Anxiety grows amid DC boom

WHEN neighbourhood WhatsApp groups start raising concerns about the proliferation of data centres (DCs) in their backyards, the raison d’être of this new phenomenon comes to the fore.

Why are these facilities appearing in so many towns, from Petaling Jaya to Nilai, and from Sungai Buloh to Port Dickson?

To the man on the street, the questions hover around the social and economic impact of these DCs. Concerns over their thirst for our critical resources – electricity and water – are at the forefront: Will this lead to shortages or higher bills for everyday consumers?

The pace at which DC investments are flowing into the country has only heightened this anxiety. Malaysia is estimated to attract about US$40bil (RM162bil) in DC investments by 2030.

The dizzying speed of these developments, coupled with fears of a potential strain on resources, has prompted deeper scrutiny at the highest levels of government, sources say.

Should Malaysia consider imposing a moratorium on DC investments, like what Singapore did, until a thorough impact analysis is carried out?

Supporters of the industry, however, question why the country should pull the rug from under one of its most significant foreign direct investment (FDI) waves in recent years.

As one government official involved in wooing investments into the country explains, it is not easy to secure an investment deal these days due to intense competition from other countries, coupled with the fact that many multinational corporations are pulling back investments amid rising geopolitical and tariff-related risks.

“So when large DC investments come knocking on your door, is it wise to turn them away?”, he quips.

Concurring is DC consultant Gary Goh, who also disputes the argument that DCs do not generate sufficient economic spillovers.

“Which industry do you think is mainly driving Malaysia’s renewable energy (RE) sector? It is demand from DCs,” he says, adding that the RE ecosystem the country is building is a major employer of high-value jobs for Malaysians.

“Why stop this party? Capital expenditure by DCs runs into the billions of ringgit and will continue for a number of years to come. Malaysia cannot afford to miss this ride,” enthuses the CEO of a local construction company.

In the first place, why exactly are DCs flocking to Malaysia, and is it happening in other countries? DCs are expanding in the West at an enormous speed, albeit not without sporadic public opposition.

Notably, persistently rising electricity costs in the United States, which have more than doubled in some DC hubs, are eroding the country’s long-term competitiveness in favour of Asia as a more attractive investment destination.

But in South-East Asia, Malaysia stands out. Singapore is maxed out, while Malaysia’s Johor and Indonesia’s Batam are emerging as preferred alternatives to service Singapore-based demand.

Malaysia’s proximity to Singapore plays a part, as does the fact that few regional countries have electricity and water infrastructure as robust as ours.

Vietnam presents geopolitical risks for China-linked players, many of whom are DC operators in Malaysia or offtakers of DC capacity. Thailand’s ability to host large-scale DCs is similarly constrained by its current power grid capacity, although some believe it could catch up within the next few years.

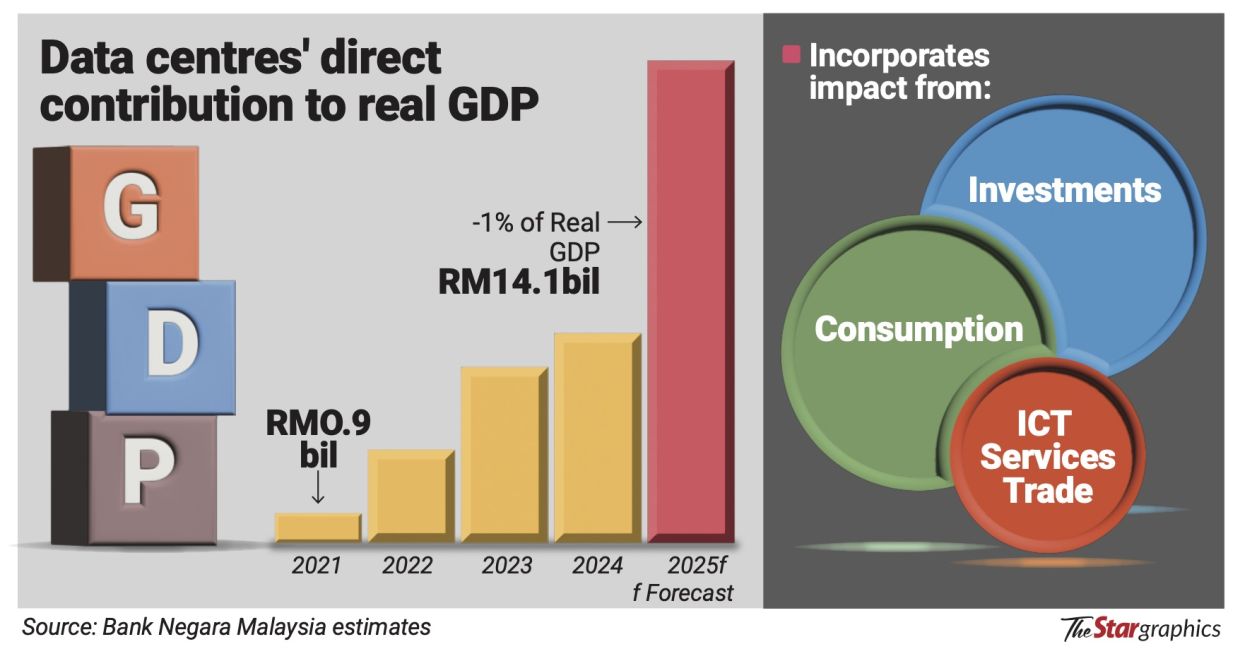

Bank Negara Malaysia (BNM) estimated that DCs will contribute about 1% of real gross domestic product (GDP), or RM14.1bil, in 2025.

