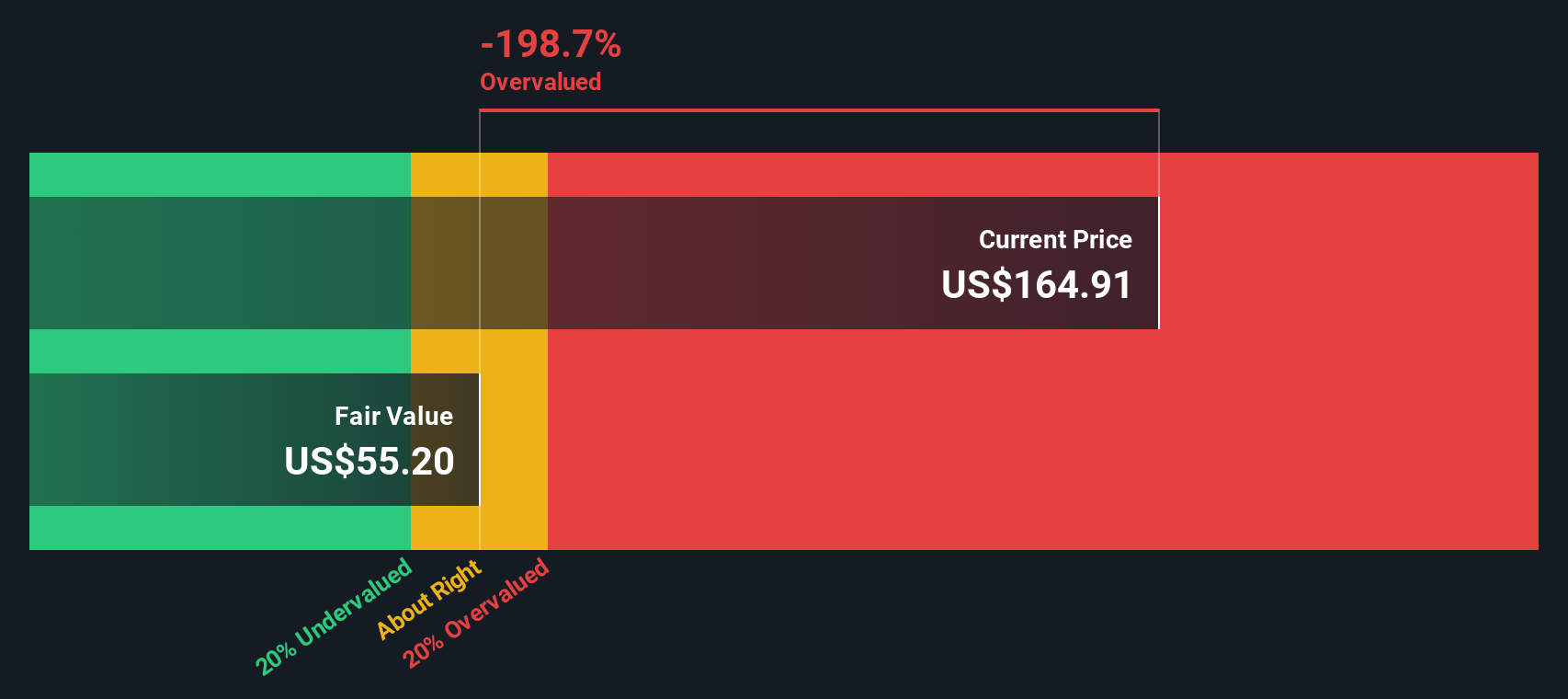

The Excess Returns model looks at how much profit a company can generate above the return that shareholders are assumed to require, then capitalizes those excess profits into an estimated intrinsic value per share.

For Blackstone, the starting point is a Book Value of $10.72 per share and a Stable EPS of $3.95 per share, based on weighted future Return on Equity estimates from 7 analysts. The model applies an Average Return on Equity of 49.27% to a Stable Book Value of $8.02 per share, which is based on estimates from 3 analysts.

The Cost of Equity is set at $0.66 per share, so the Excess Return, the profit above that required return, is $3.29 per share. These excess profits are then projected forward and discounted to arrive at an Excess Returns intrinsic value of about $73.91 per share.

Compared with the current share price of US$153.59, this suggests the stock is about 107.8% overvalued according to this model.

Result: OVERVALUED

Our Excess Returns analysis suggests Blackstone may be overvalued by 107.8%. Discover 884 undervalued stocks or create your own screener to find better value opportunities.