But how exactly will this materialise, given that many components of DCs are imported and these facilities are highly automated, potentially limiting job creation?

In one of its quarterly bulletins last year, BNM wrote that this GDP contribution will primarily come from the construction phases of these DCs, coupled with private consumption from the salaries paid to DC employees.

However, the central bank did not provide a projection of how many people will actually be hired by DCs.

Questions remain about this analysis.

An economist with a local bank, who declined to be named, observes: “How much of that 1% comes from land purchases and construction activities that are short term in nature as opposed to recurring contributions to GDP? If it is the former, then such DC projects are more of a property investment than anything else.”

Interestingly, BNM itself has raised questions about the economics of DCs.

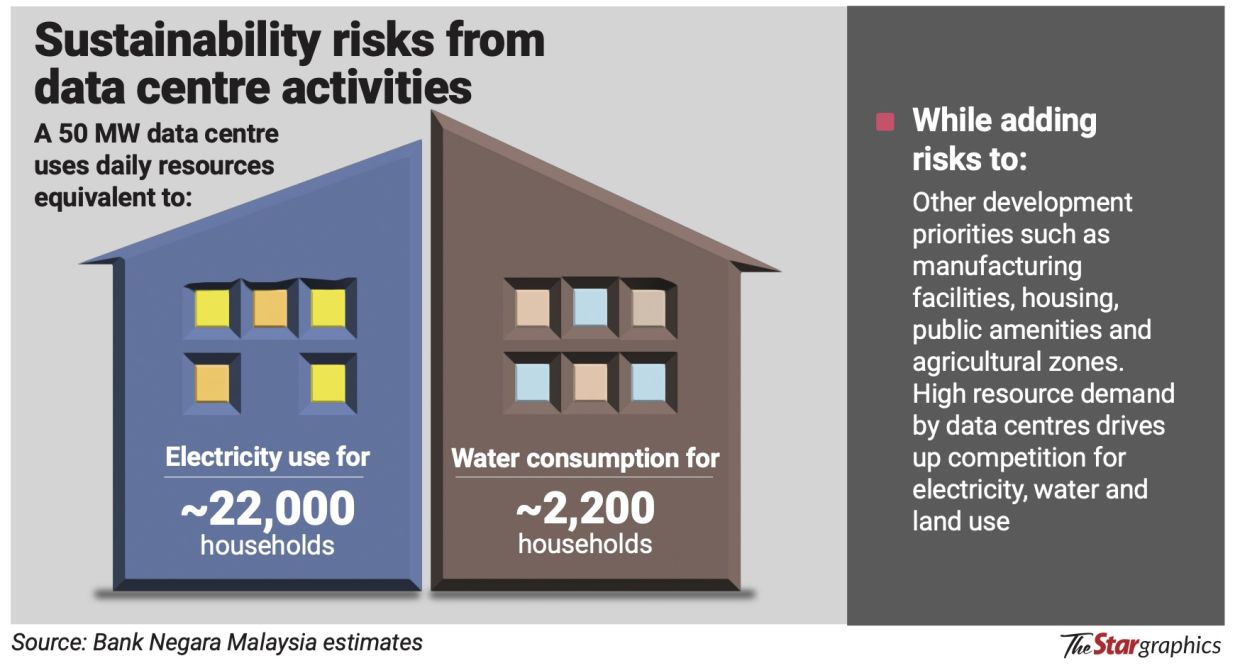

“Unregulated DC expansion can place a significant strain on domestic infrastructure, including electricity grids, water supply systems, and land use.

“Such pressures risk disrupting or displacing other development priorities such as industrial parks, housing, public amenities, and agricultural zones.

“Without coordinated and strategic planning, this could lead to utility bottlenecks, higher costs for other sectors, and undermine long-term urban planning,” the central bank says.

“It is important to have a water audit or study with a 10-to 15-year timeframe as part of the DC approval process.

“This ensures there will be sufficient water available to all stakeholders during that period following the entry of a DC, bearing in mind population increases, the expansion of new businesses in those areas, and the possibility of reduced water availability due to climate change,” he opines.

In 2019, Singapore imposed such a moratorium but lifted it in 2022. It now has a very strict approval process, selecting only DCs that meet high standards of energy efficiency, decarbonisation initiatives, and can demonstrate economic contributions.

Malaysia may have more resources to spare, but is it judicious to allocate a significant portion of them to DCs?

At present, Malaysia does not impose strict criteria, such as those in Singapore, on DCs. Nor is there any legally binding local content requirement, meaning DCs from, say, China, could literally build here by themselves if they so choose.

DCs that fulfil certain sustainability criteria, such as efficient energy and water use, currently receive incentives from the Malaysian government.

But why not make these guidelines into strict rules for DCs to adhere to if they wish to operate in Malaysia, rather than just incentive-based?

The criteria could also include local content requirements.

Another idea is to link Malaysia’s semiconductor industry with the DC boom – for example, new DCs could be required to have some of the chipsets in their computer servers packaged and tested locally.

Santiago adds that the government should also set targets for DCs to transition from fossil fuels to RE and to move from portable water to reclaimed water.

The resource fear

To be sure, the Malaysian government is not willy-nilly granting DC projects all the water and electricity they demand.

DCs must go through regulatory approvals, including from the Energy Commission, to get their allocations.

The commission, in consultation with utility giant Tenaga Nasional Bhd, reviews power demand requests to ensure they’re realistic and will not harm the reliability of the national grid.

Notably, DC energy consumption in Malaysia could reach over 5GW by 2035, a figure representing a staggering 40% of Peninsular Malaysia’s current power capacity, according to Malaysian Investment Development Authority (Mida) data.

The situation is similar with water, which is a state matter.

Water authorities participate in meetings with DC investors and government officials from Mida to determine whether the resource and related infrastructure are sufficient.

On a daily basis, a single 50MW DC would consume as much electricity as 22,000 households and as much water as 2,200 households.

No wonder the state of Johor isn’t rushing to approve new DC investments.

DCs with high water requirements are no longer being approved there, even though Johor is currently the country’s DC hub.

As of mid-2025, the state had attracted 42 DC projects worth a whopping RM164.45bil.

As a result, DC investments are shifting to other parts of the country, such as Selangor and Negri Sembilan.

Word on the street is that the single largest DC investment may appear in Selangor, with an estimated value of RM40bil.

Industry sources say discussions with the foreign investor have been ongoing for about a year, and Selangor was chosen due to the availability of land and other necessary resources.

Meanwhile, the government is racing to raise its energy capacity by calling for tenders to build more gas-fired power plants.

Combined with a global shortage of gas turbines needed for such plants, this could drive up energy prices if less efficient power plants are built.

If that happens, it lends credence to the theory that the rakyat may end up effectively “subsidising” DCs in Malaysia.

Bank exposure and bubble risk

Like all capital-intensive projects backed by offtakers, DCs are being funded by Malaysian and foreign banks, which is part of the normal course of business.

However, some sceptics of the DC boom worry if these banks fully understand the risks involved.

There are two types of hyperscale DCs: those purpose-built by technology giants such as Google, AWS and Microsoft, and those built by third-party operators (sometimes referred to as co-locators) who lease their DCs to others.

One key risk arises if a tenant decides to opt out of its contract.

While paying a fine may help the DC operator for a time, the facility could face financial difficulties in the long term.

Two weeks ago, Time dotCom Bhd executive vice-chairman Afzal Abdul Rahim warned that signs of stress in the sector could emerge this year.

Speaking on a panel titled “Beyond the Hype” at the CGS International 18th Annual Malaysia Corporate Day 2026, he said, “We have been in DCs for 26 years, and we often ask, when will this business stop? It could stop this year,” adding that the first signs of stress will be visible when a DC operator fails to service its debt.

“My sense is that banks in Malaysia and Singapore have exposure running into the tens of billions of dollars,” he said.

Afzal also noted that while much is being said about AI, “a lot of this is hype layered on top of hype.”

Some may argue that this is a stretch. But Afzal may not be far off. While demand for DCs is unlikely to slacken anytime soon, the need for massive DCs to house mega computing power is being questioned.

The prediction here is that DCs could one day be supplanted by smartphones.

As devices become more powerful and AI models get smaller, more computing could take place on smartphones, set-top boxes, or routers in users’ homes, reducing the need for remote DCs that we know today.

The economist from a local bank also raises the prospect of geopolitical risks affecting Malaysia’s DC boom.

“If US authorities decide too much capacity is serving Chinese users, multinational operators could be pressured to shift workloads elsewhere.

“It may not be that difficult for hyperscalers to terminate their leases here and move their DC hardware to a neighbouring country,” he says.

Economist Lee Heng Guie adds, “The sheer volume of DC projects in the pipeline stirs potential risks of stranded assets due to the underutilisation of facilities relative to business demand.”

For AmBank Group chief economist Firdaos Rosli, however, a bust may not be imminent.

He notes that while there appears to be overbuilding of DCs, a different outcome could emerge if one stretches the timeline.

“Just like the dotcom bust, there were concerns of oversupply. But eventually, all that capacity was taken up. So it’s just a matter of time,” he says.