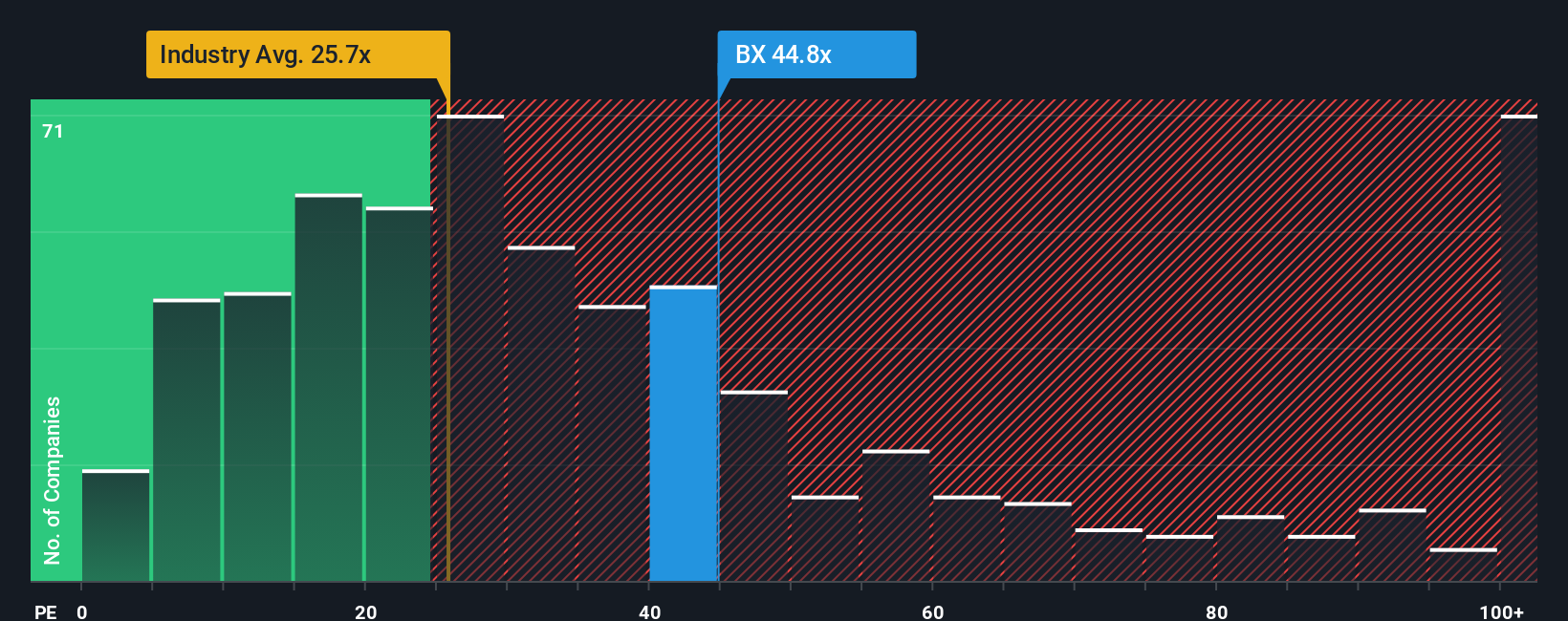

Approach 2: Blackstone Price vs Earnings

For a profitable company like Blackstone, the P/E ratio is a useful shorthand for what investors are currently willing to pay for each dollar of earnings. It ties the share price directly to the bottom line, which is usually the main driver of long term equity value.

What counts as a “normal” or “fair” P/E depends on how the market views a company’s growth prospects and risks. Higher expected growth or lower perceived risk can justify a higher multiple, while slower growth or higher uncertainty can point to a lower one.

Blackstone currently trades on a P/E of 44.40x. That is above the Capital Markets industry average of 25.77x and also above the peer group average of 38.49x. Simply Wall St’s Fair Ratio for Blackstone is 23.33x, which is its proprietary view of what a more appropriate P/E could be once factors like earnings growth, industry, profit margins, market cap and company specific risks are all considered. This tailored Fair Ratio can be more informative than a simple peer or industry comparison because it adjusts for those differences rather than assuming all companies deserve similar multiples. Comparing 44.40x to the Fair Ratio of 23.33x points to Blackstone trading at a richer level than this framework would suggest.

Result: OVERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1444 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Blackstone Narrative

Earlier we mentioned that there is an even better way to understand valuation, so Narratives on Simply Wall St give you a simple way to write your own story for Blackstone by linking your view of its future revenue, earnings and margins to a forecast and a Fair Value that you can compare with the current share price.

Instead of only relying on fixed models like P/E or Excess Returns, a Narrative lets you plug in your assumptions and see how that story translates into numbers. Because it sits inside the Community page, it is quick to use and easy to compare with what millions of other investors are thinking.

Narratives also refresh as new earnings, news or analyst updates arrive, so your Fair Value view automatically stays in sync with the latest information rather than being frozen at one point in time.

For example, one Blackstone Narrative on the cautious side might lean toward a Fair Value around US$167 per share with revenue growth closer to 18.5% and a future P/E near 14.4x. A more optimistic Narrative could point toward a Fair Value closer to US$193 per share with revenue growth around 20.3% and a future P/E of about 31.7x. Comparing those to the live market price can help you decide whether the stock fits your own expectations.

Do you think there's more to the story for Blackstone? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com